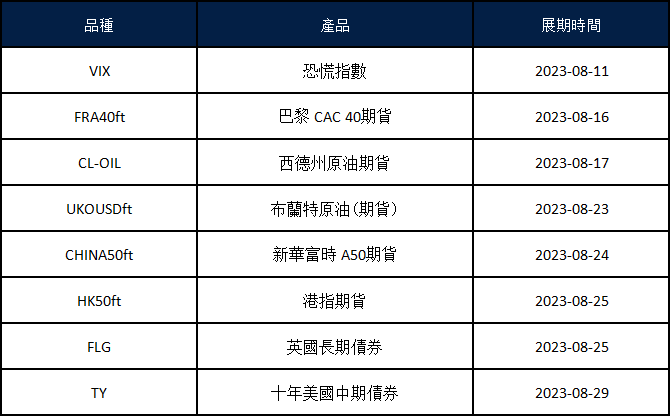

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Stocks experienced a renewed downward trend on Tuesday, triggered by a credit rating downgrade of the banking sector from Moody’s in the midst of an August selloff. The Dow Jones Industrial Average closed with a loss of 158.64 points, or 0.45%, settling at 35,314.49, while the S&P 500 ended down 0.42% at 4,499.38, reflecting a month-to-date decline of nearly 2%. The Nasdaq Composite also retreated by 0.79% to 13,884.32, deepening its August loss to 3.2%. This marked the fifth negative day in six sessions for both the S&P 500 and the Nasdaq, with neither index breaking into positive territory despite recovering from session lows.

Moody’s credit rating downgrade had a pronounced impact on the banking sector, causing a broad decline. Regional banks like M&T Bank and Pinnacle Financial faced credit rating reductions due to concerns about deposit risk, potential recession, and challenges in commercial real estate portfolios. Bank of N.Y. Mellon and State Street were placed under review for potential downgrades as well. Consequently, banking giants Goldman Sachs and JPMorgan Chase saw declines of around 2.1% and 0.6%, respectively, while the SPDR S&P Bank ETF (KBE) dropped by 1.3%. The SPDR S&P Regional Banking ETF (KRE) also lost 1.3%, with a notable history of decline due to previous events such as the failure of Silicon Valley Bank. The downgrade emphasized the crucial importance of strong credit ratings for regional banks, as any loss of faith in the sector negatively impacts market sentiment. Amid these developments, UPS reported weaker-than-expected revenue for Q2, leading to a 0.9% drop in its shares. Despite the generally positive corporate earnings season, where a majority of S&P 500 companies exceeded expectations, the market appeared to have already priced in these results, contributing to the ongoing pullback.

On Tuesday, most sectors experienced a decline, with the overall market decreasing by 0.42%. Health Care and Utilities, however, showed gains, rising by 0.78% and 0.49% respectively. Energy also saw a similar increase of 0.49%. Communication Services and Real Estate sectors faced slight decreases of 0.23% and 0.45% respectively. Industrials, Consumer Staples, Information Technology, and Consumer Discretionary sectors all declined, ranging from -0.46% to -0.87%. Financials and Materials were the hardest hit, both decreasing by 0.87% and 1.05% respectively.

Major Pair Movement

The dollar index exhibited a 0.54% increase on Tuesday, primarily driven by safe-haven demand, which overshadowed even larger gains against currencies sensitive to risk due to recent events. The euro faced additional downward pressure due to its significant reliance on Chinese demand, worsened by recent data. The European Central Bank’s (ECB) struggle to fully address inflation, with both overall and core euro zone inflation remaining above 5%, has led to market uncertainty regarding another ECB interest rate hike to reach 4%. Meanwhile, the U.S. Federal Reserve’s (Fed) July rate hike to 5.5% is perceived as its final move before future rate cuts.

In the U.S., both overall and core Consumer Price Index (CPI) stood at 3% and 4.8% in June, with forecasts projecting an increase to 3.3% and 4.8% for July. Despite the upcoming shift in the base effect, which will transition from depressing year-over-year comparisons to elevating them, the monthly increase for July is expected to remain steady at a modest 0.2%. In comparison, the Fed appears to be more advanced in its efforts to combat inflation, while the U.S. economy is displaying greater resilience compared to the euro zone. While the possibility of a soft landing for the U.S. economy is still uncertain, the likelihood of a harder landing for the euro zone seems more plausible.

The EUR/USD currency pair experienced a 0.43% decline, yet found support at 1.0930 lows, coinciding with the 55-day moving average and mirroring last week’s lows. Despite an approximately 8 basis points decline in the two-year bund-Treasury yield spreads, they did not reach their previous lows from August. The adjustment in Treasury yields, in part driven by preparation for a three-day Treasury refunding and influenced by recent auction outcomes, was followed by a subsequent decrease in yields after a strong 3-year auction. The USD/JPY pair saw a 0.57% increase, as the demand for the higher-yielding dollar overpowered the safe-haven appeal of the yen, particularly following certain developments. Furthermore, both the Australian dollar (AUD) and the Chinese yuan (CNH) experienced declines of 0.59% and 0.45% respectively, with USD/CNH surpassing a crucial downtrend line, while concerns about China and global economic growth led to significant losses in industrial metals. The focus is now shifting towards upcoming U.S. Consumer Price Index (CPI) and Producer Price Index (PPI) reports scheduled for Thursday and Friday.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Resilient Amid Strong Dollar and Economic Factors

The EUR/USD pair faced losses on Tuesday due to a robust US Dollar and rising risk aversion, yet managed to remain above a vital support level. Italy’s surprise announcement of a bank profits windfall tax caused the Italian stock index to plummet over 2%, while Wall Street indices also dipped following Moody’s downgrade of US banks. The European Central Bank’s June survey indicated decreased inflation expectations, affecting market views on rate hikes. Meanwhile, the US Dollar gained strength amidst risk aversion and mixed messages from Federal Reserve officials. The focus now shifts to Thursday’s influential US Consumer Price Index (CPI) report.

Based on technical analysis, the EUR/USD remained steady on Tuesday as the market awaited upcoming US inflation data for the week, specifically CPI and PPI, while also attempting to move toward the middle band of the Bollinger Bands. Right now, the price is slightly below the middle band, creating a small gap between the upper and lower bands of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 46, showing that the EUR/USD is in a phase of consolidation.

Resistance: 1.1038, 1.1121

Support: 1.0915, 1.0839

XAU/USD (4 Hours)

XAU/USD Hits Four-Week Low as US Dollar Strengthens Amid Fed Remarks and Economic Uncertainty

During the early American trading session, XAU/USD plummeted to a new four-week low at $1,922.74 per troy ounce. This drop was fueled by a surge in demand for the US Dollar following comments from Federal Reserve officials and in anticipation of the upcoming release of the US July Consumer Price Index.

Philadelphia Federal Reserve Bank President Patrick Harker’s statements highlighted a move toward normalcy in economic conditions. Despite optimism for a smooth economic transition, concerns persisted over supply chain issues. Harker also suggested the possibility of the Fed exercising patience with interest rates, depending on future data, including the pivotal decision in September. Despite global stock declines and worries about economic uncertainty, gold’s price decline persisted. However, a slight pullback in Treasury yields prevented a more significant appreciation of the US Dollar.

Based to technical analysis, the XAU/USD experienced a minor decrease on Tuesday, managing to touch the lower band of the Bollinger Bands. Currently, the price is slightly below the middle band within the Bollinger Bands. The Relative Strength Index (RSI) stands at 40, suggesting that the XAU/USD pair is somewhat in a bearish mode.

In ancient Japan, there was a brilliant rice trader named Munehisa Homma. He had a unique talent for predicting future price movements in the rice markets. How did he do it? Well, he closely observed market prices and studied the emotions of fear and greed among traders. This keen observation led him to create something groundbreaking – the candlestick chart.

Homma’s candlestick chart displayed the open, high, low, and close prices over specific time periods, giving traders a visual representation of price movements. This innovation caught on quickly and spread throughout Japan, revolutionising trading.

Fast forward to the late 19th century when Charles Dow, a co-founder of Dow Jones & Company and the Wall Street Journal, encountered Japanese candlestick charting. Impressed by its potential, he brought it to the Western world, where it further evolved.

Over time, Technical Analysis, as it came to be known, saw the addition of the Elliott Wave Theory and benefited greatly from advancements in technology. Traders gained access to sophisticated charting software and a wide range of technical indicators.

Today, Technical Analysis remains a favoured approach in Forex trading. It allows traders to make informed decisions based on data-driven insights, empowering them to navigate the dynamic and ever-changing markets with confidence.

Understanding Technical Analysis

Imagine being a detective, deciphering hidden clues in the financial market to predict its next move. That’s precisely what Technical Analysis does for traders! It’s a fascinating discipline that involves diving into historical market data, with a keen focus on price charts and trading volumes. But wait, there’s more!

While Fundamental Analysis looks at economic indicators and financial reports, Technical Analysis takes a different route. It operates on the belief that everything you need to know about an asset is already encoded in its price. It’s like the market’s secret language waiting to be decoded.

Traders who wield Technical Analysis skills study the past price patterns, seeking clues and hints about the future. They are the Sherlock Holmes of the trading world, spotting trends and potential trade opportunities with precision.

Through this powerful analytical approach, traders get a glimpse into the market’s underlying sentiment. They understand when it’s giddy with optimism, paralysed by fear, or in the grip of uncertainty. Armed with these insights, they make informed decisions about the perfect moment to enter or exit trades.

So, why does this matter so much? In the fast-paced world of Forex trading, timing is everything. Technical Analysis gives traders the edge they need to navigate through the turbulence of the market, making well-timed moves and staying ahead of the game. It’s no wonder Technical Analysis is a favourite among traders who love the thrill of decoding the market’s mysteries and reaping rewards from their astute predictions.

Basic Concepts of Technical Analysis

To navigate the dynamic world of financial markets effectively, traders must grasp the foundational concepts of Technical Analysis. These core principles provide a deeper understanding of market dynamics and empower traders to make well-informed decisions.

Price Charts

Price charts serve as the bedrock of Technical Analysis, offering a visual representation of historical price movements of currency pairs over specific timeframes. Among the commonly used charts are candlestick and line charts.

Candlestick charts present a wealth of information, revealing open, high, low, and close prices within a designated timeframe. On the other hand, line charts provide a simplified view, showcasing only the closing prices. Understanding these charts enables traders to spot patterns, trends, and potential turning points in the market.

source: Britannica Money

Timeframes

Mastering different timeframes is essential for traders to adapt their strategies to various market conditions.

Timeframes vary from ultra-short periods, such as seconds or minutes, favoured by intraday traders seeking rapid profit opportunities, to longer-term perspectives like daily or weekly, preferred by investors aiming to capture substantial trends.

Analysing price action across multiple timeframes offers a comprehensive view of market behaviour, facilitating well-timed entries and exits.

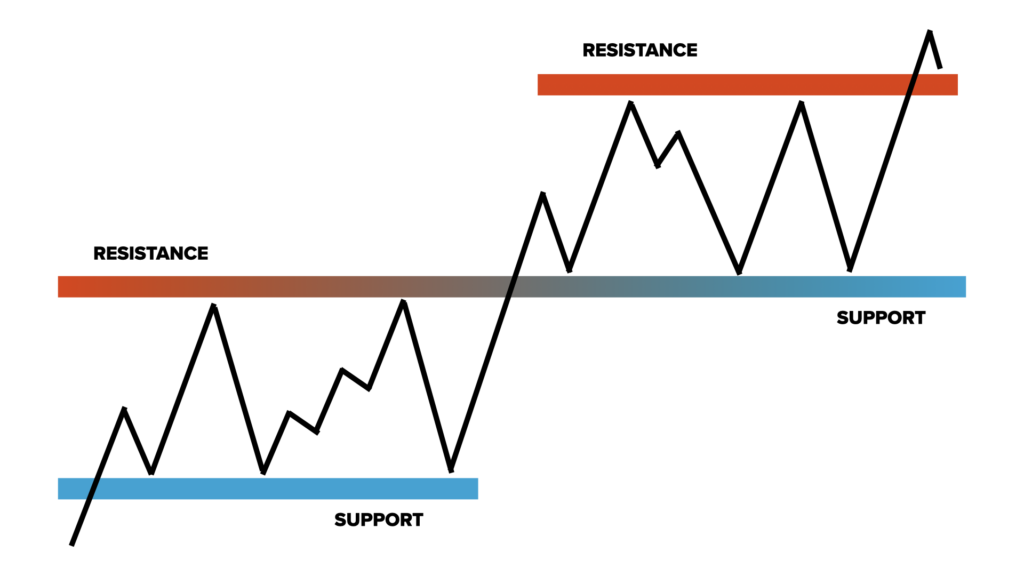

Support and Resistance

The concepts of support and resistance levels are invaluable tools for traders seeking to identify crucial price levels in the market.

Support refers to price zones where demand is strong enough to halt a downtrend, acting as a price floor. Conversely, resistance denotes areas where supply is abundant enough to prevent an uptrend from continuing, creating a price ceiling.

Recognising these levels empowers traders to make strategic decisions, such as placing stop-loss and take-profit orders and enables them to anticipate potential trend reversals.

Trend Lines

Trend lines are powerful aids in understanding market direction and momentum. By drawing straight lines connecting consecutive peaks or troughs on a price chart, traders gain insights into the prevailing trend – whether it is upward, downward, or sideways.

Trend lines help traders identify key support and resistance levels, confirm trend strength, and anticipate potential breakout or reversal points. Understanding trend lines enhances traders’ ability to ride trends and capitalise on market opportunities.

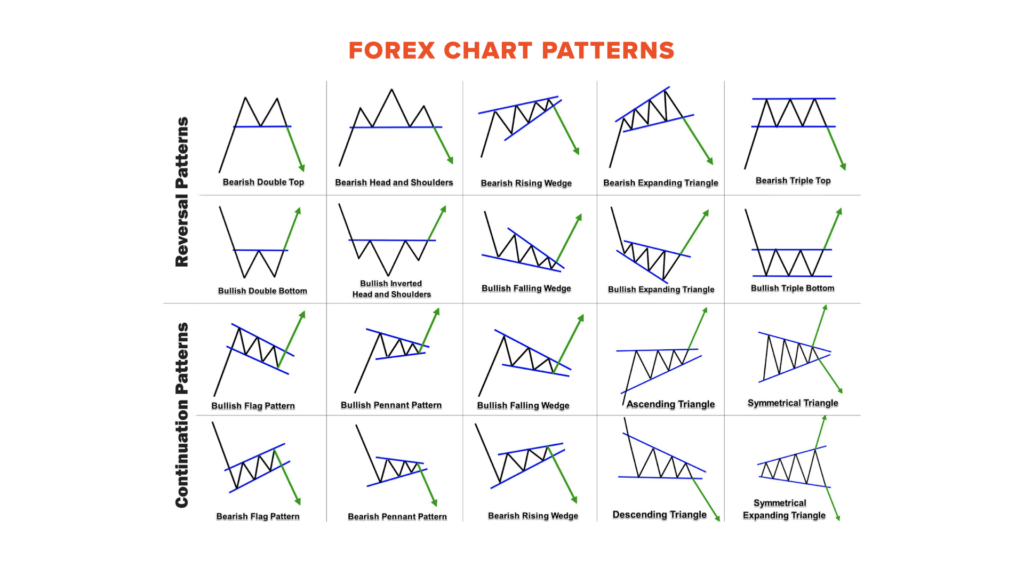

Basic Chart Patterns

In Technical Analysis, chart patterns play a significant role in providing insights into potential market reversals or continuations. These patterns are recognised for their ability to signal shifts in market sentiment. Let’s explore some common chart patterns that traders frequently encounter:

Technical Analysis encompasses a variety of chart patterns, each carrying its own unique implications. Some well-known patterns include the Head and Shoulders, Double Tops, Double Bottoms, and Triangles. Understanding these patterns can help traders anticipate potential changes in market direction and identify trading opportunities.

The key to effective trading lies in accurately identifying chart patterns. Each pattern provides important information about the balance between buyers and sellers. By mastering pattern recognition, traders can gain insights into potential price targets and develop informed trading strategies.

Moreover, chart patterns are often accompanied by volume trends, which can serve as additional confirmation of their validity. Volume, reflecting the number of shares or contracts traded in a given period, can complement pattern analysis and help assess the strength of signals. Integrating both chart patterns and volume analysis empowers traders to make well-considered decisions when executing trades.

Technical Indicators

Technical indicators are mathematical calculations derived from price, volume, or open interest data. Their primary purpose is to aid traders in confirming trends, measuring momentum, and identifying potential buy or sell signals.

source: Britannica Money

There is an array of technical indicators available to traders, each serving a unique purpose. Moving Averages help smooth out price data and indicate trend direction. The Relative Strength Index (RSI) measures overbought or oversold conditions, while the Moving Average Convergence Divergence (MACD) highlights changes in a trend’s strength and direction.

Interpreting indicators involves analysing their values in conjunction with price patterns and other relevant market factors. Divergence between an indicator and price movement can also provide valuable insights into potential shifts in market sentiment.

Pros & Cons of Technical Analysis

Mastering the art of trading involves understanding the strengths and limitations of various analytical approaches. Technical Analysis, a popular method used by traders worldwide, offers its fair share of advantages and drawbacks.

Pros:

Accessibility: Technical Analysis is renowned for its accessibility, catering to traders of all experience levels. With a wealth of educational resources available, beginners can quickly grasp its concepts and apply them to their trading endeavours.

Visual Representation: Price charts and technical indicators act as valuable visual aids, providing traders with an intuitive representation of market trends and patterns. The visual nature of Technical Analysis simplifies data interpretation and supports informed decision-making.

Wide Range of Indicators: The diverse selection of technical indicators empowers traders to customise their analyses to adapt to various market conditions and trading styles. This flexibility allows for a more personalised and adaptable approach to trading.

Cons:

Subjectivity: Technical Analysis entails interpreting patterns and indicators, making it susceptible to subjectivity. Different traders may draw varying conclusions from the same data, leading to a degree of interpretation variance.

Historical Based: Technical Analysis primarily relies on historical price data, which may not fully account for unforeseen events or sudden shifts in market sentiment. As a result, abrupt market changes can challenge the accuracy of technical predictions.

Limited Scope: Relying solely on Technical Analysis might overlook crucial fundamental factors that significantly influence currency movements. Neglecting these fundamental aspects can lead to incomplete market analyses and trading decisions.

Tips for Using Technical Analysis in Forex Trading

To leverage Technical Analysis in the Forex market effectively, follow these key tips:

Master the Basics: Understand key concepts like price charts, trend lines, and support/resistance levels.

Combine Indicators: Use a mix of indicators and chart patterns for stronger analysis.

Choose Timeframes Wisely: Select the right timeframe that suits your trading style.

Be Patient and Disciplined: Avoid impulsive decisions and wait for clear signals.

Implement Risk Management: Set stop-loss and take-profit orders to protect your capital.

Stay Informed: Keep an eye on market news and events that may impact your analysis.

Backtest Strategies: Test your strategies on historical data before live trading.

Avoid Overtrading: Stick to your trading plan and avoid excessive trades.

Maintain a Trading Journal: Record your trades and learn from your experiences.

Keep Learning: Stay updated with new developments in Technical Analysis and Forex trading.

In conclusion, Technical Analysis is an invaluable tool in the world of Forex trading, empowering traders with insights into market trends and potential trading opportunities. By mastering basic concepts, recognising chart patterns, and effectively using technical indicators, traders can make more informed decisions. However, it is crucial to combine Technical Analysis with other analytical methods and apply sound risk management practices to navigate the complexities of Forex trading successfully.

Summary:

Technical Analysis decodes the market’s language using historical data and price charts.

Core concepts include price charts, timeframes, support/resistance, trend lines, and chart patterns.

Technical indicators confirm trends and identify buy/sell signals.

Technical Analysis offers pros such as accessibility, visual representation, and a wide range of indicators, but it has cons like subjectivity, reliance on historical data, and limited scope.

Combining Technical Analysis with other methods and risk management enhances trading success.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

The Dow Jones Industrial Average commenced the week with a robust surge of 1.16%, gaining 407.51 points to conclude at 35,473.13, marking its most substantial upswing since June 15. Buoyed by a nearly 4% rally from Amgen, the blue-chip index received a notable boost. In tandem, the S&P 500 climbed by 0.9% to settle at 4,518.44, while the Nasdaq Composite posted a more modest 0.61% increase, curtailed by a near 1% dip in Tesla shares following the departure of CFO Zach Kirkhorn. Both the Nasdaq and S&P 500 managed to break their four-day losing streaks.

Berkshire Hathaway exhibited a remarkable ascent of over 3%, reflecting investor contentment with the company’s financial results and robust cash reserves. Notably, shares of both A and B share classes reached unprecedented levels. Elanco, a player in the animal healthcare sector, surged by 4% after surpassing Wall Street expectations, whereas Tyson Foods faltered by 3.8% on the back of a less-than-anticipated report. In another significant development, Sovos Brands, recognized for Rao’s, witnessed a remarkable surge of more than 25% after Campbell Soup’s announcement of its acquisition of the pasta sauce manufacturer. While Campbell Soup’s shares slipped by approximately 1.8%, they settled at their lowest price in over a year. Following a challenging week on Wall Street, marked by a 2.9% slide in the Nasdaq Composite and a 2.3% dip in the S&P 500, the market rebounded with renewed vigor.

This resurgence was attributed to a stronger-than-expected corporate earnings season, with around 80% of S&P 500 companies surpassing Wall Street forecasts. According to Chris Zaccarelli, Chief Investment Officer of the Independent Advisor Alliance, the market has regained a “risk-on mode” due to the favorable earnings trend. Looking ahead, investors are poised to focus on the impending release of consumer and producer price index data for July, as these indicators hold crucial implications for inflation trends and economic well-being.

On Monday, across all sectors, the market showed a notable uptick of 0.90%. Particularly strong gains were observed in the Communication Services sector, which surged by 1.88%, followed closely by Financials with a rise of 1.36%, and Industrials, which advanced by 1.26%. Real Estate also exhibited a solid increase of 1.21%, while the Health Care sector saw a rise of 1.18%. Noteworthy gains were recorded in the Consumer Discretionary sector, which climbed by 1.10%, and the Consumer Staples sector, which experienced a respectable growth of 0.85%. Materials exhibited a modest uptrend of 0.70%. However, the Information Technology sector displayed a more subdued increase of 0.27%, and the Energy sector had a marginal rise of 0.15%. In contrast, the Utilities sector showed a slight decline of -0.02% during the same trading period.

Major Pair Movement

The dollar index initially rebounded on Monday from the previous slide triggered by Friday’s jobs report, yet it remained relatively unchanged as shorter-term Treasury yields decreased. The upcoming U.S. inflation report on Thursday could potentially affirm the belief that the Federal Reserve’s tightening cycle has concluded, increasing the likelihood of rate cuts in 2024. The recent jobs report offered conflicting signals regarding the labor market’s condition and the necessity for further Fed tightening, contributing to market uncertainty. While the labor market is gradually loosening, the exact timing of a significant shift and subsequent Fed rate cuts remains uncertain, especially considering the economy’s resilience despite substantial rate hikes by the Fed.

Market confusion persists over the necessity of tight policy, irrespective of the labor market’s status, particularly if inflation continues its trajectory towards the Fed’s target. Monday saw contrasting policy outlooks from Fed officials Bowman and Williams, hinting at a potential pause by the Fed until clearer indications emerge for a more or less restrictive approach. The impending Consumer Price Index (CPI) release on Thursday could play a pivotal role in resolving this policy divergence. In the currency markets, EUR/USD dipped slightly by 0.05%, unable to surpass Friday’s initial post-payrolls highs. The European Central Bank’s assessment of peaking underlying inflation and concerns over economic growth, amplified by Chinese economic uncertainties, could impact the probability of another ECB rate hike. USD/JPY, on the other hand, rose by 0.5% as buyers entered the market above 141.50 following post-payrolls lows. Despite the Bank of Japan’s hopeful stance on rising wages, low Japanese Government Bond yields continue to contrast with higher U.S. Treasury yields. Sterling managed to gain 0.3% after a hesitant start, supported by a rise in 2-year gilts-Treasury yields spreads and the maintenance of essential support levels following the Bank of England’s recent rate hike.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rises Amid Weaker Dollar and Market Focus on US Inflation Data

The EUR/USD pair rebounded to 1.1000 during the American session, propelled by a weakened US dollar and improved risk appetite. While Monday brought relative calm to financial markets, attention remains fixed on the upcoming US inflation figures later in the week. Germany’s Industrial Production data for June displayed a larger-than-expected contraction of 1.5%, diverging from the projected -0.4% decline. Meanwhile, Eurozone Sentix Investor Confidence showed recovery, reaching -18.9 from -22.5. In the coming days, the spotlight shifts to Germany’s final Consumer Price Index (CPI) report for July, anticipated to reflect an unchanged annual rate of 6.2%.

Market sentiment revolves around the possibility of an impending rate hike by the European Central Bank (ECB), though the September meeting might not be the venue for such action. While the likelihood of a rate hike remains below 50% for September, odds increase to 60% for October, as indicated by the interest rate market. The EUR/USD’s trajectory continues to hinge on the performance of the US Dollar, which posted mixed results on Monday following the Non-Farm Payrolls (NFP) report-induced decline on Friday. The upcoming US inflation data release on Thursday and Friday takes center stage, with the US Dollar Index exhibiting a bearish bias in the short term, tempered by the underlying strength of the US economy.

Based on technical analysis, the EUR/USD remained steady on Monday as the market awaited upcoming US inflation data for the week, specifically CPI and PPI, while also attempting to move toward the middle band of the Bollinger Bands. Right now, the price is slightly above the middle band, creating a small gap between the upper and lower bands of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 50, showing that the EUR/USD is in a phase of consolidation.

Resistance: 1.1038, 1.1121

Support: 1.0915, 1.0839

XAU/USD (4 Hours)

XAU/USD Retreats as USD Gains Momentum Amid Fed Tightening Concerns

The XAU/USD pair experienced a reversal in its recent gains as the US Dollar gained strength, trading at around $1,933 per troy ounce after the close of London’s session. Concerns over the Federal Reserve’s ongoing tightening measures in the new week led to a risk-averse shift in financial markets. While the USD’s rally paused prior to Wall Street’s opening, comments from Fed’s New York President John C. Williams provided some reassurance, emphasizing data-dependency for any future rate adjustments. As Wall Street saw upward momentum, particularly reflected in the Dow Jones Industrial Average’s rise by approximately 350 points, the precious metal faced downward pressure. In the week ahead, market attention will be focused on the US Consumer Price Index (CPI) data for July, with potential implications for USD sentiment depending on the outcome relative to expectations.

Based on technical analysis, the XAU/USD faced a small decrease on Monday, aiming to get closer to the lower band of the Bollinger Bands. Right now, the price is a bit above the lower band in the Bollinger Bands setup. The Relative Strength Index (RSI) is at 40, indicating that the XAU/USD pair has a somewhat negative outlook.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Several key market events are expected to influence the financial markets this week. Specifically, the highly awaited US Consumer Price Index and Producer Price Index will be released. In light of these crucial announcements, we advise traders to approach their trading preparations with caution, considering the potential for heightened market volatility.

Here are some key economic highlights to keep an eye on during the week:

New Zealand Inflation Expectations (9 August 2023)

Inflation expectations in New Zealand declined to 2.79% in Q2 2023 from 3.3% in Q1 2023.

The figures for Q3 2023 will be released on 9 August, with analysts expecting another decrease to 2.5%.

US Consumer Price Index (10 August 2023)

Consumer prices in the US rose 0.2% month-over-month in June 2023 after a 0.1% increase in the previous month.

Analysts anticipate a 0.2% rise in the figures for July, scheduled for release on 10 August.

UK Gross Domestic Product (11 August 2023)

The British economy shrank by 0.1% month-over-month in May 2023, following a 0.2% growth rate in April.

The figures for June are set to be released on 11 August, with analysts expecting the country’s GDP to grow by 0.1%.

US Producer Price Index (11 August 2023)

Producer prices for final demand in the US edged up 0.1% month-over-month in June 2023, following a 0.4% fall seen in May.

The data for July 2023 will be released on 11 August, with analysts expecting a 0.2% increase.

University of Michigan Consumer Sentiment Index (11 August 2023)

The University of Michigan consumer sentiment for the US was revised lower to 71.6 in July 2023 from a preliminary reading of 72.6. It was the highest reading since October 2021 due to the continued slowdown in inflation along with the stabilisation of labour markets.

Analysts expect a reading of 70.9 in the upcoming set of data, due for release on 11 August.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The S&P 500 continued its decline for a third day in a row, grappling with the impact of rising bond yields and mixed corporate earnings results. The index fell 0.25%, closing at 4,501.89, while the Dow Jones Industrial Average also lost 0.19%. The Nasdaq Composite inched down by 0.1% at the end of the trading day. The surge in the benchmark 10-year Treasury yield, reaching around 4.18% – its highest since November 2022, added pressure to the real estate sector and resulted in a spike in the Cboe Volatility index. Utilities were also impacted, losing 2.3%.

Some experts on Wall Street highlighted that the market had been overdue for a pause or minor correction, following months of bullish performance. The recent trend of eroding momentum raised concerns, although the longer-term outlook remained positive. The week’s busy earnings reports included chipmaker Qualcomm, which saw an 8.2% drop after disappointing results, and PayPal, which shed 12.3% despite posting in-line results. Meanwhile, Expedia experienced a significant plunge of 16.4% as its gross bookings fell short of expectations.

The market’s focus shifted to tech giants Apple and Amazon, set to release their earnings reports after trading hours. So far, approximately 79% of S&P 500 companies have issued quarterly reports, with around 82% surpassing expectations, but overall earnings are expected to be about 5% lower than the previous year. In the midst of these developments, the Bank of England raised interest rates by 25 basis points to tackle inflation. Additionally, Wall Street kept a close eye on economic data, including weekly jobless claims and second-quarter productivity figures, which showed slight improvements.

On Thursday, the overall market declined by 0.25%. The energy sector showed a notable gain of 0.95%, while consumer discretionary and financial sectors also saw modest increases of 0.34% and 0.07%, respectively. On the other hand, the real estate and utilities sectors experienced significant losses of 1.35% and 2.29%, respectively. Additionally, the information technology sector declined by 0.32%, health care by 0.50%, and industrials and materials both dropped by 0.61% and 0.60%, respectively. Communication services and consumer staples also faced minor declines of 0.17% each.

Major Pair Movement

The dollar index experienced a 0.11% decline, led by a 0.48% loss in USD/JPY, as mixed U.S. data weighed on market sentiment ahead of Friday’s employment report. The dollar’s recent recovery was interrupted due to rising Treasury yields compared to bunds, JGBs, and gilts, though it had already recovered most of its late June to July slide. The markets eagerly awaited Friday’s jobs report to gauge its potential impact on monetary policy.

During Thursday’s trading, long dollar positions were squared off, partly driven by signs that the recent surge in longer-term Treasury yields might have reached a near-term peak. EUR/USD rebounded slightly, while USD/CNH and USD/JPY experienced losses, contributing to profit-taking on long dollar positions. The sharp fall in the yen was influenced by the Bank of Japan’s decision to double the hard cap on 10-year JGB yields, raising concerns over potential Japanese selling of Treasury holdings. Sterling remained flat after the Bank of England’s 25bp rate hike, which fell short of expectations for a 50bp hike. Additionally, Brent and WTI crude oil prices rose following Saudi Arabia’s decision to extend production cuts, impacting USD/NOK and AUD/USD.

EUR/USD Stays Steady Ahead of US Employment Data Despite Limited Market Impact

The EUR/USD remained flat during a quiet session, trading around 1.0940, as investors awaited crucial US employment data. On the economic front, Germany reported lower-than-expected June exports and imports, while Eurostat revealed a decline in the Producer Price Index (PPI) for the Euro area. The Bank of England’s rate hike initially boosted EUR/GBP, but gains were later reversed. In the US, data on initial Jobless Claims and Unit Labor Costs were released, with focus shifting to the upcoming Nonfarm Payrolls report, expected to show an increase of 200,000 jobs.

According to technical analysis, the EUR/USD remained flat on Thursday as the market awaited today’s US Non-farm data, reaching the middle band of the Bollinger Bands. Currently, the price is moving at the middle band, creating a narrow gap between the upper and lower bands of the Bollinger Bands. The Relative Strength Index (RSI) currently stands at 44, suggesting that the EUR/USD is back in consolidation mode. Please be aware that we expect high volatility in the EUR/USD today as the US Non-Farm data will be released.

Resistance: 1.1038, 1.1121

Support: 1.0915, 1.0839

XAU/USD (4 Hours)

XAU/USD Consolidates Losses as US Dollar Strength Persists Amid Labor Market Concerns

On Thursday, XAU/USD traded in the $1,930 price zone, consolidating losses after hitting its lowest point in almost a month at $1,929.48 per troy ounce. The decline was attributed to the continued strength of the US Dollar, which benefited from a somber market sentiment, leading to increased government bond yields and impacting equities. Market players are worried that the tight US labor market will prompt the Federal Reserve to maintain its tightening path for a longer duration than expected. Despite signaling at least one more rate hike, uncertainty prevails as tepid economic indicators suggest a possible pause. The July Nonfarm Payrolls Report (NFP) is eagerly awaited to gain more clarity on the employment situation in the US.

According to technical analysis, on Thursday, the XAU/USD remained flat, with the upper and lower bands of the Bollinger Bands moving closer together. Currently, the price is slightly below the middle band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 39, indicating that the XAU/USD pair is still slightly bearish.