The US will release the Non-Farm Employment Change and FOMC Meeting Minutes this week.

The Non-farm Employment Change is expected to show a total of 220,000 jobs added in December, down from the 263,000 jobs added in November. Forecasters also expect the Unemployment Rate to remain unchanged at 3.7%.

Meanwhile, the Minutes from the Federal Open Market Committee will shed further light on policy intentions going forward.

Here are the key market events for the week ahead:

Swiss Consumer Price Index (4 January)

The Consumer Price Index in Switzerland stood at 0% in November of 2022, unchanged from the previous month.

Analysts expect the index to decrease by 0.3% in December.

US ISM Manufacturing PMI (4 January)

The US Institute for Supply Management’s Manufacturing Purchasing Managers Index fell to 49 in November 2022 from 50.2 in October, its first contraction since May 2020.

Analysts expect the index to remain at 49.

US JOLTS Job Openings (4 January)

US job openings dropped by 353,000 to 10.3 million in October 2022, according to the JOLTS report. This may indicate that demand for workers has started to slow amid a softer economic forecast and higher interest rates.

Analysts expect that the number of available jobs will decrease more in November to 10.1 million.

FOMC Meeting Minutes (5 January)

In its last monetary policy meeting of 2022, the Federal Reserve raised the fed funds rate by 50bps to 4.25%-4.5%. This was its seventh consecutive rate hike.

The Fed expects that interest rates would reach 5.1% in 2023, 4.1% in 2024, and 3.1% in 2025.

ADP Non-Farm Employment Change (5 January)

The US private sector added only 127,000 jobs in November of 2022, below economists’ expectations.

Economists expect ADP Non-Farm to create another 150,000 jobs in December.

Canada Employment Change (6 January)

In November 2022, 10,100 jobs were added to the Canadian economy, while the unemployment rate stood at 5.1%, decreasing from the previous month’s rate of 5.2%.

Analysts predict that employment will grow by an additional 60,000 positions over the next month, with the unemployment rate to stand at 5.2%.

US Non-Farm Employment Change (6 January)

The US non-farm payrolls report for November showed an increase of 263,000 jobs following a downwardly revised 284,000 gain in October. The unemployment rate was unchanged at 3.7%, close to September’s 3.5%.

Analysts expect the unemployment rate to remain unchanged at 3.7% while non-farm payrolls will increase by 220,000 for December.

US ISM Services PMI (6 January)

The US Institute for Supply Management’s Services Index jumped to 56.5 in November from 54.4 in October. It is expected to decline slightly to 53 in December.

American markets start trading today. Before Asia opened, U.S. equity futures surged. An economic data-packed week will start the year. ADP and the Department of Labor will report nonfarm employment change and first jobless claims during the late American trading session on the fifth. The December U.S. nonfarm payrolls and unemployment rate will be noted on December 6. German and EU CPI for December will be released on December 6, respectively.

In 2022, all three major U.S. market indices performed worst since 2008. Dow Jones Industrial Average dropped 8.8% to 33147.25. S&P 500 fell 19.4% to 3839.5. Nasdaq plummeted 33.1% to 10466.88. Inflation and central bank tightening have caused one of the most volatile equity markets in recent years. Late-cycle economic activity—tight labour markets, increasing inventories, declining profit margins, and most importantly, tighter monetary policy—indicates an even gloomier investment climate for 2023.

Geopolitical conflicts will drive market action in 2023. Since March 2022, the Russia-Ukraine conflict has persisted. The Kremlin has faced unprecedented Western punishment for shelling Kyiv and other Ukrainian cities. The eight-month battle has disrupted supply chains, raising commodity prices, and weakened international relations. A resolution between the two countries will affect Eastern Europe’s economy and the Euro.

Main Pairs Movement

On the very first trading day of 2023, the Dollar index did not make the market surprised with huge floating based on last Friday’s close price. Instead, it failed to start in a positive way to 2023 as the DXY remained under pressure during the early Asian session on Monday near a seven-month low, which was near 103.40 by now.

EURUSD lost some vantages on the first trading day of 2023 due to thin liquidity conditions in the financial markets. It fell around 0.32% and closed at around 1.06640 price level. The release of S&P Global PMIs in the Eurozone on Monday failed to support the shared currency.

GBPUSD extends its daily slide trend, failing to keep price above 1.2050 of the closing price during Monday’s trading course. Amid thin trading conditions on the observed New Year holiday, the pairs’ losses remain limited for the time being.

Gold price settled around 1823.00 on last Friday after failing to surpass the same resistance despite a sell-off in the DXY. The precious metal delivered a gradual upside move from the psychological support of $1,800.00 after sheer pain in the USD Index.

Technical Analysis

EURUSD (4-Hour Chart)

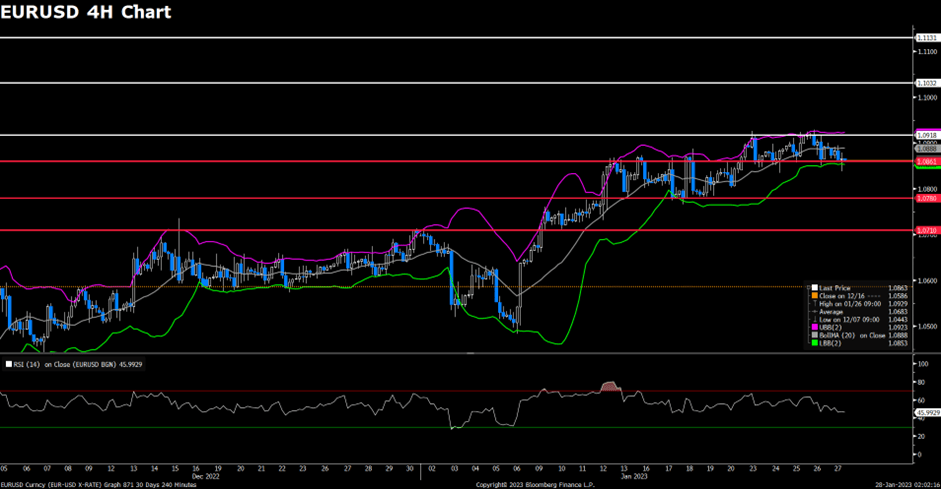

The EUR/USD pair edged lower on Monday, remaining under bearish pressure and continued to trade in a tight channel below 1.0700 as trading conditions remain thin with major markets remaining closed during the New Year holiday. The pair is now trading at 1.0667, posting a 0.31% loss daily. EUR/USD stays in the negative territory amid holidays in the global markets, despite the downbeat prints of the US data has dragged the US Dollar Index (DXY) to refresh a seven-month low the previous day. On the economic data front, Wednesday’s latest FOMC meeting minutes and Friday’s December month employment numbers for the US will both be crucial for the EUR/USD traders to watch. In the Eurozone, the hawkish comments from ECB President Christine Lagarde failed to support the EUR/USD pair as Germany’s Finance Minister Christian Lindner expects that inflation in Europe’s biggest economy to drop to 7% this year and continue falling in 2024.

For the technical aspect, RSI indicator 51 figures as of writing, suggesting that the pair could experience some downside momentum as the RSI is falling towards 50. As for the Bollinger Bands, the price witnessed fresh selling and dropped to the moving average, therefore the downside traction should persist. In conclusion, we think the market will be bearish as the pair is heading to test the 1.0660 support line. On the upside, the case for recovery will be firmer if the pair extends gains above 1.0710.

Resistance: 1.0710

Support: 1.0660, 1.0584, 1.0467

GBPUSD (4-Hour Chart)

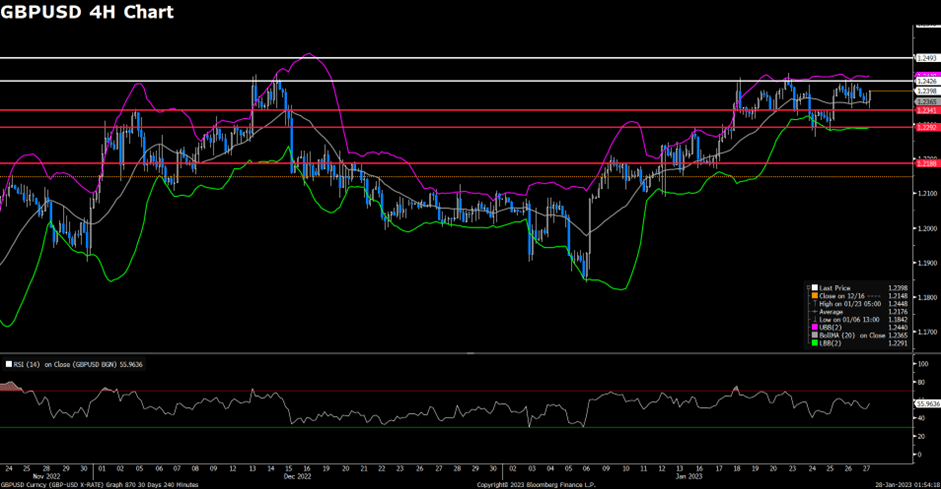

The GBP/USD pair declined on Monday, coming under modest bearish pressure and stretched lower to the 1.2050 area amid a cautious market mood on the first trading day of 2023. At the time of writing, the cable stays in negative territory with a 0.36% loss for the day. Investors grow increasingly concerned over the impact of the surging number of coronavirus cases in China on global economic activity as the country stays on the reopening path. For the British pound, British Prime Minister (PM) Rishi Sunak shelved the plans for a major overhaul of the childcare system aimed at saving parents money and helping them return to work. Moreover, British ministers think UK labour unions will run out of money and have to back down but the unions reject the claim. Therefore, the British labour strike and UK PM Sunak’s pushback to childcare reform join geopolitical concerns to exert bearish pressure on the GBP/USD pair.

For the technical aspect, RSI indicator 44 figures as of writing, suggesting the bearish traction will remain in the near-term technical outlook as the RSI stays below the mid-line. As for the Bollinger Bands, the price preserved its downside traction and dropped below the moving average, therefore a continuation of the bearish trend can be expected. In conclusion, we think the market will be bearish as long as the 1.2095 resistance line holds. A four-hour close above that level could open the door for additional gains and favour the bulls.

Resistance: 1.2095, 1.2212, 1.2334

Support: 1.2012, 1.1942

USDCAD (4-Hour Chart)

Despite most markets remaining closed on the observance of the new year’s holiday on Monday, the pair USD/CAD witnessed some upside momentum and climbed to a daily top around the 1.3580 mark in the early US trading session. USD/CAD is trading at 1.3572 at the time of writing, rising 0.23% daily. the lack of US and Canadian economic data keeps traders leaning on market mood and technicals. Investors now shift their focus to the S&P Global Manufacturing PMIs for both countries, with Canada’s PMI expected to drop to 49.2, below the previous month’s reading of 49.6. On top of that, the fears of easing demand, which is mainly due to the Covid fears emanating from China, might limit the upside for the crude oil prices and undermine the commodity-linked loonie. Looking forward, holidays in multiple markets could restrict the USD/CAD intraday moves.

For the technical aspect, RSI indicator 54 figures as of writing, suggesting the pair’s indecisiveness in the near term as the RSI indicator hovers around the mid-line. For the Bollinger Bands, the price regained some upside strength and climbed above the moving average, therefore a continuation of the upside trend could be expected. In conclusion, we think the market will be slightly bullish as long as the 1.3529 support line holds. The rising RSI also reflects bull signals as the oscillator has exited from the bearish territory.

US stocks rose in a broad-based rally and Treasury yields fell as data allayed fears of a supercharged jobs market that would support a more aggressive policy path. A gauge of the dollar fell. Investors took solace in US jobs data that failed to reveal unwanted surprises while underscoring the resilience of the labour market in the face of the Federal Reserve’s aggressive monetary tightening. Initial unemployment claims rose slightly to 225,000, in line with expectations, in the week ended Dec. 24.

Continuing claims rose to 1.7 million in the week ended Dec. 17, the most since early February. The rally is a ray of light as a dismal year for stocks and bonds draws to a close. Global equities have lost a fifth of their value in 2022, the largest decline since 2008 on an annual basis.

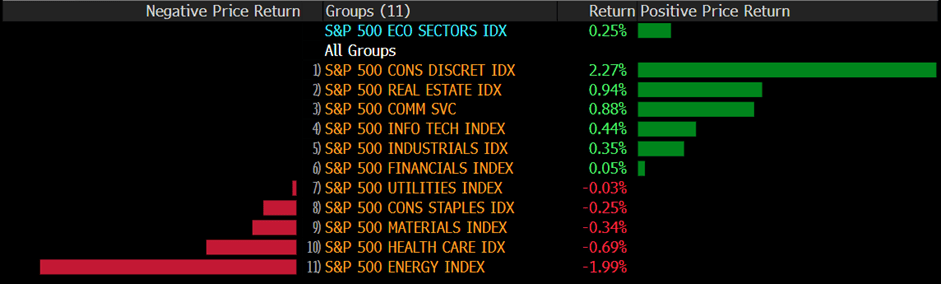

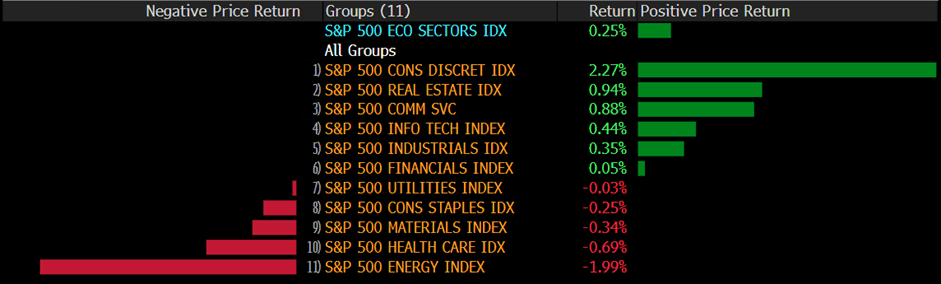

The benchmark, the S&P500 rallied with a 1.75% daily gain on Thursday. All eleven sectors in S&P500 stayed in the positive territory, with the Communication Service and Information technology section performing the best among all groups, rising 2.69% and 2.64% respectively for the day. Apart from this, the tech-heavy Nasdaq 100 outperformed, surging by 2.54% on a daily gain.

The US Dollar slid with 0.49% daily losses on Thursday, as US data showed the resilience of the labour market. The DXY index suffered heavy selling pressures all day, touching a daily low level below 103.8.

The GBPUSD edged higher with 0.31% daily for the day, as a decent recovery in the risk appetite theme. The pair regained mildly positive momentum in the late UK trading session, ending around the 1.2045 level. Meanwhile, the EURUSD witnessed fresh transactions since European trading hours and touched a daily high level of 1.069. The pair ended the day with a 0.46% daily gain.

The gold surged by 0.59% daily on Thursday, as the greenback stayed on the back foot, which provide support for the dollar-denominated yellow metal. The XAUUSD gained upside traction during the late European session, once reaching a daily high of $1820 marks in the middle of US trading hours.

Technical Analysis

EURUSD (4-Hour Chart)

EURUSD raised $0.0049 and edged higher around 0.46% throughout Thursday’s trading. The EUR is holding gains against the dollar as market sentiment improves ahead of the final trading day of 2022. Data from the US showed a slight increase in jobless claims, boosting EUR/USD, while China’s Covid-19 easing made investors nervous. In other places, Russia’s invasion of Ukraine has escalated with a news report of the shelling of Kyiv and other cities.

Meanwhile, the Eurozone economic calendar saw Spanish retail sales jump 3.8% month-over-month over the previous month’s 0.4%, while EU M3 money supply jumped to 4.8% year-over-year in November versus expectations of 5%.

On the technical side, EUR/USD is still trading unstable, as usually happened in the last ten days of trading of the year. However, the RSI indicators show that the common currency could start the new year at a higher as the RoC is flat. RSI for the pair sits at 64.52, as of writing. On the four-hour chart, EURUSD currently trades above its 50, 100, and 200-day SMA.

Resistance: 1.0695, 1.0736

Support: 1.0585, 1.0459

GBPUSD (4-Hour Chart)

The Pound remains sideways during the North American session after hitting a daily low of $1.2005 against the US dollar. However, the cable slightly raised by 18 pips after US initial jobless claims data was released on the 30 minutes chart. As of writing, the price sitting at $1.20707, raised around 0.45% in today’s trading course. On Friday, the UK economic docket is empty, while the US calendar will feature the Chicago PMI for December, estimated at 40.

On the other side, the GBP/USD is motivated by the US dollar due to the lack of UK economic data. The DXY a gauge that tracks the greenback value of a packet of six currencies tumbles 0.5% down to $103.8 as of writing. Weighed by falling US treasury yields. The US 10-year benchmark note rate drops 3.0 basis points to 3.85%.

On the technical side, from the daily chart, the GBP/USD upside was restricted by the 20 and 200-day EMA, each at $1.12111 and $1.2082. The RSI and RoC indicate that the cable is edging up, even though the short-side sellers are beginning to gather momentum. From the four-hour chart, the price level sits above the descending regression channel and is close to 20-day SMA. RSI for the pair sits at 54.74, as of writing. On the four-hour chart, GBPUSD currently trades above its 50, and 100-day SMA and just crossed its 200-day SMA.

Resistance: 1.2320, 1.2600

Support: 1.19, 1.176

XAUUSD (4-Hour Chart)

Gold price raised over 0.8% to $1,820 during today’s trading course as of writing. As US 10-year treasury yields edge lower 3.0 basis points to 3.85%, probes the DXY bulls and puts a floor under the gold price. Also, the US weekly initial jobless claims-related data with 225K meet markets’ expectations. Which gave the investors the belief that the Fed may ease the fighting strength against inflation, leading the greenback to devaluation, and DXY falls over 0.5% down to $103.8 as of writing.

On the other hand, should keep an eye on China’s Zero-Covid policy, as around seven major nations have recently announced Covid test requirements for Chinese travellers as the virus cases swirl in the dragon nation. a top official from the Chinese Center for Disease Control and Prevention recently warned of Covid spreading throughout the holiday season. The diplomat, however, also mentioned that the covid virus outbreaks have peaked in Beijing, Tianjin and Chengdu.

On the technical side, a three-week-old ascending triangle restricts Gold prices between $1,782 and $1,825. That means the XAU/USD currently fades bounce off a fortnight-old upward-sloping support line inside the stated triangle. RSI sits at 59.21 as of writing. On the four-hour chart, gold price trades above its 50, 100, and 200-day SMA.

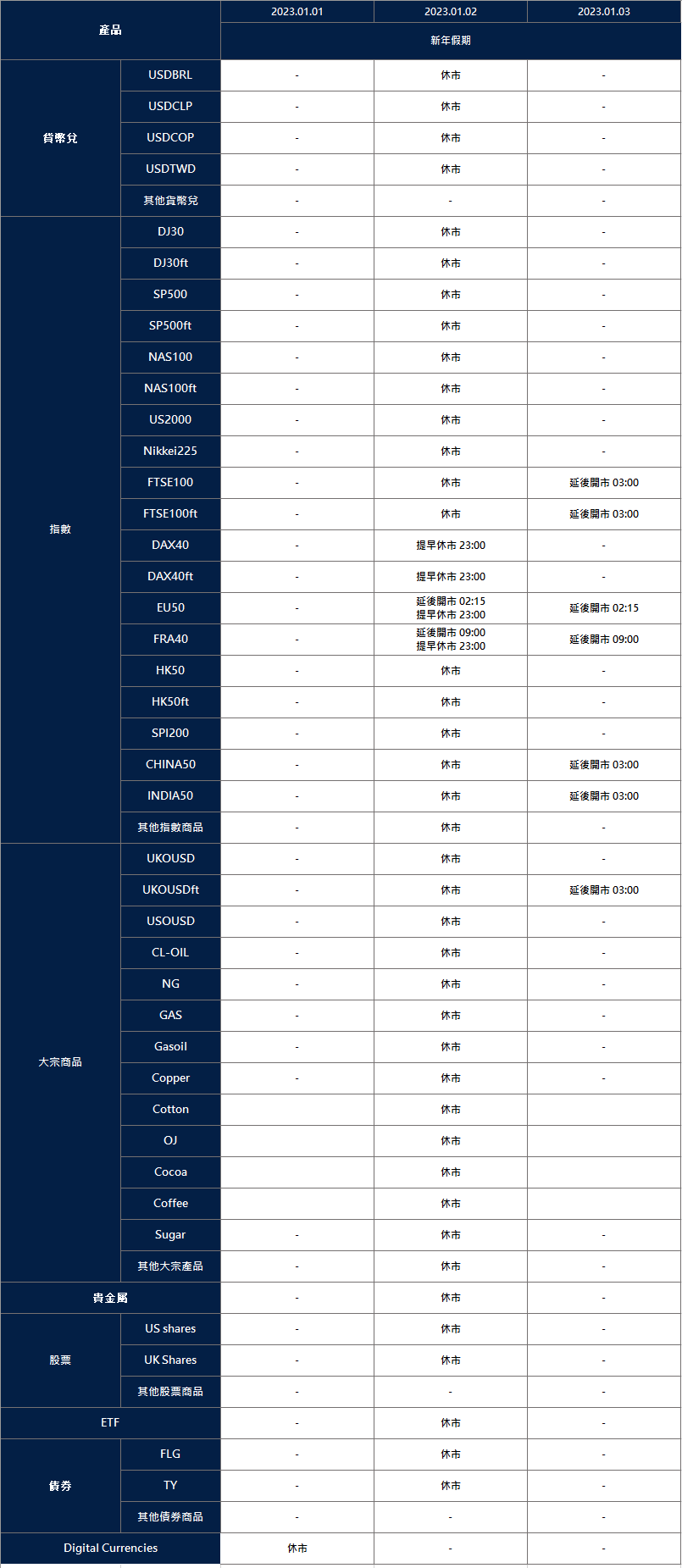

Please note that when constituent stocks of a market index generate dividends, VT Markets will make dividends and deductions for clients who hold the products after the close of the day before the ex-dividend date.

The dividends will not be paid/charged as an inclusion along with Swap. It will be executed separately in your account and the record will be annotated as “Div & Product Name & Net Volume”.

Please note the specific adjustments as follows:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

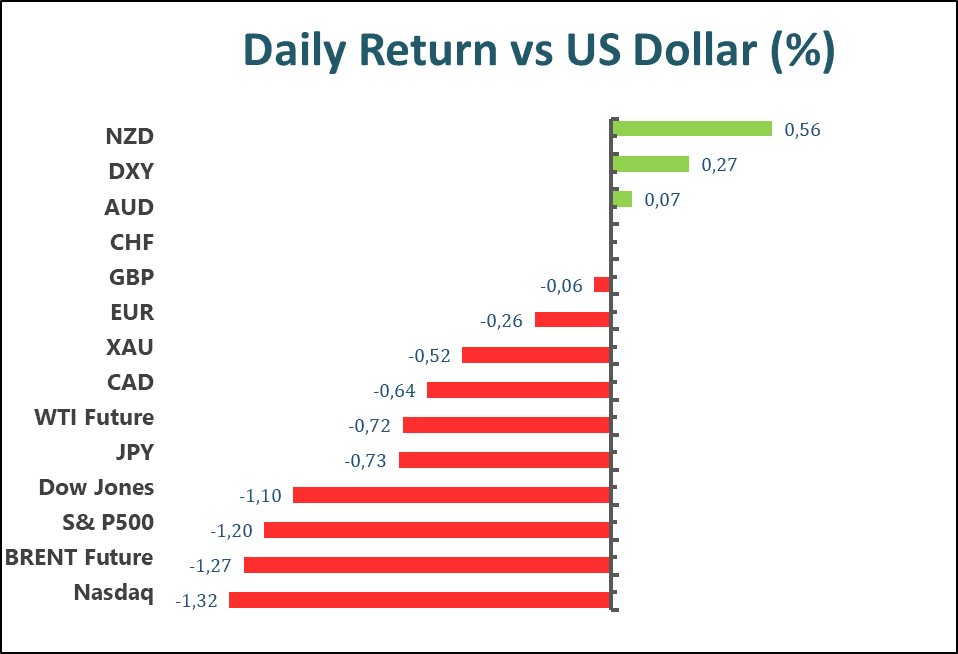

US stocks were dragged lower for a second day, as stocks in Asia headed for declines on Wednesday with fresh concerns about the spread of Covid-19 from China unnerved investors. Market appetite for risk waned on news that the US would require inbound airline passengers from China to show a negative Covid-19 test before entry.

In Italy, health officials said they would test arrivals from China and said almost half of passengers on two flights from China to Milan were found to have the virus. However, Hong Kong removed limits on gatherings and testing for travellers in a further unwinding of its last major Covid rules, offering a boost to the global economy but sparking concerns it would amplify inflation pressures and prompt US policymakers to maintain tight monetary settings.

The benchmarks, the S&P500 dropped 1.2% for the day, to the lowest level in more than a month. All eleven sectors stayed in the negative territory, especially the Energy sector fell dramatically with 2.22% daily losses after the several-day surge. The tech-heavy Nasdaq 100 further declined by 1.3% daily, and the Dow Jones Industrial Average slid 1.10% on Wednesday.

Main Pairs Movement

The US Dollar edged higher with a 0.27% daily gain on Wednesday, as the concerns about the outbreak of Covid-19 from China attracted some risk-aversion flow to the safe-haven greenback. The DXY index confronted some mild selling during the first half of Wednesday, then managed to rebound above the 104.4 level during the US trading session.

The GBPUSD has little change lower for the day, as the strong US Dollar is across the board. The cables dropped hugely during the early American trading session as the US administration announced mandatory Covid tests for travellers from China. In the meantime, EURUSD tumbled by almost 0.36% undermining market risk sentiment. The pair ended the day with 0.26% daily losses.

The Gold price remains defensive around the $1805 mark after printing the first daily negative closing in three, as the market’s fresh fears of inflation, emanating from China, as well as geopolitical tension surrounding Russia and Ukraine, which in turn provide support for US Treasury bond yields and the greenback. The XAUUSD slumped during the UK trading hour and once fell below the $1800 mark, then regain upside momentum and stand firmly around the $1805 mark.

Technical Analysis

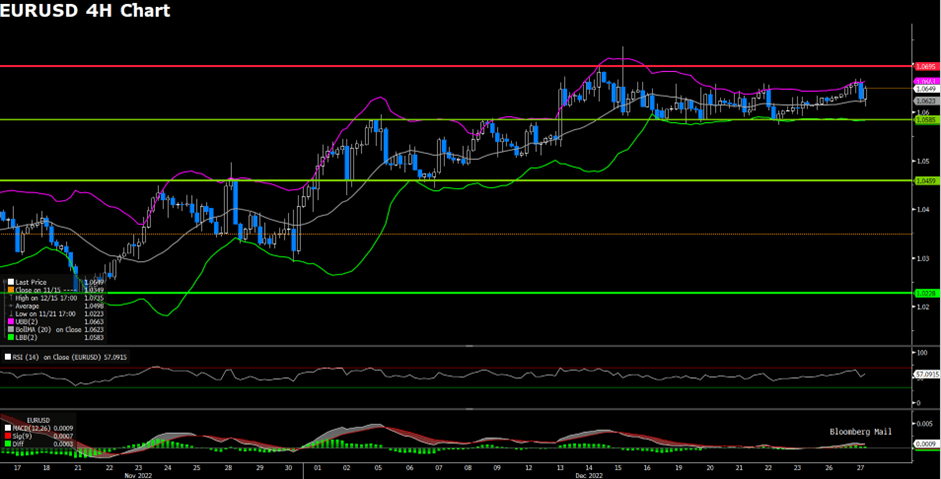

EURUSD (4-Hour Chart)

EURUSD edged lower throughout Wednesday’s trading and could not extend the pair’s three-day winning streak. The Euro-Dollar pair witnessed large volatility at the start of the American trading session as the Dollar dipped before starting an impressive rally that altered the course of EURUSD. The renewed Dollar strength comes after U.S. equities continue to sell off as the year comes to a close. Market participants are looking for safety as both equities and bonds continue to lose ground since trading began after the holidays. The benchmark U.S. 10-year treasury yield is now trading above the 3.87% mark, while the 2-year treasury yield was last seen trading at 4.357%. Yield curve inversion, often seen during late-cycle economies, will continue to be the norm as global economies head into a grim 2023. The nature of late-cycle economies could favour the U.S. Greenback in 2023 as global market participants look to protect asset valuations.

On the technical side, EURUSD has continued to trade below our previously estimated resistance level of 1.0695. Short-term support remains at 1.0585 and 1.04591. RSI for the pair sits at 61.97, as of writing. On the four-hour chart, EURUSD currently trades above its 50, 100, and 200-day SMA.

Resistance: 1.0695

Support: 1.0585, 1.0459

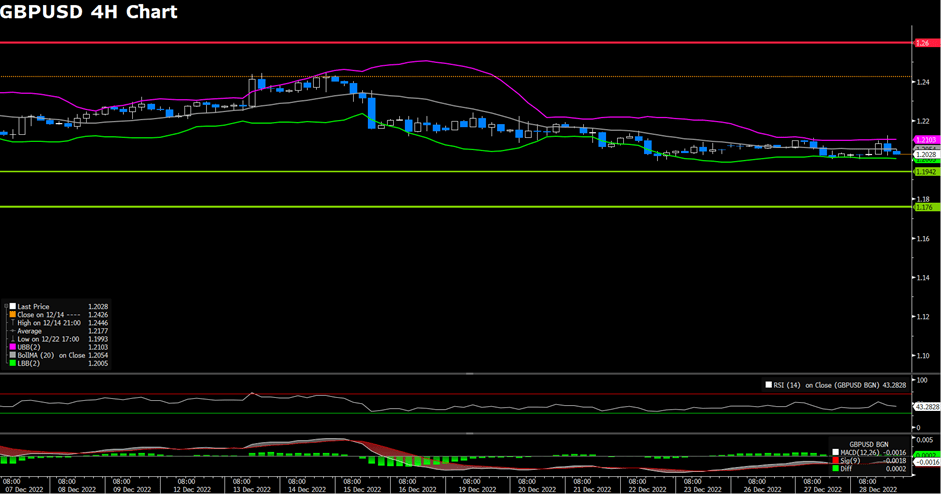

GBPUSD (4-Hour Chart)

The pound rose sharply after a choppy European session, rebounding from an intra-day low near $1.2000 to challenge the $1.2100 figure in the American session. China is lifting Covid-19 restrictions on tourists, while it has started issuing travel permits to Hong Kong residents. In addition, authorities are starting to issue passports and will officially reopen the border on Jan. 8. Even though sentiment has turned positive, concerns about rising inflationary pressures are keeping traders on their toes. the U.S. Dollar Index, which measures the value of the greenback against a basket of peers – was down 0.28% at 103.984, weighed down by lower yields on U.S. Treasuries. There are no particular market events by this week for the UK.

Looking at the daily chart, GBP/USD is testing the 20 and 200-day EMA at 1.2113 after bouncing off the weekly lows near 1.2000. If the former is cleared, nest resistance would be the previous support-transfer-resistance of the uptrend line near 1.2180, followed by the 1.2200 figure. Conversely, failure to stay above 1.2100 could pave the way towards the weekly low at 1.2000 and the 50-day EMA at 1.1935. RSI for the pair sits at 48.71, as of writing. On the four-hour chart, GBPUSD currently trades above its 50, 100 day SMA but above its 200-day SMA.

Resistance: 1.2320, 1.2600

Support: 1.19, 1.176

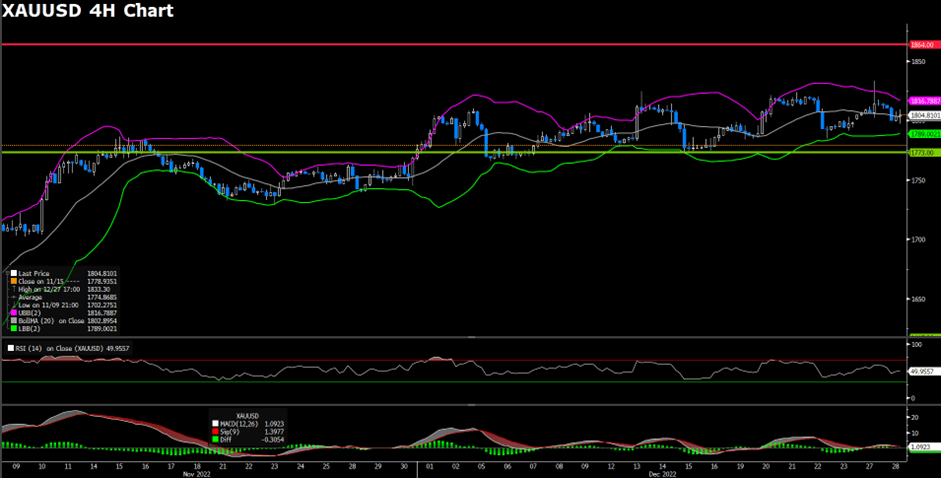

XAUUSD (4-Hour Chart)

XAUUSD gave back gains after surging higher on Tuesday and fell further on Wednesday, basically having spit out all gains so far. The prices edged lower by nearly 1% to the lowest price at $1,797 during the American trading session. It is hovering around $1,800 with bearish trends. As the price broke through the last estimated support of $1,812 and $1,800, it would make gold vulnerable to a decline to test an uptrend line around $1,795. A break below could trigger more losses, to the $1,785 zone. Below the next support is located at $1,773, which is Dec 15 & 16 low. As equity prices in Wall Street turned negative and amid a rebound in US yields to fresh daily highs, and the US Dollar Index rose from the lowest level in almost a week at 103.84 to 104.45, the strongest since Friday. The context put pressure on the gold price.

On the technical side, The four-hour chart shows that gold prices have slowed since mid-November, with the centre of gravity gradually rising, but the trend is gradually forming a rising wedge that warrants caution, as this is often a signal for a reversal to the downside. RSI sits at 57.47 as of writing. On the four-hour chart, gold price trades above its 50, 100, and 200-day SMA.

US stocks fall to start the final week of 2022 trading. Tesla Inc. shares led to losses as a report of a plan to temporarily halt production at its China factory rekindled fears about demand risks. Besides, Apple Inc. touched the lowest since June 2021 amid a slump in big tech. Moreover, Southwest Airlines Co. led declines in airline stocks after cancelling flights, hobbled by a massive winter storm that battered the US.

The yield on 10-year Treasuries climbed 10 basis points to the highest since mid-November, as China moved to end the quarantine for inbound visitors.

The benchmark, the S&P 500 fell with 0.40% daily losses with trading about 20% below the 30-day average. Six of eleven sectors of the S&P500 stayed in the negative territory, and the Consumer Discretion section got the worst performance among all groups, recording 1.64% losses daily. Apart from this, the tech-heavy Nasdaq underperformed, dropping more than 1%. The Dow Jones Industrial Average surprisingly edged higher by 0.1%, and the MSCI world index moved lower by 0.1% for the day.

Main Pairs Movement

The US Dollar index edged lower on Tuesday, as trading volume is low with investors just coming back from the Christmas holidays. The DXY index hovered in a narrow range from 103.9 to 104.4 during the first trading day of the last week of this year.

The GBPUSD stayed on the defensive since the UK trading session, with China announcing earlier in the day that it will lift quarantine obligations for travellers from January 8 as part of its reopening efforts. The pair dropped around 0.78% in the period of European trading hours. In the meantime, the EURUSD was pricing with wild moves on Tuesday. The pair dropped hugely ahead of the US trading hour but managed to erase most losses and ended with a 0.03% daily gain.

The gold is benefiting from recent positive headlines surrounding Beijing. China’s easing of the Coronavirus-linked activity restrictions joined an upward revision to the 2021 GDP forecast to favour gold bulls amid a sluggish holiday season. The XAUUSD surged and once climbed above the $1830 mark in the early American trading session, then pullback and ended with a 0.86% daily gain on Tuesday.

EURUSD edged higher on the first day of the holiday-shortened trading week. The Euro fared better against the Dollar as market participants continue to sell the Greenback while U.S. interest rate expectations trim lower. Furthermore, the Dallas Fed’s December Texas Manufacturing Outlook Survey indicates a further drawdown of business activity and demand, thus prompting market participants to ditch the U.S. Greenback as markets lower interest rate expectations from the Fed.

The lowered business activity indicator furthers the recession rhetoric as markets brace for pending economic slowdown. On the economic docket, no major data releases are scheduled for the E.U., while the U.S. will release its pending home sales figures during today’s American trading session.

On the technical side, EURUSD continues to trade below our previously estimated resistance level of 1.065, but the pair has witnessed a steady upward momentum over the past four days. A new short-term support level around the 1.0585 price region. RSI for the pair sits at 56.95, as of writing. On the four-hour chart, EURUSD currently trades above its 50, 100, and 200-day SMA.

Resistance: 1.0650, 1.0695

Support: 1.0580, 1.0500, 1.0459, 1.0228

GBPUSD (4-Hour Chart)

GBPUSD edged lower on the first trading day of the week. Cable has been trading extremely range-bound over the past 3 trading sessions as the year ends. The British Pound continues to be plagued by the U.K.’s economic outlook and inflation; however, losses for Cable should be contained as no significant market-moving news is scheduled before 2023. The U.S. Greenback has shown weakness over the holiday weekend as China loosened its Covid restrictions and prompted a gain for the CNY.

The Dollar index lost 0.2% throughout Tuesday’s trading. While the U.S. 10-year treasury yield has resumed above 3.8%, market participants are not piling into U.S. treasury bonds as they expect flows to favour the equity market. On the economic docket, the U.K. has no significant news scheduled for the 28th, while the U.S. will release its pending home sales figures for November during the American trading session.

On the technical side, GBPUSD continues to trade below our previously estimated resistance level of 1.232. A steady downward trend has formed for Cable over the past week. The short-term support level for Cable remains at around the 1.19 and 1.176 price region. RSI for the pair sits at 43.51, as of writing. On the four-hour chart, GBPUSD currently trades below its 50, 100, and 200-day SMA.

Resistance: 1.2320, 1.2600

Support: 1.19, 1.176

XAUUSD (4-Hour Chart)

After dropping toward $1,800 in the early American session on Tuesday, yellow metal prices hiked nearly 1.9% up to a fresh December high of $1,833 during the intraday trading. The markets’ atmosphere started the week in an optimistic mood amid news from China, which is the biggest country producing gold, indicating that the local government will focus on economic growth, further moving away from its zero-covid policy. Meanwhile, the 10-year US Treasury bond yield holds positive territory above 3.8% but does little to nothing to derail the gold price’s rally.

On the technical side, according to the four-hour chart, technical indicators head north almost vertically, although the Momentum stands at neutral levels, while the RSI is near overbought readings. At the same time, XAUUSD has accelerated north after meeting buyers around a flat 20 SMA, currently at $1,805, which remains above the longer ones. RSI sits at 64.28 as of writing. On the four-hour chart, gold price trades above its 50, 100, and 200-day SMA.

US stock ended Friday’s session with gains as investors digested data showing inflation is continuing to ease and the Federal Reserve’s rate hikes are serving their purpose. Data on Friday showed the Fed’s closely watched measure of inflation cooling and consumer spending stagnating. Consumers’ year-ahead inflation expectations also dropped this month to the lowest since June 2021. Both sets of data calmed the market sentiment on Friday. While central bank officials have repeatedly said that they’ll keep raising rates this year, markets have often shrugged off these warnings. However, robust economic data has continued to keep investors on edge.

The benchmarks, the S&P 500 edged higher with a 0.59% daily gain on Friday, and all eleven sectors stayed in the positive territory. Especially for the Energy sector, surging with 3.16% daily for the day, performed the best among all groups. However, the S&P 500 and the tech-heavy Nasdaq 100 still suffered their third week of losses, the longest losing streak since late September, as investors this month grappled with a hawkish Fed and data pointing to a resilient economy that can handle more rate-hike pain.

Main Pairs Movement

The US Dollar index edged lower with 0.11% daily losses, as the US inflation figure declined further than expected. The Personal Consumption Expenditure (PCE) Price Index rose a modest 0.1% in November, missing expectations for a reading of 0.3%. Additional details showed that the Core PCE Price Index (the Fed’s preferred inflation gauge) climbed by 0.2% MoM in November and decelerated to a 4.7% YoY rate from 5.0% previous. The DXY index was wandering in a range from 104.1 to 104.5 level all day, except the moment when the data was released climbing above 104.5 level.

The GBPUSD has little changed on Friday, as trading volume dropped lower ahead of the Christmas holidays. The pair was hovering between the 1.2020 to 1.2090 levels on the last day of the week. In the meantime, the EURUSD mildly moved upward with large volatility, and the pair ended the day with 0.20% daily gains.

The Gold regained upside tractions and rose 0.32% for the day, as US consumer data has shown the inflation is cooling. The XAUUSD witnessed some fresh transactions during the early US trading hours and surged by 0.35% in an hour.

Technical Analysis

EURUSD (4-Hour Chart)

EURUSD traded 0.27% higher throughout Friday’s trading as of writing. It continues to trade in positive territory slightly above $1.0600. The data released by the US for hew home sales (Nov.) increased by 5.8%, core PCE inflation rate declined to 4.7% (Nov.) which all looks a favour in Euro. However, it failed to trigger a reaction. Core PCE’s impact should be straight forward with a weaker-than-forecast print weighing on the US dollar and helping the pair push higher. It probably could be affected by the thinning trading conditions into the Christmas holidays, which failed to gather enough momentum to make a decisive move in either direction.

On the technical side, the pair faces strong support at around the $1.0580 area, where the Fibonacci 23.6% retracement of the latest uptrend and the 100-period SMA on the four charts align. The next estimated level could be seen as $1.0500. RSI for the pair sits at 52.13, as of writing. On the four-hour chart, EURUSD currently trades above its 50 and 100-day SMA but below its 200-day SMA.

Resistance: 1.0650, 1.0695

Support: 1.0580, 1.0500, 1.0459, 1.0228

GBPUSD (4-Hour Chart)

The cable pair raised around 0.28% after two consecutive days of a downtrend, struggling to retain the $1.2000 price level. US PCE inflation eased as anticipated in November and core durable goods orders data is better than expected with 0.2% which is higher than the forecast 0.1%.

The pound edged higher on Friday against the backdrop of a modestly weaker dollar. The UK GDP (annual and quarterly) results released on Thursday were weaker than expected, with the UK economy posting negative growth in the third quarter of 2022 and will add to the focus on the fourth quarter data to be released next year – a technical recession that includes two consecutive quarters of negative growth. In addition, strike action in the U.K., which has reduced household incomes amid rising inflation, puts the Bank of England (BoE) in a difficult position but could end rate hikes sooner than the Federal Reserve, making the outlook for the pound against the dollar unfavourable in 2023.

On the daily chart of GBP/USD, the currency pair is trading near its 200-day SMA after yesterday’s daily close below the psychological barrier of 1.2000 and even a brief break below it. RSI for the pair sits at 53.54, as of writing. On the four-hour chart, GBPUSD currently trades above its 50-day SMA but below its 100 and 200-day SMA.

Resistance: 1.2320, 1.2600

Support: 1.20, 1.19, 1.176

XAUUSD (4-Hour Chart)

Gold price remains mildly bid as bears take a breather after a two-day downtrend. As of writing, the price has back to the $1,800 price level and up to the highest $1,802.75 as of today’s trading. Even so, mixed catalysts challenge the metal buyers in consolidation the biggest daily in over a week.

By the end of 2022, a brief annual review and prospect in 2023 of gold price. Gold prices started in 2022 in an indecisive way after fluctuating around $1,800 in the last quarter of 2021. In late February, gold rose sharply and reached its highest level since August 2020 at $2,070 in early March. However, in the second and third quarters, the gold price fell sharply and fell for seven months in a row, approaching $1,600 in September for the first time since April 2020. In November, gold prices recovered decisively, rising more than 8%, and continued higher in the first few weeks of December, returning to the midpoint of the annual range of around $1,800. Gold prices in 2023 will be driven by two important factors: the Fed’s monetary policy and China’s economic performance.

On the technical side, nothing seems to have changed as gold price still yearns for acceptance above trendline resistance at $1,825. RSI for the precious metal sits at around 55.45, as of writing. On the four-hour chart, XAUUSD currently trades below its 50, 100 day SMA but above the 200-day SMA.