Sydney, Australia, 27 December 2023 – Having reaffirmed its commitment to corporate social responsibility (CSR) earlier in the year, VT Markets is closing the year with 3 major environmental, social, and governance (ESG) milestones under its belt:

Food for good with the UN’s ShareTheMeal programme Through the United Nations’ online ShareTheMeal platform, VT Markets raised 2,000 meals for communities in need between November to December 2023.

A gift of joy with South Africa’s Cotlands Ahead of the holiday season, VT Markets donated 1,240 educational toys—including stacking rings and puzzles—to Cotlands, a Johannesburg organisation seeking to provide early development opportunities to marginalised children.

Youth advocacy at UNESCO’s Jakarta workshop In addition to pledging its support as a key sponsor, VT Markets advocated for equal treatment of young STEM professionals via a keynote address at the UNESCO-led 3rd International Workshop and Training on Youth and Young Professionals in Science, Engineering, Technology, and Innovation for Disaster and Climate Resilience.

Commenting on these initiatives, VT Markets’ Director of Global Marketing, Martin Li, stated: “The work we’ve done with ShareTheMeal, Cotlands, and UNESCO is just the start of much more to come. In a year that has yielded its fair share of challenges for humanity, we’re delighted to have contributed in some way.”

Heading into 2024, VT Markets is poised to build on this success. Off the back of a fresh partnership with the renowned team competing in the formula E world championship Maserati MSG Racing, the company will redouble its ESG efforts with both new and existing collaborators in tow. For news of upcoming initiatives and potential sponsorship opportunities, be sure to follow VT Markets on their official website and social media pages.

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

With no high-impact news expected, the market’s attention will be focused on the holiday season this week. Investor sentiment is likely to be influenced by holiday festivities, resulting in increased shopping activity and the investment of holiday bonuses. Additionally, the end-of-year period typically coincides with institutional investors going on vacation, leaving the market in the hands of comparatively bullish retail investors. This phenomenon, known as the Santa Claus rally, is expected to occur in the last week of December.

Holiday-related factors aside, here are several other medium-impact market indicators to watch for in the last week of 2023:

US unemployment claims (28 December 2023)

The number of Americans filing for unemployment benefits increased by 2,000 to 205,000 in the week ending 16 December, staying close to the 2-month low of 203,000 seen in the previous week.

Analysts expect a further rise to 207,000 in the week ending 28 December.

US pending home sales (28 December 2023)

Following a 1% rise in September 2023, pending home sales in the US dropped 1.5% month-over-month in October, marking the lowest level since records were first kept in 2001.

Analysts expect a 0.5% increase in the figures for November, set to be released on 28 December.

Thursday witnessed a strong comeback for stocks, with the S&P 500, Dow Jones, and Nasdaq rebounding significantly, nearing their record highs. Micron Technology’s stellar performance fueled tech stocks, while companies like Salesforce contributed to the climb. This turnaround followed a recent market dip attributed to profit-taking after a sustained period of gains. Meanwhile, the currency market saw the dollar index decline due to weaker U.S. economic data, impacting Treasury yields, while EUR/USD faced resistance and USD/JPY retreated within a defined range. Attention now turns to pivotal economic releases that could influence market dynamics, including the US core PCE and Japan CPI data.

Stock Market Updates

Stocks rebounded on Thursday after a recent dip, marking a robust resurgence in the year-end rally. The S&P 500 recovered from its recent decline, edging up by 1.03% to 4,746.75, inching within 1% of its closing high and 1.5% of its intraday record. The Dow Jones Industrial Average soared by 0.87% to 37,404.35, and the Nasdaq Composite surged 1.26% to 14,963.87. The market’s upward trajectory was widespread, with over 450 companies in the S&P 500 index witnessing gains. Micron Technology notably stood out, jumping by 8.6% following its quarterly performance surpassing expectations, bolstered further by an optimistic current-quarter guidance. Chip stocks broadly surged, with Intel and Advanced Micro Devices rising by 2.9% and 3.3%, respectively. Salesforce also contributed to the Dow’s climb, rising by 2.7% after receiving an upgrade from Morgan Stanley.

This upward swing followed a recent downtrend where Wall Street faced losses due to profit-taking after a streak of gains. The prior session marked the Dow and Nasdaq’s worst performance since October, breaking nine-day winning streaks, while the S&P 500 experienced its most significant decline since September. Rhys Williams, chief strategist at Spouting Rock Asset Management, attributed this shift to a technical correction following a robust market period. Since late October, the Dow and S&P 500 have surged over 15%, while the Nasdaq Composite saw an impressive 18% surge during the same period, reflecting a substantial upward momentum in the market.

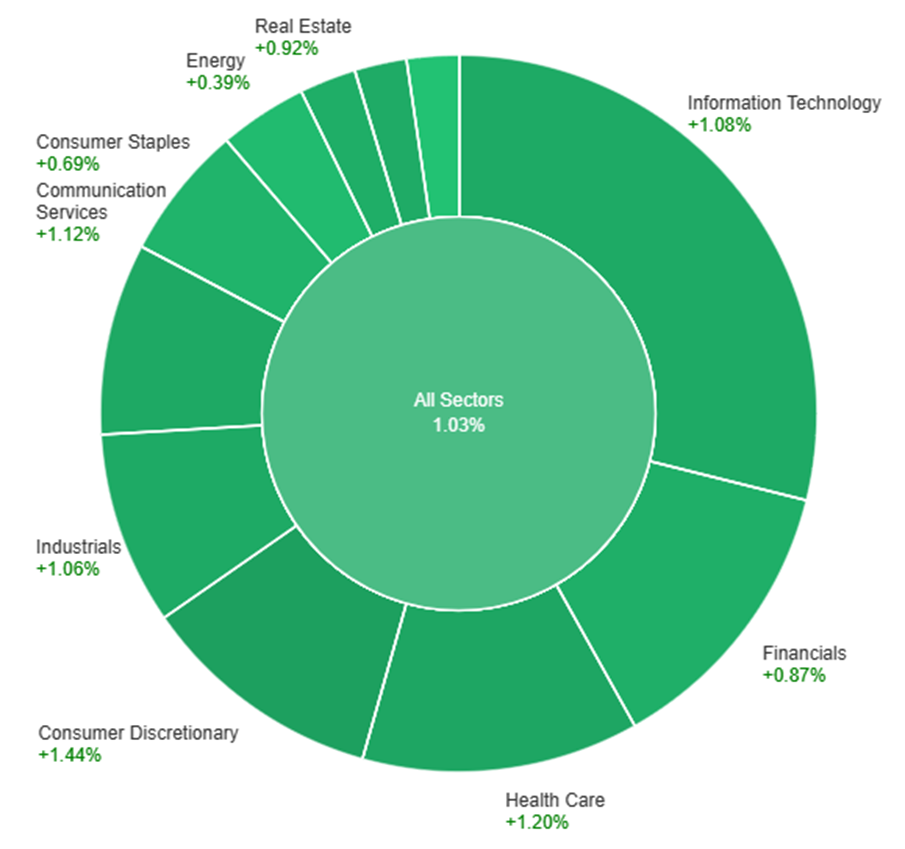

On Thursday, across various sectors, the market showed a general upward trend with an overall increase of 1.03%. Consumer Discretionary saw the highest surge at 1.44%, followed closely by Health Care at 1.20% and Communication Services at 1.12%. Information Technology and Industrials also experienced notable gains at 1.08% and 1.06%, respectively. Meanwhile, Energy and Utilities demonstrated the smallest upticks, with Energy rising by 0.39% and Utilities by 0.13%. Real Estate and Financials fell within the mid-range increases, with Real Estate at 0.92% and Financials at 0.87%. Consumer Staples trailed behind with a rise of 0.69%.

Currency Market Updates

The currency market saw notable shifts as the dollar index declined by 0.4% due to weaker-than-expected U.S. economic data, impacting Treasury yields. Despite a solid 4.9% annualized GDP increase in Q3, downward revisions in GDP and core PCE figures influenced market sentiment. Core PCE rose only 2.0% year-on-year, signaling a potential downside miss, which could favor dollar bears. The upcoming release of November’s core PCE, income, and spending figures was highlighted as pivotal for Treasuries, risk, and the dollar, with indications pointing towards a possible downward trend in core PCE, impacting market dynamics.

EUR/USD observed a 0.4% rise, facing resistance near 1.1000 due to ongoing weak economic data and outlooks in the eurozone, particularly in Germany. USD/JPY, on the other hand, experienced a 0.8% fall, retracting all weekly gains but maintaining a recovery pattern within the 140.95-4.95 range following dovish meetings from both the Fed and BoJ. With the upcoming Japan CPI and U.S. core PCE releases, attention is on the 200-day moving average at 142.72, potentially signaling a retest of 140.95. Sterling saw a marginal 0.25% rise amidst a pessimistic UK CBI retail sales survey and below-forecast UK CPI, with further market focus on impending UK retail sales and Q3 GDP announcements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD USD Gains Ground Amid Dollar Weakness Despite Mixed US Data; Eyes on Inflation Figures

The EUR/USD edged higher, reaching the 1.1000 mark as the Dollar struggled despite increased Treasury yields. US economic indicators presented a mixed picture, with declines in the Philadelphia Fed Index and a revision in Q3 GDP, while Jobless Claims remained steady. Investors await the crucial Core PCE inflation data, anticipating a 0.2% rise for November. Despite the rebound in US yields, the Dollar remains subdued, limiting the EUR/USD upside potential amidst thinner market conditions.

On Thursday, the EUR/USD moved higher and reached the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 66, signaling a neutral outlook for this currency pair.

Resistance: 1.1017, 1.1138

Support: 1.0946, 1.0830

XAU/USD (4 Hours)

XAU/USD Resilient Above $2,040 Despite USD Swings Amidst Mixed US Economic Data

In fluctuating market sentiment driven by a resilient US Dollar and mixed economic indicators, spot Gold managed to maintain its position above $2,040 per troy ounce. The Dollar initially gained traction, favored by Wall Street’s lackluster performance and softer Treasury yields, but a shift in direction followed mixed US data. Despite GDP figures slightly below estimates and declining bond yields, investor confidence bounced back on Wall Street. With attention now turning to upcoming US economic releases, including the Core PCE Price Index and Michigan Consumer Sentiment Index, Gold remains resilient amidst the market’s uncertain landscape.

On Thursday, XAU/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just below the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 63, signaling a neutral outlook for this pair.

Stock futures edged higher after a recent market pause, with S&P 500, Nasdaq 100, and Dow Jones futures indicating slight upticks. Micron’s notable postmarket leap of over 4% propelled optimism after surpassing Wall Street’s projections for its first fiscal quarter. However, the prior day marked a downturn as investors seized profit opportunities, reflecting the S&P 500’s worst performance since September. Looking forward, attention is on forthcoming economic indicators like jobless claims and GDP figures, alongside Nike’s imminent earnings release. In currency markets, Sterling declined by 0.5% due to disappointing UK CPI, while the dollar, euro, and yen stabilized. Ongoing central bank comments continue to sway sentiment, impacting the EUR/USD pair and hinting at potential shifts in global monetary policies tied to upcoming data releases like Japan’s core CPI and the U.S. core PCE.

Stock Market Updates

Stock futures indicated a modest upward trend following a pause in the recent market surge. S&P 500 futures rose by 0.16%, Nasdaq 100 futures by 0.24%, and Dow Jones Industrial Average futures climbed 0.15%. Micron experienced a significant postmarket increase, jumping over 4% after surpassing Wall Street’s expectations for its first fiscal quarter and providing a stronger-than-expected outlook for the current quarter. The day prior witnessed a downturn in the markets as investors seized the opportunity to capitalize on recent profits, resulting in the S&P 500’s worst performance since September and the Dow and Nasdaq marking their most significant drops since October. These declines marked a breather from a robust market rally that saw substantial gains in the Dow, S&P 500, and Nasdaq Composite over the past few months.

Looking ahead, investors are eyeing upcoming data releases such as jobless claims and third-quarter gross domestic product figures, along with the closely watched personal consumption expenditures price index, known as an essential measure of inflation. Additionally, market watchers are anticipating Nike’s earnings announcement after the closing bell on Thursday, which is likely to influence market sentiment and direction.

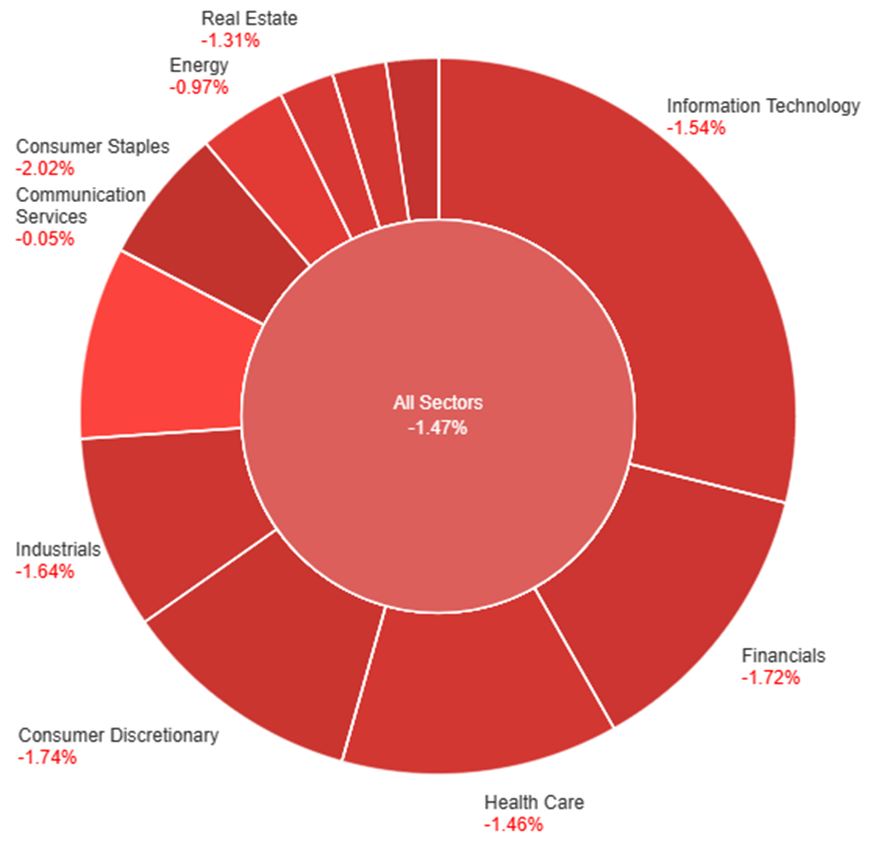

On Wednesday, the overall market experienced a decline of 1.47%. Across sectors, most industries saw negative movements, with Utilities and Consumer Staples facing the steepest drops at -1.98% and -2.02% respectively. The Information Technology sector also fell notably by 1.54%, while Financials and Consumer Discretionary both recorded decreases of 1.72% and 1.74% respectively. Other sectors such as Health Care, Materials, and Industrials followed a similar downward trend, showing declines ranging from 1.46% to 1.64%. Communication Services and Energy sectors were relatively less affected, with marginal decreases of -0.05% and -0.97% respectively. Real Estate experienced a decline of 1.31%. Overall, it was a day of widespread negative performance across various sectors, with Utilities and Consumer Staples bearing the brunt of the losses.

Currency Market Updates

In recent currency market movements, Sterling faced losses as UK CPI fell below expectations, leading to a 0.5% decline. This drop was influenced by a significant 16bp decrease in two-year gilt yields, impacting the market and offsetting risk-on flows. Conversely, the dollar, euro, and yen stabilized within specific ranges following fluctuations post-recent central bank meetings. However, these adjustments were insufficient to extend the EUR/USD’s attempt to surpass November and December highs or bolster USD/JPY after its post-Fed pivot retreat.

The market sentiment remains influenced by ongoing post-meeting comments from the Fed and ECB. Eurozone dynamics saw ECB hawks challenging aggressive rate cut expectations while grappling with declining German producer prices amidst forecasts of increased German inflation in early 2024 due to budget constraints. As a result, the EUR/USD pair experienced a 0.2% decline, nearing 1.0950 from its late 2023 peaks. Additionally, the focus now shifts towards upcoming data releases, including Japan’s core CPI, predicted to drop to 2.5%, potentially influencing the BoJ’s policies. Meanwhile, the U.S. core PCE is expected to decrease to 3.3%, aligning with futures pricing indicating a decline in Fed rates to 3.85% by the next December. These impending reports stand poised to shape future currency movements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Teeters Amid US Dollar Recovery: Key Data Points Influence Direction

The EUR/USD faced a dip amidst a recovering US Dollar Index, struggling to break the 1.1000 mark as it moved directionlessly. Supported by a weak US Dollar and a hint of risk appetite, the pair showed resilience. Positive US data, including a rise in Existing Home Sales and Consumer Confidence, countered the Eurozone’s moderate uptick in Consumer Confidence and the ECB’s resistance to early rate cuts. While the bias leans towards an upward trajectory, the EUR/USD needs to breach 1.1000 swiftly to mitigate focus on the diverging economic performances of the US and Eurozone. Thursday’s upcoming data, including Jobless Claims and Q3 GDP, followed by Friday’s Core PCE report, will likely steer the pair’s direction.

On Wednesday, the EUR/USD moved slightly lower reaching the middle band of the Bollinger Bands. Currently, the price moving slightly above the upper band, suggesting a potential for another upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1017, 1.1138

Support: 1.0946, 1.0830

XAU/USD (4 Hours)

XAU/USD Holds Steady Amidst USD Strength and Inflation Concerns

Spot Gold, represented by XAU/USD, navigated within a tight range as the US Dollar gained momentum earlier in the day, buoyed by upbeat US data like the CB Consumer Confidence report. Despite hitting an intraday high before retracing, Gold settled near its daily low. Market sentiment shifted during the European session on news of easing UK inflation, alleviating some concerns. Eyes now turn to the upcoming US Personal Consumption Expenditures Price Index, anticipated to influence markets significantly and potentially affirm or challenge the Fed’s recent policy stance.

On Wednesday, XAU/USD moved slightly lower and reached the middle band of the Bollinger Bands. Currently, the price moving just above the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 56, signaling a neutral outlook for this pair.

The stock market witnessed a strong surge, propelling the S&P 500 close to its all-time high after significant gains fueled by the Federal Reserve’s positive stance on interest rates. The Dow Jones Industrial Average and Nasdaq Composite also experienced substantial increases, while energy stocks, particularly in the S&P 500 sector, saw notable rises due to escalating oil prices. The bullish momentum, backed by the Fed’s indications of potential interest rate cuts in 2024 and favorable market conditions, led to December’s substantial gains across major indices. Concurrently, currency markets saw fluctuations, with the US Dollar Index declining, housing sector data revealing mixed results, and various currency pairs experiencing diverse movements amidst global economic shifts.

Stock Market Updates

The stock market showed a robust uptick, with the S&P 500 nearing its all-time high after a 0.59% gain, coming within 0.6% of its previous record close. This surge was fueled by the Federal Reserve’s dovish stance on interest rates, fostering investor confidence. The Dow Jones Industrial Average climbed by 0.68%, reaching 37,557.92 points, while the Nasdaq Composite surged by 0.66%, breaching the 15,000 mark for the first time since January 2022. Additionally, the Nasdaq 100 hit all-time intraday and closing highs, ascending by 0.49% to 16,811.85. Energy stocks, particularly in the S&P 500 sector, outperformed with a 1.2% rise, propelled by increasing oil prices, with companies like Occidental Petroleum, Halliburton, and Exxon Mobil witnessing significant gains. Moreover, Walgreens Boots Alliance led the Dow with a 4.2% surge, while Enphase Energy and First Solar notably contributed to S&P 500 advances, up by about 9% and 4%, respectively.

The market’s bullish momentum has been amplified by recent Federal Reserve indications of potential interest rate cuts in 2024, along with encouraging signs of moderated inflation and a retreat in Treasury yields. December showcased significant gains across the board, with the S&P 500, Dow, and Nasdaq boasting increases of 4.4%, 4.5%, and 5.5%, respectively, reflecting the market’s strong performance and its longest weekly winning streak since 2017. This rally coincides with the typically robust season for equities, further buoyed by favorable market conditions.

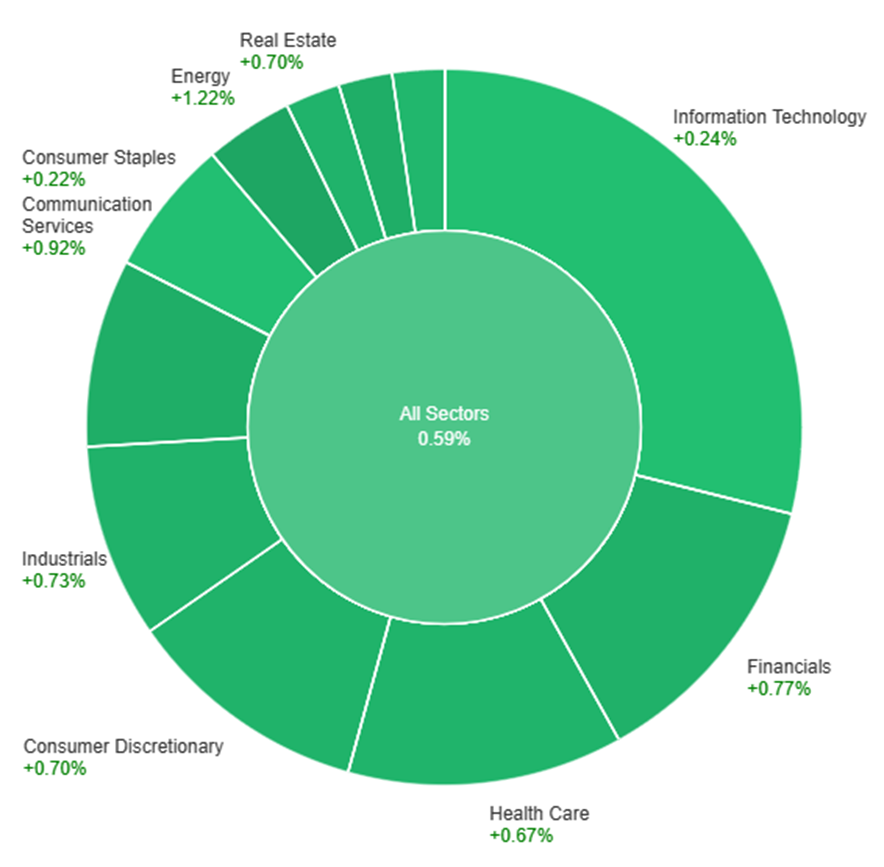

On Tuesday, across all sectors, there was a positive trend with a 0.59% increase. Energy notably surged by 1.22%, leading the gains, followed closely by Communication Services and Materials, both showing strong increases at 0.92% and 0.91%, respectively. Financials, Industrials, Consumer Discretionary, and Real Estate all demonstrated moderate growth between 0.70% and 0.77%. Health Care also contributed positively, rising by 0.67%, while Utilities saw a more modest increase of 0.56%. However, Information Technology and Consumer Staples exhibited lower growth rates, with increases of only 0.24% and 0.22%, respectively, compared to the other sectors.

Currency Market Updates

In the latest currency market updates, the US Dollar Index (DXY) continued its downward trajectory, slipping by over 0.30% and approaching the 102.00 mark, albeit remaining above December lows. Wall Street stocks surged, pushing the Dow Jones to a fresh all-time high close, while the 10-year Treasury yield hovered around 3.90%. Mixed data from the US housing sector revealed an unexpected rise in Housing Starts to 1.56 million, surpassing predictions, while Building Permits slightly declined to 1.46 million, below the anticipated figure. Wednesday’s focus will be on further housing data release with Existing Home Sales and the CB Consumer Confidence survey.

Meanwhile, the currency pairs saw notable movements: EUR/USD displayed an upward bias but struggled to reclaim the 1.1000 mark, hovering around 1.0970. GBP/USD trimmed gains and dipped towards 1.2700, encountering resistance near 1.2800, ahead of significant UK consumer and wholesale inflation figures due on Wednesday. The Japanese Yen weakened sharply following a “dovish hold” by the Bank of Japan, impacting USD/JPY, which initially spiked before retracing amidst a weaker US Dollar and declining global yields. USD/CHF hit four-month lows under 0.8600 and is expected to test the 2023 low around 0.8550, with the Swiss National Bank’s quarterly bulletin due.

Additionally, the Canadian Dollar (CAD) strengthened across the board after the Consumer Price Index rose 0.1% in November, contrary to expectations of a 0.2% decline. This led USD/CAD to its lowest daily close since early August below 1.3350, ahead of the Bank of Canada’s (BoC) Summary of Deliberations. On another front, AUD/USD broke above 0.6730 and surged to 0.6774, marking its highest level in nearly five months, driven by US Dollar weakness, improved risk appetite, and support from rallying commodity prices. Meanwhile, Gold prices struggled to sustain gains above $2,040, while Silver, despite reclaiming $24.00, faced challenges holding above the 20-day Simple Moving Average, aiming for a breakthrough at $24.30 for substantial advances in XAG/USD (Silver/US Dollar).

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges Amid Dollar Weakness Despite Euro’s Mixed Signals

The EUR/USD pair rallied for a consecutive second day, edging closer to the 1.1000 mark and November’s peaks, buoyed by a faltering US Dollar amidst growing risk appetite. Despite the Dollar’s downturn, the Euro’s outlook remains uncertain, highlighted by Eurostat’s revised downward November inflation figures, tempering optimism. As the Federal Reserve and European Central Bank officials push against market expectations, the interest rate market hints at probable rate cuts by April, pressuring the Dollar amid ascending equity and commodity prices. Mixed US housing sector data added to the complex market landscape, with Housing Starts surpassing forecasts while Building Permits fell short. The upcoming data on Wednesday, including Current Account, Construction Output, and Consumer Confidence figures, further intensifies the intricate dynamics influencing the EUR/USD pair.

On Tuesday, the EUR/USD moved higher trying to reach the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 65, signaling a neutral but still bullish outlook for this currency pair.

Resistance: 1.1017, 1.1138

Support: 1.0946, 1.0830

XAU/USD (4 Hours)

XAU/USD Holds Steady Amidst Dollar Weakness and Equities’ Optimism

Gold (XAU/USD) maintained a resilient stance, hovering around $2,040 as the US Dollar weakened, buoyed by a positive equities market driven by robust risk appetite. The Nasdaq Composite achieved consecutive record highs, reinforcing the sentiment inspired by central banks. Compounding the USD’s pressure were sliding Treasury yields, hitting lows unseen since July. Despite a relatively quiet US macroeconomic calendar, attention is fixated on Friday’s release of the Core PCE Price Index, the Federal Reserve’s favored inflation gauge, keeping speculative interests keenly attuned to potential market shifts.

On Tuesday, XAU/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just below the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 62, signaling a neutral outlook for this pair.

The stock market witnessed a persistent upward trend with the S&P 500 maintaining a seven-week winning streak, inching closer to its previous all-time high. While the Dow Jones Industrial Average showed marginal movement, the S&P 500 surged by 0.45%, notably driven by gains in mega-cap tech companies like Meta Platforms and Alphabet. U.S. Steel shares soared by 26% following an acquisition announcement by Japan’s Nippon Steel. December marked robust performance across major indices, spurred by the Federal Reserve’s indication of potential short-term interest rate cuts in 2024 amidst cooling inflation. In the currency market, fluctuations in major pairs like EUR/USD, USD/JPY, Dollar Index, and British Pound were observed, influenced by speculation on rate cuts by central banks and economic indicators impacting their trajectories.

Stock Market Updates

The stock market saw a continuation of its upward trend as the S&P 500 maintained its seven-week winning streak. The Dow Jones Industrial Average experienced marginal movement, edging up by only 0.86 points to 37,306.02, while the S&P 500 climbed by 0.45% to reach 4,740.56, inching closer to its all-time closing high from January 2022, now just 1.2% away. Communication services stood out with a 1.9% increase in the S&P 500, notably driven by gains in mega-cap tech companies like Meta Platforms and Alphabet, which surged nearly 3% and more than 2%, respectively. Additionally, U.S. Steel shares soared by 26% following the announcement of Japan’s Nippon Steel acquiring the company for $14.9 billion.

December showcased robust performance across major indices, with the S&P 500 up by 3.8% for the month, while the Dow and Nasdaq rose by 3.8% and 4.8%, respectively. The positive investor sentiment stemmed from the Federal Reserve’s indication of expecting three short-term interest rate cuts in 2024, given the backdrop of cooling inflation. This sentiment shift led to a drop in Treasury yields, with the 10-year Treasury yield dipping below the 4% mark, further contributing to the market’s positive trajectory.

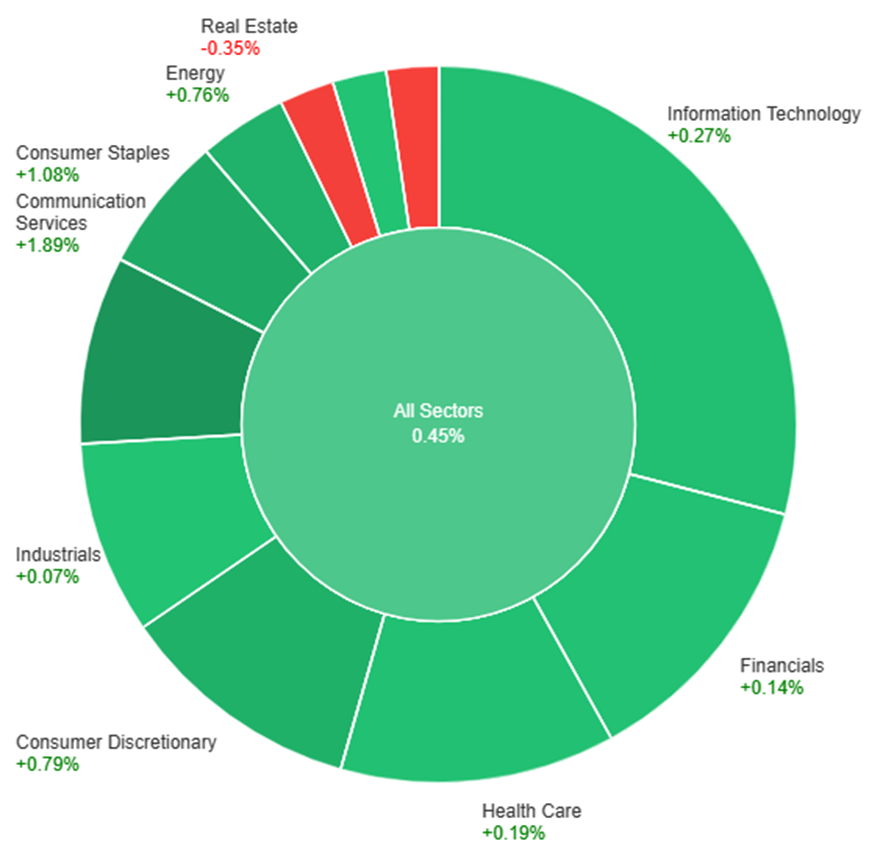

On Monday, the overall market saw a positive trend, with a collective rise of 0.45% across all sectors. Notably, Communication Services performed exceptionally well, soaring by 1.89%, followed by strong gains in Consumer Staples at 1.08% and Consumer Discretionary at 0.79%. Energy and Information Technology also contributed positively with increases of 0.76% and 0.27%, respectively. However, Utilities and Real Estate experienced declines, showing decreases of -0.30% and -0.35%, respectively, marking the only sectors that saw a downturn on that day.

Currency Market Updates

In the recent currency market updates, the focus was primarily on the fluctuations of major currency pairs, notably the EUR/USD and USD/JPY, alongside observations regarding the Dollar Index and the British Pound. The Dollar Index experienced a 0.1% decline amid speculations regarding potential rate cuts by the Fed, ECB, and BoE in 2024. The EUR/USD pair saw a 0.3% rise, influenced by the rebound in Bunds-Treasury yield spreads due to resistance from some ECB policymakers against early 2024 rate cuts. However, the pair faced concerns over German Ifo business sentiment and the risk of a potential recession reading, impacting its trajectory within a specific trading range.

Conversely, USD/JPY observed a 0.5% increase as it continued its recovery from prior plunges, influenced by market uncertainties surrounding aggressive Fed rate cut expectations versus the possibility of a BoJ hike. The broader trend for USD/JPY seemed downward, particularly if the BoJ failed to indicate a move away from negative rates. Meanwhile, the British Pound declined by 0.3%, distancing itself from recent highs following a dovish Fed and hawkish BoE meeting. Focus shifted to the upcoming UK CPI report, while observations noted a bearish divergence from last week’s highs and a strong demand for Sterling at its 200-day moving average, hinting at potential consolidation in the near term.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds Ground Amidst Dollar Pressure and ECB Speculation

The EUR/USD pair showed resilience, edging up after a recent dip, finding support above the 20-day SMA, and hovering above 1.0900 in a subdued market atmosphere. The US Dollar faced bearish pressures following the Federal Reserve’s dovish tone, although rate cuts seem distant despite initial forecasts. Meanwhile, in the Eurozone, lower-than-expected IFO business survey readings in Germany and steady but moderate inflation figures have raised expectations of potential ECB rate cuts, capping the Euro’s upward momentum below the 1.1030 mark. The market awaits the US Core PCE Price Index report for further cues on the greenback’s trajectory.

On Friday, the EUR/USD moved flat and moved around the middle band of the Bollinger Bands. Currently, the price moving slightly below the middle band, suggesting a potential for another consolidation movement. Notably, the Relative Strength Index (RSI) maintains its position at 57, signaling a neutral but still bullish outlook for this currency pair.

Resistance: 1.0945, 1.1017

Support: 1.0895, 1.0830

XAU/USD (4 Hours)

XAU/USD Maintain Soft Tone Amid Fed’s Stance on Monetary Policy and Market Optimism

Gold prices for XAU/USD held marginally above Friday’s closure at $2,018.19 per troy ounce despite subdued demand for the US Dollar triggered by softer government bond yields following the Fed’s decision to halt monetary tightening. The Fed’s stance, marking a pivot toward potential rate cuts, caused a retreat in US Treasury yields, notably the 10-year note, which currently stands at 3.95%. Wall Street’s positive performance limited the safe-haven appeal of the Greenback, constraining upward movement for gold. However, as financial markets approach the winter holidays, attention turns to upcoming inflation updates from the UK, Canada, and the Bank of Japan’s monetary policy decision, culminating with the US releasing the Core PCE Price Index, anticipated to show a slight decrease in November’s YoY inflation.

On Friday, XAU/USD moved in consolidation around the middle band of the Bollinger Bands. Currently, the price moving just below the middle band, suggesting a potential consolidation movement. The Relative Strength Index (RSI) stands at 53, signaling a neutral outlook for this pair.

This week, the market’s focus will primarily revolve around the Bank of Japan’s rate decision. Investors are eagerly anticipating any statements from the bank’s governor Kazuo Ueda, especially after observing the impact of the strong Japanese Yen arising from a weakening US Dollar. In addition to this, consumer price index (CPI) and gross domestic product (GDP) data for various regions will also be released, possibly further affecting the market.

As always, traders are advised to exercise caution as we approach these significant market highlights for the week:

Bank of Japan’s interest rate decision (19 December 2023)

Following its October meeting, the Bank of Japan (BOJ) maintained its key short-term interest rate at -0.1% and held 10-year bond yields steady at approximately 0%.

No changes are expected in the BOJ’s upcoming rate statement, scheduled for release on 19 December.

Canada CPI (19 December 2023)

Canada’s CPI rose by 0.1% month-over-month in October 2023, rebounding from a 0.1% decline in September.

Analysts expect a decrease of 0.2% in the CPI figures for November, scheduled for release on 19 December.

UK annual CPI (20 December 2023)

The UK’s annual CPI data reflected a decline in the UK’s inflation rate, from 6.7% in August and September 2023 to 4.6% in October 2023.

Analysts expect the UK’s annual CPI to drop further to 4.3% in the next set of updated figures, scheduled for release on 20 December.

US final GDP (21 December 2023)

The US economy saw an annualised expansion of 5.2% in Q3 2023, surpassing a preliminary estimate of 4.9% and marking the strongest growth since Q4 2021.

Analysts expect a 5.2% expansion in the US economy to be confirmed following the release of updated GDP data on 21 December.

UK retail sales (22 December 2023)

Retail sales in the UK declined by 0.3% month-over-month in October 2023 following a revised 1.1% decrease in September.

Analysts expect a 0.5% increase in the next set of UK retail sales figures, scheduled for release on 22 December.

Canada GDP (22 December 2023)

The Canadian economy grew by 0.1% in September 2023, primarily propelled by a 0.3% increase in goods-producing industries. This also marked its first upturn in six months.

Analysts expect a 0.2% increase in the next set of GDP data for Canada, slated for release on 22 December.

US core PCE price index (22 December 2023)

Core personal consumption expenditure (PCE) prices for the US increased by 0.2% in October 2023, marking a slight easing from the 0.3% rise observed in September.

Analysts expect a 0.2% increase in the core PCE price index for the US following the release of updated data on 22 December.

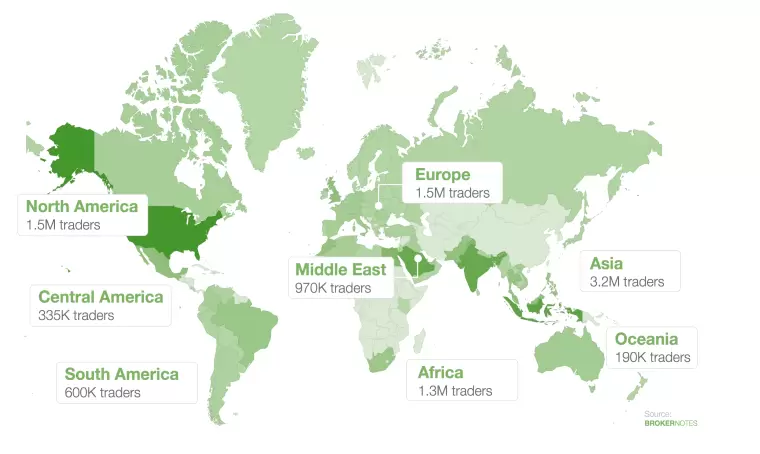

The Forex market’s landscape is constantly evolving, with various countries emerging as key players based on the number of active traders.

In 2023, according to data provided by Forex Broker Report, there’s been a significant global distribution of Forex traders. This spread is largely influenced by the intricate dynamics of advanced financial systems and regulatory frameworks.

The regional distribution of online Forex traders Source: Broker Notes

The global distribution of online Forex traders, as highlighted in the ForexBrokers.com report, shows a notable regional variance: Asia leads with 3.2 million online traders, Europe follows with 1.5 million, and Africa with 1.3 million, while the United States also shows a substantial presence in the Forex market. These figures underscore the widespread popularity and varied levels of Forex trading engagement across different regions.

As we delve into the top 10 countries at the forefront of Forex trading, each presents a unique combination of attributes and challenges within their Forex markets.

1. United Kingdom (341,000 Traders)

The UK, especially London, is not just Europe’s but one of the world’s foremost financial hubs. The Financial Conduct Authority (FCA) provides robust regulation, ensuring transparency and trader protection. London’s time zone advantageously positions it to capitalise on both Asian and American market hours, enhancing its Forex trading activity.

2. United States (335,000 Traders)

The U.S. boasts a highly developed financial market with extensive Forex trading activity. The regulatory environment, overseen by organisations like the CFTC and NFA, ensures a secure trading platform for a diverse array of traders. The U.S. dollar’s dominance in global finance further amplifies the country’s role in the Forex market.

3. Japan (223,000 Traders)

Japan’s Forex market has witnessed exponential growth since retail Forex trading was legalised in 1998. The Japanese yen, a major currency in Forex markets, is often involved in carry trades due to Japan’s low-interest-rate environment. The Financial Services Agency (FSA) maintains a well-regulated trading environment, balancing openness with trader protection.

4. Singapore (218,000 Traders)

As a critical financial centre in Asia, Singapore’s strategic location enables significant trading overlap with global markets. The Monetary Authority of Singapore (MAS) is known for its stringent regulatory standards, fostering a secure and efficient trading environment. Singapore’s advanced technological infrastructure also contributes to its robust Forex market.

5. Hong Kong (200,000 Traders)

Hong Kong stands as a significant gateway to Asian markets, with a stable economy and a strong regulatory framework. The Hong Kong dollar is a crucial currency in Forex markets, and the region’s proximity to mainland China adds to its strategic trading position. Hong Kong’s sophisticated financial services sector attracts traders globally.

6. Australia (195,000 Traders)

Australia’s Forex market is underpinned by its resource-driven economy and political stability. Regulated by the Australian Securities and Investments Commission (ASIC), the market offers a safe environment for traders. The Australian dollar, a commodity currency, is highly influenced by the country’s trade dynamics, particularly with China.

7. Switzerland (182,000 Traders)

Switzerland’s reputation for financial stability and banking secrecy makes its Forex market attractive. The Swiss Franc, a safe-haven currency, is a popular choice during global economic uncertainties. Switzerland’s Forex market benefits from its neutrality and the country’s stringent regulatory practices.

8. France (120,000 Traders)

France’s Forex market is integral to the Eurozone. The Euro’s strength and stability, combined with France’s significant economic position in Europe, make it a key player in Forex trading. The Autorité des Marchés Financiers (AMF) ensures a well-regulated trading environment.

9. Germany (109,000 Traders)

Germany’s robust economy and the Euro’s prominence bolster its Forex market. Germany’s Forex trading is influenced by its strong industrial and export sectors. The Federal Financial Supervisory Authority (BaFin) provides a stringent regulatory framework, ensuring market integrity.

10. China (105,000 Traders)

China’s growing Forex market reflects its rising economic power. The Chinese Yuan’s increasing inclusion in global Forex trading symbolises China’s expanding financial influence. However, the market is more regulated and less open than in other major countries, with strict oversight from the People’s Bank of China and SAFE.

In conclusion, the Forex trading landscape in 2023 highlights the diversity and dynamism of global financial markets. Each of the top 10 countries offers unique advantages and challenges, shaped by their respective economic conditions, regulatory frameworks, and currency strengths. These nations not only provide significant opportunities for Forex traders but also play a crucial role in shaping the future of international finance and trade.

In the fast-paced world of Forex trading, where fortunes can be made or lost in the blink of an eye, the importance of selecting the right trading approach cannot be overstated.

Today, over 70% of traders rely on algorithmic trading methods, as revealed by the research report “Predictive Assessment of Electronic Trade Dynamics: 2022-2027“. This staggering statistic underscores the prevalence and influence of algorithmic trading in the contemporary financial landscape.

Understanding the nuances of both manual and algorithmic trading is crucial for non-professional traders to navigate these complexities successfully. Let’s delve into these approaches, exploring their intricacies and uncovering the key considerations that can shape the success of Forex trading.

Manual Trading: The Art of Hands-On Decision-Making

Involving a traditional, hands-on approach where traders rely on intuition and market analysis, manual trading provides a unique learning experience and enables the exercise of emotional control.

This method offers a practical learning environment, allowing traders to engage directly with the market. For instance, envision a trader meticulously analysing historical price charts, identifying key support and resistance levels, and anticipating a trend reversal based on a combination of technical indicators and economic factors.

Actively participating in decision-making processes, manual trading helps traders develop emotional control – a crucial aspect of success. Consider a scenario where a trader, faced with a sudden market downturn, resists the impulse to panic sell and instead relies on their analysis to make rational decisions, avoiding potentially significant losses.

However, manual trading has its challenges. The time-intensive nature demands constant attention, making it challenging for traders with busy schedules. Emotional challenges remain prevalent, and the limited capacity for multitasking can hinder a trader’s ability to seize multiple opportunities simultaneously.

To illustrate, imagine a manual trader who, after studying market conditions, identifies a potential breakout in a currency pair. This trader monitors the charts, patiently waiting for the opportune moment to enter the market. When the anticipated reversal occurs, the trader executes a well-timed trade, capitalising on insights gained through hands-on analysis.

In essence, manual trading offers a personalised and engaging experience for traders willing to invest time and effort into understanding the intricacies of the Forex market. While it requires discipline and focused attention, the skills acquired through manual trading can be invaluable for those seeking a deep connection with their trading strategies.

Algorithmic Trading: The Precision of Automated Decision-Making

In stark contrast to manual methods, algorithmic trading relies on automated execution and data-driven decisions, emphasising speed, efficiency, and systematic strategy application.

Algorithmic trading excels in speed and efficiency, processing vast market data in milliseconds. An example is an algorithm identifying and capitalising on price discrepancies across markets, executing trades instantaneously.

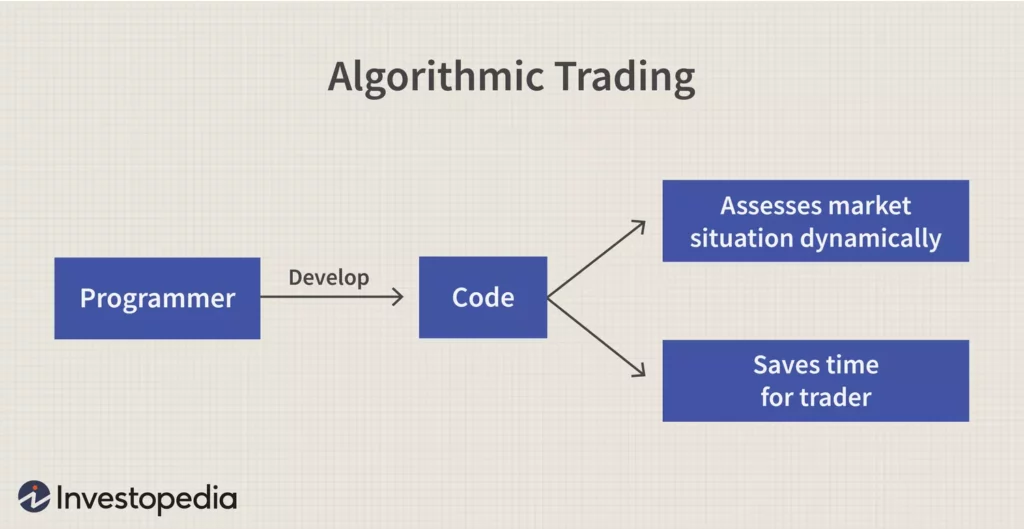

Algorithmic trading model source: Investopedia

Crucial to algorithmic trading, backtesting validates strategies using historical data, minimising the risk of flawed analysis. Imagine a trader developing an algorithm identifying profitable trends through historical price movements, ensuring viability before live application.

Despite its advantages, algorithmic trading has complexities. A steep learning curve demands proficiency in programming and data analysis. Over-reliance on historical data poses risks, as strategies may lose effectiveness in rapidly changing markets.

Consider a trader developing a sophisticated algorithm with machine learning techniques, allowing anticipation of price movements accurately and consistently yielding profits by adapting to evolving market conditions.

Algorithmic trading comes with risks, including system failures and technical challenges. Traders must be vigilant to address potential issues promptly, as glitches or failures could lead to unintended consequences.

In essence, algorithmic trading offers an efficient, systematic approach to Forex trading. Despite technical demands and potential risks, a well-designed algorithm has the potential to unlock consistent profits in the ever-evolving financial landscape.

Factors to Consider: Choosing Between Manual and Algorithmic Trading

When faced with the decision between manual and algorithmic trading, a careful evaluation of several key factors can significantly impact your trading journey.

Factor 1.Risk Tolerance:

Manual Trading: Ideal for those comfortable with risk, offering flexibility and adaptability.

Algorithmic Trading: Suited for risk-averse individuals, providing a disciplined and controlled approach.

Factor 2.Time Commitment:

Manual Trading: Demands constant attention and time investment.

Algorithmic Trading: Offers automation, saving time for exploring opportunities and strategy refinement.

Factor 3.Skill Level:

Manual Trading: Requires a deep understanding of market dynamics and analysis.

Algorithmic Trading: Involves programming and data analysis skills.

In summary, align your trading approach with your risk tolerance, time commitments, and skill set to make an informed decision between manual and algorithmic trading.

For example, a computer science-savvy trader might excel in algorithmic trading, leveraging programming skills. Meanwhile, a trader attuned to market psychology may find success in manual trading.

Each method has unique benefits, ensuring a strategic fit for your preferences and enhancing your success in Forex trading.

Combining Manual and Algorithmic Trading: The Power of Hybrid Strategies

As technology and trading methodologies evolve, the concept of hybrid trading has emerged as a compelling strategy for traders seeking the best of both worlds. By combining manual and algorithmic approaches, traders can capitalise on the strengths of each method, creating a versatile and adaptive trading strategy.

source: Freepik

Intuitive Decision-Making with Efficiency

Hybrid trading combines manual intuition with algorithmic efficiency. Traders leverage the strengths of both approaches – making informed decisions based on market understanding while benefiting from the speed and precision of automated execution.

Risk Management at the Core

Central to hybrid trading is robust risk management. Traders can swiftly adapt to changing market conditions by switching between manual and algorithmic modes. This dynamic approach enhances risk mitigation, allowing traders to navigate diverse market scenarios with agility.

A trader, combining economic insight with sentiment analysis algorithms, may switch between manual and algorithmic modes based on market events. This adaptability ensures critical decision-making during unexpected situations.

Continuous Adaptation and Learning

Hybrid traders embrace continuous adaptation and learning. The synergy between manual and algorithmic methods enables real-time strategy refinement, crucial in the ever-changing Forex market.

Optimising Strengths, Minimising Weaknesses

By combining manual and algorithmic trading, traders aim to optimise strengths while mitigating weaknesses. Manual trading adapts to unique market conditions, while algorithmic trading provides efficiency in executing predefined strategies.

VT Markets welcomes traders of all styles, whether engaging in manual or algorithmic trading.

For manual traders, the user-friendly interfaces of MT4, MT5, and WebTrader Plus ensure a seamless and intuitive experience across Forex, indices, commodities, and other assets. Execute trades with precision and efficiency, empowered by real-time data and analytical tools.

Alternatively, for those who prefer automated strategies, leverage the platform’s compatibility with expert advisors. Implement finely-tuned algorithmic approaches tailored to the nuances of your preferred instrument and aligned with unique trading objectives.

In conclusion, both manual and algorithmic trading have their merits and drawbacks. Forex traders should explore both approaches, considering factors such as risk tolerance, time commitment, and skill level. Embracing a hybrid strategy and leveraging the tools and opportunities provided by platforms like VT Markets can empower traders to navigate the Forex market successfully. Continuous learning and adaptation are key in this ever-evolving financial landscape.

Summary:

Manual trading and algorithmic trading are two primary approaches to engaging in financial markets.

Manual trading involves hands-on decision-making but faces challenges like time intensity.

Algorithmic trading relies on automated execution but has a steep learning curve.

Hybrid trading, blending manual intuition with algorithmic efficiency, is gaining popularity.

Consider your risk tolerance, time commitments, and skill set when choosing between manual and algorithmic trading in Forex.

The stock market soared to record highs as the Dow Jones Industrial Average closed at 37,248.35 points, marking a 0.43% increase, spurred by a drop in the 10-year Treasury note yield. This surge resonated in the S&P 500 and Nasdaq, both climbing upwards. Investor confidence in a potential soft economic landing for 2024 grew, with speculation about forthcoming rate cuts, especially after the Federal Open Market Committee hinted at possible reductions. Specific sectors, including solar stocks and Moderna, experienced substantial gains. Additionally, sectors like Energy and Real Estate thrived, while Utilities and Consumer Staples saw declines. In the currency market, the dollar index dropped significantly as the Bank of England and the European Central Bank diverged from the Federal Reserve’s dovish stance, influencing currency pairs like EUR/USD and Sterling, while USD/JPY faced downward pressure amidst expectations surrounding major central banks’ policies.

Stock Market Updates

The stock market experienced a positive surge as the Dow Jones Industrial Average hit a record high, closing up by 0.43% at 37,248.35 points, following its previous milestone above 37,000. This increase was mirrored by the S&P 500, which rose by 0.26% to 4,719.55, and the Nasdaq Composite, which gained 0.19% to 14,761.56. These upticks were propelled by the 10-year Treasury note yield dropping below 4%, leading to increased investor confidence in a potential soft economic landing for 2024. This drop in interest rates spurred speculation about potential rate cuts for the upcoming year, with the Federal Open Market Committee indicating the possibility of three rate reductions.

Additionally, specific sectors saw notable movements. Solar stocks, including SunRun and Enphase, surged as the 10-year Treasury yield fell, with the Invesco Solar ETF (TAN) climbing over 8.1%. Moderna’s shares also rose by 9.3% after trial data revealed promising results for its cancer vaccine used in conjunction with Merck’s Keytruda. Looking ahead, the S&P 500 inches closer to its all-time closing record set in January 2022, sitting just 1.6% away, while the Nasdaq remains approximately 8% below its closing record and 9% from its intraday peak.

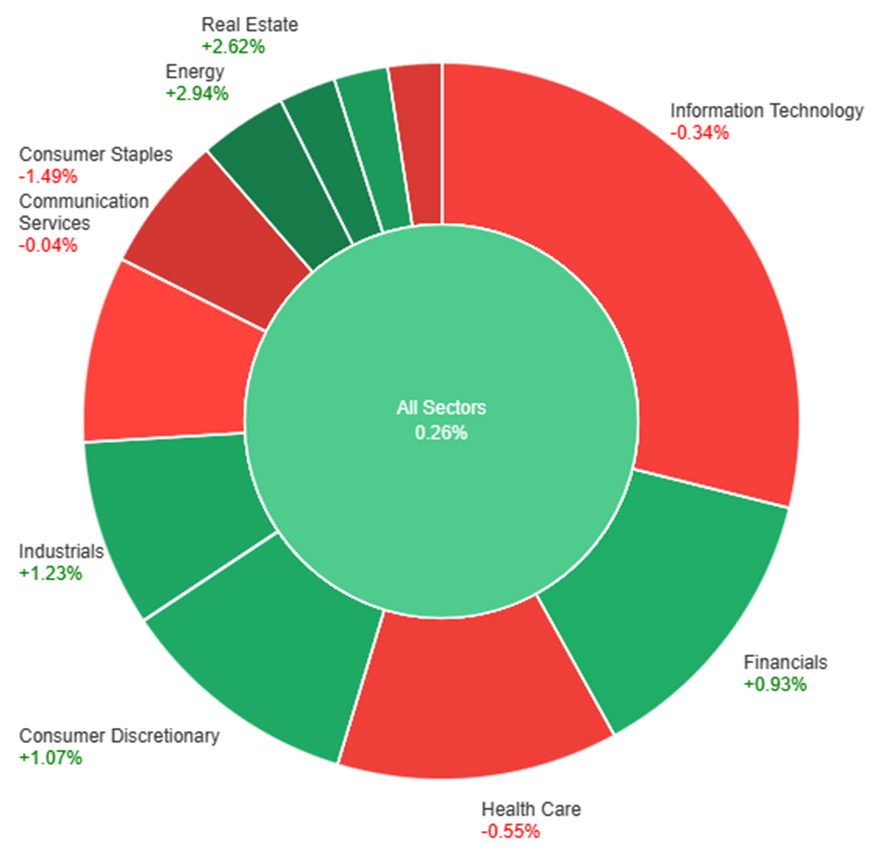

On Thursday, the overall market showed a positive trend, with a gain of 0.26%. The standout performers were Energy and Real Estate, surging by 2.94% and 2.62%, respectively. Materials and Industrials also experienced notable gains, rising by 1.68% and 1.23%. However, sectors like Utilities and Consumer Staples saw declines, with decreases of 1.28% and 1.49%, respectively. Communication Services remained relatively stable, showing a marginal decrease of 0.04%. Notably, Information Technology and Health Care experienced declines of 0.34% and 0.55%, respectively, contributing to the overall mixed performance across sectors.

Currency Market Updates

In the currency market updates, the dollar index faced a significant decline by 1% after the Bank of England (BoE) and the European Central Bank (ECB) chose not to mirror the Federal Reserve’s dovish stance. This highlighted a trend where the U.S. central bank consistently leads major policy shifts during the pandemic. Despite a brief rebound in the dollar following positive U.S. retail sales and jobless claims, this momentum was overshadowed by the divergence between the Fed’s dovishness and the BoE and ECB’s reluctance to consider easing.

The BoE maintained elevated rates due to UK core inflation at 5.7%, substantially higher than the central bank’s target, while the ECB’s 4% rate remained notably lower compared to the BoE and Fed. Market futures now anticipate the Fed’s first rate cut in March, accumulating to 150 basis points by 2024. On the other hand, the ECB is slightly predicted to cut rates by March, aiming for nearly 150 basis points by year-end. The BoE is expected to cut rates by May, albeit by 106 basis points for 2024. Amidst this, currency pairs like EUR/USD surged by 1%, nearing November’s trend high, while Sterling rose by 1.36%, driven by the BoE’s resistance to rate cut expectations and benefited from risk-on flows.

USD/JPY experienced a decline from November’s peak, reaching 140.95 after the Fed’s pivot and ahead of crucial announcements from the BoE, ECB, and U.S. retail sales. Despite a retracement to 140.71, USD/JPY faced downward pressure, partly attributed to the expectation that the Bank of Japan (BoJ) stands alone among major central banks in considering a hike next year.

The EUR/USD pair experienced a surge, hitting 1.1009 before a minor pullback, driven by contrasting central bank actions. The US Dollar faced pressure post-Fed, while the Euro gained ground following the ECB’s decision to maintain rates and continue PEPP reinvestments through H1 2024, with plans to reduce the portfolio by €7.5 billion monthly in H2. Despite expectations of a gradual inflation decline till 2024 and concerns over price pressures, ECB President Christine Lagarde clarified no discussions on rate cuts occurred. Additionally, the Dollar’s slide was compounded by a drop in Treasury yields. While positive US data on Retail Sales and Jobless Claims surpassed expectations, the focus remains on Friday’s release of S&P Global’s preliminary December PMIs for the EU and the US.

On Thursday, the EUR/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential continuation movement, potentially reaching the resistance level at 1.1017. Notably, the Relative Strength Index (RSI) maintains its position at 77, signaling a bullish outlook for this currency pair.

Resistance: 1.1017, 1.1060

Support: 1.0963, 1.0912

XAU/USD (4 Hours)

XAU/USD Hold Steady Amidst Dollar Respite and Central Bank Divergence

Gold (XAU/USD) navigates a week of fluctuations, poised for a weekly gain after a retreat from record highs. The Asian market’s influence is marked by the US Dollar’s pause in its decline, propelled by a slight rebound in US Treasury bond yields. Amidst this, the US Dollar finds stability as Asian stocks trim early gains, awaiting pivotal preliminary PMI data from the US and Eurozone, crucial for gauging global economic health. The backdrop is a US Federal Reserve embracing a dovish stance, contrasting with the Bank of England and European Central Bank hinting at potential tightening, revealing a pronounced monetary policy divergence that weighs heavily on the dollar. Despite temporary Dollar recoveries due to unexpected US Retail Sales upticks, the dovish Fed outlook continues to fuel a global risk-on sentiment, supporting Gold prices near recent highs. As the week concludes, the focus remains on the PMI data’s impact and potential profit-taking amid a volatile week dominated by central bank actions.

On Thursday, XAU/USD moved in consolidation around the upper band of the Bollinger Bands. Currently, the price moving below the upper band, suggesting a potential continuation movement, potentially reaching the resistance level at $2,041. The Relative Strength Index (RSI) stands at 64, signaling a bullish outlook for this pair.