Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In the fast-paced world of trading, staying vigilant and well-informed is paramount for success. The upcoming week is filled with crucial economic events that traders should closely monitor to navigate the markets effectively. From employment figures in the UK to price trends in Canada and inflation rates worldwide, each data point narrates a compelling story. The canvas of our economic puzzle extends to include US retail sales and Australian employment statistics, offering valuable insights that guide our understanding of the global financial terrain.

UK Claimant Count Change (16 January 2024)

Keep an eye on the UK Claimant Count Change, set to be released on January 16, 2024. After witnessing an increase from 8,900 to 16,000 in November, expectations are that the figure will rise further to 18,100 in the upcoming release.

Canada Monthly Consumer Price Index (16 January 2024)

An additional event in January 16, Canada unveils its Monthly Consumer Price Index (CPI). In November 2023, consumer prices in Canada defied expectations by rising 0.1%, contrary to the anticipated 0.1% decline. However, the December 2023 data, expected to be released on January 16, 2024, forecasts a 0.3% decline in the monthly Consumer Price Index.

UK Annual Consumer Price Index (17 January 2024)

On January 17, 2024, the focus turns to the UK Annual Consumer Price Index. After a slowdown to 3.9% in November 2023 from 4.6% in October, analysts anticipate a further decrease to 3.8% in the December 2023 data.

US Retail Sales (17 January 2024)

Discover the trajectory of US retail sales on January 17. Following an unexpected 0.3% increase in November 2023, the upcoming release is projected to show a further uptick, with an expected growth of 0.4% in December 2023.

Australia Employment Change (18 January 2024)

Turn your attention to Australia on January 18, as the Employment Change data unfolds. After a notable increase of 61,500 in November 2023, the forecast for December 2023 suggests a more modest rise, with expectations set at 18,000.

UK Retail Sales (19 January 2024)

As we approach January 19, anticipation builds for the release of UK Retail Sales data. Despite a robust 1.3% month-over-month growth in November 2023, December 2023 is expected to show a contraction of 0.5%.

US Prelim University of Michigan Consumer Sentiment (19 January 2024)

Closing out the week, all eyes will be on the US preliminary consumer sentiment from the University of Michigan for January 19. Projections indicate a slight dip to 69.6 from the previous month’s 69.7 in December 2023, offering insights into the mood of the American consumer.

The US Dollar gains strength in response to higher-than-expected US inflation data and a decrease in unemployment claims.

Despite inflation exceeding the target and a robust labor market, the Federal Reserve may hesitate to cut interest rates prematurely.

The technical analysis in this article focuses on EUR/USD and GBP/USD, examining critical price levels post the US CPI report.

The DXY index, measuring the US Dollar, rises by 0.3% following the release of the December inflation survey and weekly jobless claims data.

Headline CPI surprises on the upside, registering 3.4% year-on-year, surpassing the expected 3.2%, while the core gauge comes in at 3.9%.

Jobless benefits applications hit a three-month low, indicating a resilient labor market and ongoing hiring despite the late business cycle stage.

With consumer prices above the 2.0% target and a strong labor market, the Fed is unlikely to make significant interest rate cuts, contrary to market expectations.

Monitoring Fedspeak in the upcoming days and weeks will provide insights into the monetary policy outlook, with a potential shift towards a more hawkish stance favoring yields and the US Dollar.

Banks stocks, coming off their strongest quarter since 2021, are poised for a significant earnings event where top executives will provide insights into the US economy.

JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc., and Wells Fargo & Co. are set to kick off the earnings reporting cycle after US bank stocks gained 23% in the last quarter, outperforming the broader market.

Bank shares faced pressure in 2023 but surged in late October amid confidence that the Federal Reserve would conclude its rate-hike campaign without causing a recession.

The focus now shifts to the timing of policy easing, with investors closely examining its implications for various aspects of the banking business, including loan portfolios and deposit rates.

Analyst Richard Ramsden from Goldman Sachs Group Inc. notes that while banks are not as cheap as before, their valuations are not perceived as stretched.

Positive outcomes regarding net interest income, loan growth, capital markets, and deposit pricing are expected to contribute to greater earnings and potential outperformance by some banks.

The KBW Bank Index fell about 1% on Thursday, underperforming the broader market.

Morgan Stanley and Goldman Sachs’ earnings on Tuesday will be closely watched, along with PNC Financial Services Group’s results, which will serve as a bellwether for regional lenders.

Big banks are anticipated to report subdued fourth-quarter results due to higher funding costs, with net interest income expected to decline, and elevated expenses and weak trading revenue likely weighing on earnings.

Companies are also expected to disclose payments to the Federal Deposit Insurance Corp. related to regional bank failures from the previous year.

The rally in bank shares last quarter was driven by optimism about reduced recession risks and expectations of Fed rate cuts in 2024, alleviating concerns about net interest margins.

Despite positive momentum, caution is advised, with concerns about the inflation rate remaining above the Fed’s target and potential wild swings in sentiment.

Hedge funds have been selling the financial sector in the past four weeks, but financial companies are the only sector where the majority of analyst earnings revisions were upward over the past month.

DWS Group’s David Bianco maintains an overweight position on big banks, including JPMorgan, Bank of America, Citigroup, and Wells Fargo, citing their robust profitability and stable credit.

In a market shaped by unexpected inflation rates and resilient labor trends, join VT Markets to expertly navigate the shifting currents of the forex and stock markets.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Thursday, major stock indices experienced a subdued performance with the Nasdaq Composite settling at 14,970.19, the Dow Jones Industrial Average gaining 0.04%, and the S&P 500 dipping 0.07%. The release of December’s consumer price index (CPI) report, revealing a 0.3% increase in consumer prices, impacted market sentiment, influencing expectations for future interest rate cuts. Investors also remained cautious about the Federal Reserve’s rate cut timeline and upcoming fourth-quarter earnings reports. Meanwhile, the cryptocurrency market saw positive momentum, marked by the rise of bitcoin exchange-traded funds (ETFs) following recent SEC-approved rule changes. The currency market experienced volatility driven by higher-than-expected US inflation figures, with the USD Index surging initially but later losing momentum. The Euro, Pound, Yen, Aussie, and Canadian Dollar showed varied responses to the economic landscape, reflecting the uncertainties surrounding inflation dynamics and corporate earnings.

Stock Market Updates

Stocks experienced a relatively flat performance on Thursday, as reflected in the closing numbers of major indices. The Nasdaq Composite settled at 14,970.19, while the Dow Jones Industrial Average gained a modest 0.04%, closing at 37,711.02. The S&P 500 saw a slight dip of 0.07%, ending the session at 4,780.24, briefly surpassing its record closing high earlier in the day. The market was influenced by the release of December’s consumer price index (CPI) report, which showed a slightly higher-than-expected increase of 0.3% in consumer prices, pushing the annual rate to 3.4%. The data hinted at persistent but easing inflation pressures, impacting expectations for future interest rate cuts. Yields on the 10-year note initially rose in response to the CPI data, reaching a high of 4.068% before settling around 3.98%.

The market’s movements on Thursday were also shaped by cautious sentiments surrounding the Federal Reserve’s rate cut timeline and concerns about upcoming fourth-quarter earnings reports. Investors are closely monitoring earnings releases from major banks such as Bank of America, Wells Fargo, and JPMorgan Chase. Additionally, the cryptocurrency market saw positive momentum, with bitcoin exchange-traded funds (ETFs) rising on their first day of trading following recent rule changes approved by the U.S. Securities and Exchange Commission. Despite a winning session on Wednesday, uncertainties in the economic landscape, including inflation dynamics and corporate earnings, continue to influence market sentiment.

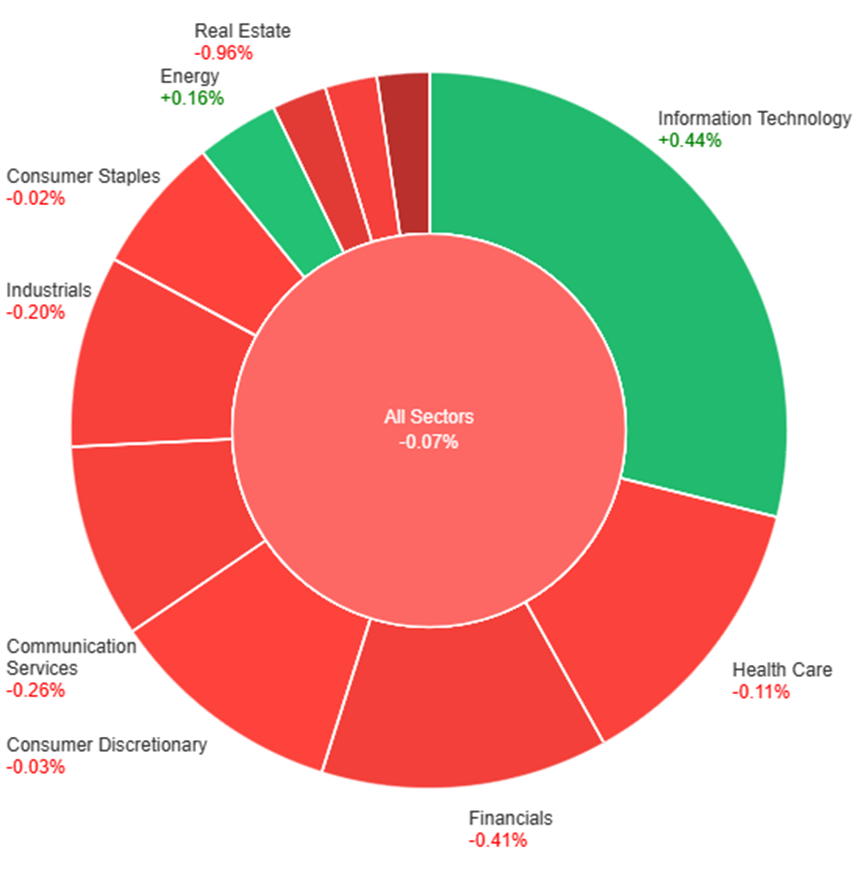

On Thursday, market performance across various sectors showed mixed results. The overall market experienced a marginal decline of 0.07%. The Information Technology sector outperformed others with a positive growth of 0.44%, while Energy and Consumer Staples also exhibited modest gains of 0.16% and 0.02%, respectively. On the downside, Utilities suffered the most significant setback with a substantial decrease of 2.35%. Real Estate also faced a notable decline of 0.96%. Other sectors, including Consumer Discretionary, Health Care, Industrials, Communication Services, Materials, and Financials, reported slight decreases ranging from 0.03% to 0.41%. The diverse performance across sectors reflects a nuanced market landscape on Thursday.

Currency Market Updates

The currency market experienced heightened volatility driven by the release of higher-than-expected US inflation figures in December. The USD Index (DXY) initially surged to new highs near 102.80 as investors reevaluated the possibility of the Federal Reserve reducing interest rates in the second quarter. However, the momentum waned as the session concluded.

EUR/USD briefly touched the 1.1000 mark before a US CPI-driven pullback dragged it down to the 1.0930 zone. Despite the initial setback, the pair managed to recover along with other risk-associated assets. GBP/USD continued its upward momentum, reaching the 1.2770/75 level, approaching the highs seen in 2024. USD/JPY, on the other hand, couldn’t sustain its early gains, retreating to the 145.60 region by the closing bell, influenced by a late corrective decline in the greenback and mixed US yields. In contrast, AUD/USD faced persistent selling pressure, leading to new weekly lows near 0.6650 amid a volatile session in the greenback and mixed activity in the commodity space. USD/CAD advanced to new four-week highs near 1.3440 despite tepid gains in the greenback.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Retreats Below 1.1000 Amidst Surging US Inflation and Fed’s Caution

In Thursday’s trading, the EUR/USD pair faced resistance in breaching the critical 1.1000 level, triggering a notable corrective move following a higher-than-expected rise in US inflation figures for December 2023. The robust US Consumer Price Index (CPI) bolstered the greenback, leading investors to adjust their expectations regarding the Federal Reserve’s potential interest rate cuts in the second quarter. The pair’s downward trend was also influenced by varied performances in US yields across different maturities, prompting investors to reevaluate their bets on potential rate adjustments. Federal Reserve’s L. Mester from Cleveland emphasized that the central bank is not yet considering rate cuts, underlining the necessity for additional evidence of economic progress. Mester highlighted the importance of the Fed fine-tuning its policy for a soft landing, contingent upon sustained declines in inflation. Despite the absence of notable domestic data releases, the US docket revealed a 3.4% year-on-year increase in headline CPI for December and a 3.9% rise in Core CPI. Additionally, weekly Initial Claims climbed by 202,000 in the week ending January 6.

On Thursday, the EUR/USD moved slightly lower, unable to reach the lower band then went back higher and reached the upper band of the Bollinger Bands. Currently, the price moving just around the upper band, suggesting another potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 59, signaling a neutral but bullish outlook for this currency pair.

Resistance: 1.1000, 1.1068

Support: 1.0950, 1.0892

XAU/USD (4 Hours)

XAU/USD Faces Pressure as Stronger-than-Expected US Inflation Boosts Dollar

Stronger-than-anticipated US inflation figures led to a surge in the US Dollar, exerting mild pressure on Gold (XAU/USD) ahead of Wall Street’s opening. Despite hopes for positive figures, the Consumer Price Index rose to 3.4% YoY in December, surpassing both the previous 3.1% and the expected 3.2%. This unexpected inflation surge bolstered the US Dollar in a risk-averse environment, as investors anticipated the Federal Reserve maintaining higher rates for a longer period. The increased likelihood of prolonged rate hikes weighed on the prospects of a rate cut in March, causing stocks to dip and government bond yields to rise, impacting the gold market.

On Thursday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price moving higher above the middle band and trying to reach the upper band. The Relative Strength Index (RSI) stands at 50, signaling a neutral outlook for this pair.

The December U.S. inflation report, releasing on Thursday, will be a focal point for markets.

While core CPI is expected to moderate on a year-over-year basis, the headline gauge is predicted to reaccelerate, posing challenges for the Federal Reserve.

Gold prices, yields, the U.S. dollar, and the Nasdaq 100 are expected to be highly sensitive to the consumer price index data.

The data could influence the Federal Reserve’s future monetary policy decisions, including the timing of the first interest rate cut.

December headline CPI is projected to increase by 0.2% month-over-month, pushing the annual rate to 3.2%, a setback for the Fed aiming for a 2.0% inflation target.

The core gauge is forecasted to rise by 0.3% month-over-month, with the 12-month reading easing to 3.8% from the previous 4.0%.

Market Response Scenarios:

Market response will depend on how the inflation figures align with consensus estimates, considering two scenarios: an upside surprise or lower-than-projected numbers.

Potential Outcomes:

A hot CPI report exceeding forecasts may prompt traders to unwind dovish bets on the Fed’s path, resulting in higher Treasury yields and a stronger U.S. dollar. This could bear negatively on gold, stocks, and indices like the S&P 500 and Nasdaq 100.

Conversely, a benign report with figures milder than anticipated, especially on core metrics, may validate aggressive wagers on rate reductions in 2024. This scenario could be bullish for gold and risk assets.

Market Dynamics:

Current market pricing suggests around 130 basis points of easing for the new year. The resilience of the U.S. economy and signs of stabilization may make the FOMC hesitant to significantly cut borrowing costs, adding significance to the December CPI report.

Focus: Investors seeking clues on Federal Reserve’s interest rate decisions

Expected Inflation Rates:

Annual Headline Inflation: 3.2%

Annual Core Inflation: 3.8% (excluding food and energy)

Importance: Critical for investors, influencing the Fed’s monetary policy and potential interest rate cuts

Market Expectations:

Bank of America expects slightly higher readings than consensus, leaving room for a Fed rate cut in March.

Markets currently price in a roughly 67% chance of a Fed rate cut in March.

Monthly Changes (December):

Overall Prices: Expected to increase by 0.2%

Core Inflation: Expected to increase by 0.3%

Key Areas to Watch (Goldman Sachs):

Car prices and shelter expected to continue declining.

Airfares could pose an upside risk, with a potential 5% increase in December.

Fed Officials’ Comments:

Fed officials, including Governor Michelle Bowman and Atlanta Fed President Raphael Bostic, show a measured approach.

Bowman suggests a potential rate cut if inflation falls further, while Bostic emphasizes the need to evolve with the economy.

Market Reaction Expectations: Wall Street strategists temper expectations for stock reactions, considering an already aggressive rally and potential asymmetric risk in CPI numbers.

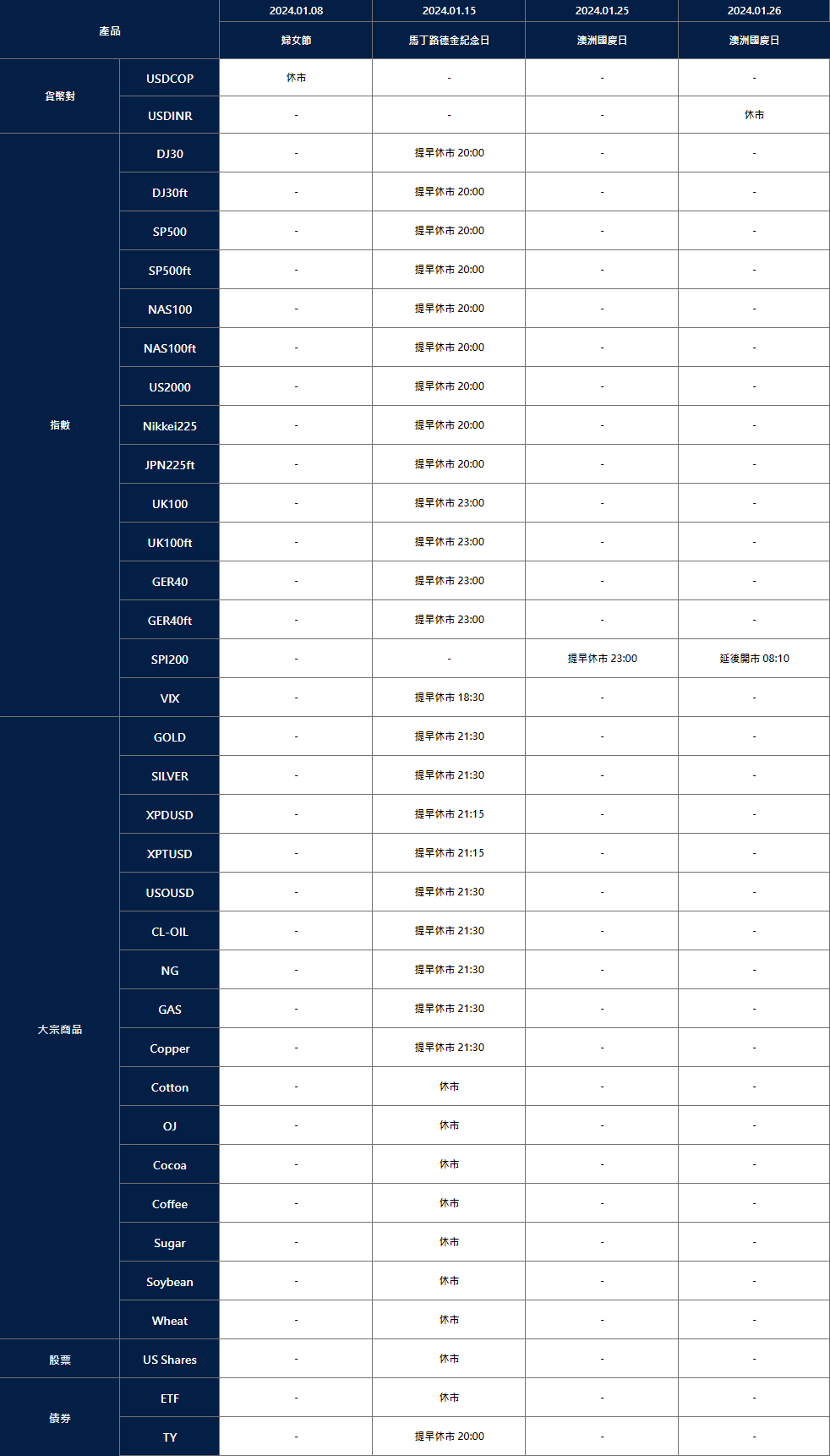

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the remaining affected products:

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a bullish session, stocks closed higher with the S&P 500, Dow Jones, and Nasdaq posting gains fueled by positive earnings reports, particularly from Intuitive Surgical and Lennar. Investor attention is now focused on the eagerly awaited consumer price index (CPI) report and producer price index, with expectations influencing speculation about potential shifts in Federal Reserve interest rate policies. The dollar index declined slightly due to gains against the yen and losses versus the euro, influenced by yield spreads and economic indicators. Meanwhile, the Bank of Japan maintains caution in unwinding monetary policies, while the eurozone faces economic concerns. Sterling rose, supported by higher gilts-Treasury yield spreads, despite BoE rate cuts pricing lower than the Fed’s.

Stock Market Updates

Stocks closed higher on Wednesday, driven by anticipation surrounding the upcoming release of fresh U.S. inflation data and corporate earnings reports. The S&P 500 rose by 0.57% to close at 4,783.45, the Dow Jones Industrial Average added 170.57 points (0.45%) to reach 37,695.73, and the Nasdaq Composite advanced 0.75% to settle at 14,969.65. Intuitive Surgical and Lennar played pivotal roles in lifting the market, with both companies experiencing notable stock increases of 10.3% and 3.5%, respectively. Intuitive Surgical raised its procedure growth outlook for fiscal year 2024, while Lennar announced an increase in its annual dividend.

Investor focus is now shifting towards the awaited consumer price index (CPI) report scheduled for release on Thursday, with expectations of a 3.2% year-over-year increase in December. Additionally, the producer price index is set for release on Friday. Investors are closely monitoring these reports for insights into potential shifts in the Federal Reserve’s interest rate policies, with current expectations hovering around a 64% likelihood of rate cuts, according to the CME Group FedWatch tool. The upcoming earnings season adds to the market’s dynamics, with major financial heavyweights like JPMorgan Chase, Bank of America, UnitedHealth, and Delta Air Lines set to reveal their results on Friday. Despite a mixed session on Tuesday, stocks exhibited positive momentum on Wednesday.

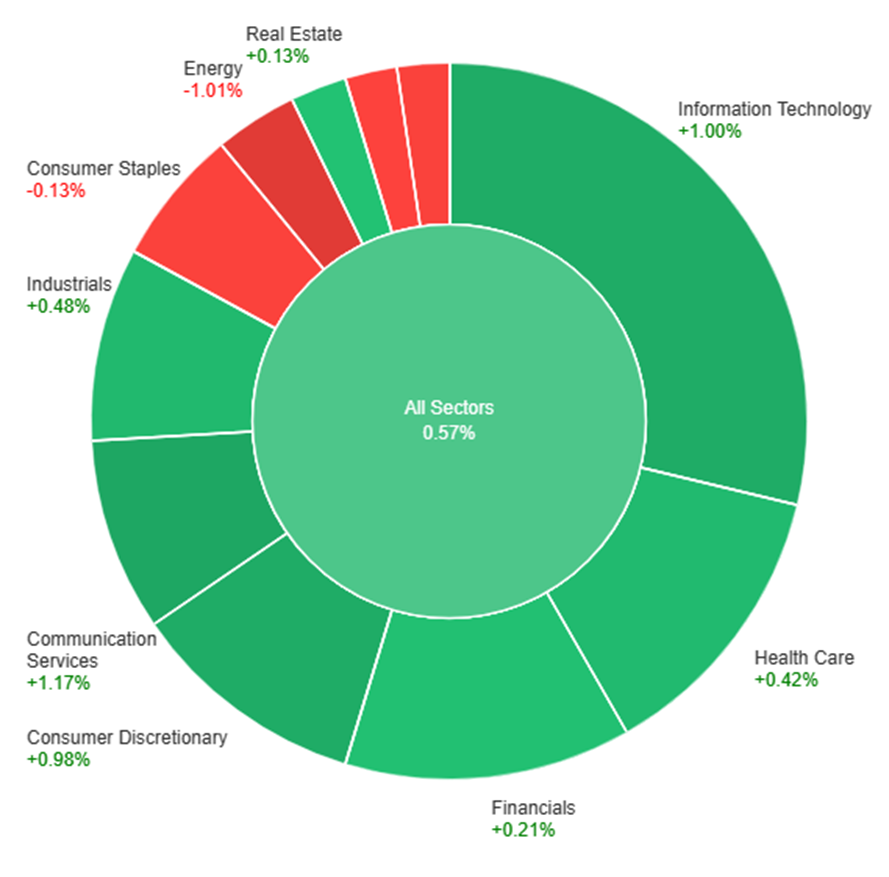

On Wednesday, the overall market exhibited a positive trend with a gain of 0.57%. Notable sector performances include Communication Services and Information Technology, both experiencing substantial increases at +1.17% and +1.00%, respectively. Consumer Discretionary and Industrials also contributed to the positive momentum with gains of +0.98% and +0.48%. Health Care and Financials showed more modest increases at +0.42% and +0.21%. On the flip side, Energy suffered a notable decline of -1.01%, dragging down the overall performance. Utilities and Consumer Staples experienced marginal losses at -0.06% and -0.13%, while Real Estate and Materials also showed slight decreases at +0.13% and -0.17%.

Currency Market Updates

The dollar index experienced a 0.1% decline, driven by notable gains against the vulnerable yen and losses versus the euro. This shift was influenced by the widening 2-year bund-Treasury yield spreads, reaching their highest point since July. The euro’s strength was partly attributed to comments made by ECB hawk Isabel Schnabel. Meanwhile, the Japanese yen faced broad selling pressure as Japanese data revealed a mere 1.2% rise in regular wages and a 3.0% year-on-year decline in real wages for November. This decline underscores persistent inflation concerns and a lack of domestic demand-driven wage growth, aligning with the Bank of Japan’s reluctance to end negative rates.

As the Japanese household spending continued to plummet, acting as a drag on growth and reinforcing disinflation in the December Tokyo CPI report, the BoJ governor expressed a cautious approach towards unwinding ultra-loose monetary policies. In contrast, the U.S. market anticipates the CPI report, assessing the likelihood of a soft landing and potential cuts to the Fed’s 5.5% policy rate compared to the BoJ’s -0.1% rate. The accommodative BoJ policies contributed to the Nikkei 225 reaching its highest point since the 1990s bubble, fostering risk-on sentiment and positively correlating with the rise of USD/JPY towards the key resistance. Meanwhile, EUR/USD showed a 0.34% increase, approaching the 10-day moving average but staying within the range set by Friday’s U.S. jobs data. ECB policymakers highlighted a tepid economic recovery outlook in the eurozone, anticipating a recession in late 2023, driven by concerns about the German property market and supply chain risks. Sterling saw a 0.24% rise, supported by higher gilts-Treasury yield spreads, despite remaining below the November and December highs, as the BoE’s 2024 rate cuts priced roughly 30bp less than those for the Fed.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Ground Amidst Greenback’s Downside Pressure and Market Optimism

In response to a renewed downside bias in the greenback, EUR/USD rebounded, reaching two-day highs in the 1.0965/70 range. The firm optimism in the risk space on Wednesday contributed to the climb, as the USD Index (DXY) faced pressure, retreating to the 102.30 region. Factors such as the absence of clear direction in US yields, an uptick in Germany’s 10-year bund yields, and prevailing risk-on sentiment influenced the pair’s daily movement. Despite a lack of clarity in US yields and rising 10-year bund yields, the focus now shifts to the upcoming US inflation readings, set to be a crucial driver for the dollar’s price action, considering the Federal Reserve’s potential interest rate reductions in the second quarter. Conversely, comments from ECB’s De Guindos and Schnabel regarding a soft landing in the Eurozone’s economy and a reachable inflation target in 2025 had limited impact on the pair. Suggestions of premature interest rate cuts by the ECB, despite speculations of potential reductions, did not significantly sway the market.

On Wednesday, the EUR/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just around the upper band, suggesting another potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 59, signaling a neutral but bullish outlook for this currency pair.

Resistance: 1.1000, 1.1068

Support: 1.0950, 1.0892

XAU/USD (4 Hours)

XAU/USD Hovers as Investors Await Key CPI Data Amidst Lethargic Trading

Gold (XAU/USD) continues to tread familiar levels, showing limited movement amid a cautious market environment marked by a sparse macroeconomic calendar. The precious metal recently touched a weekly low at $2,016.61 and faces support at various levels. As Wall Street maintains a positive but uneventful stance, anticipation builds for the upcoming release of the December Consumer Price Index (CPI) in the United States. Analysts predict a 3.2% annualized increase, with a potential impact on the US Federal Reserve’s rate-cutting decisions. The gold market remains on edge, awaiting CPI readings that could influence sentiment and guide the trajectory of the US Dollar in the coming days.

On Wednesday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price moving higher and trying to reach the middle band. The Relative Strength Index (RSI) stands at 45, signaling a neutral outlook for this pair.

Stagnant US Dollar: The US dollar remains relatively unchanged in today’s opening trade, leading to a state of uncertainty for USD pairs.

Consolidation Phase: The US dollar index is currently consolidating its recent upward movement. The lack of direction from the rates market is expected to persist until the release of the upcoming US inflation report on Thursday at 13:30 UK time.

Market Expectations: Financial markets are currently factoring in a total of 150 basis points in US interest rate cuts for the year. The initial 25 basis point adjustment is anticipated at the March 20th FOMC meeting.

Chart Analysis: The US dollar index chart illustrates a short-term consolidation, with last Friday’s jobs report candle acting as a constraining factor. Conflicting moving averages, including the 20-day sma supporting the dollar index and the 50-/200-day sma forming a potential negative ‘death cross,’ present a mixed outlook.

Fibonacci Retracement: The dollar index is positioned on the 61.8% Fibonacci retracement of the mid-July to early-October movement.

Financial Markets Analysis:

STOCK MARKET:

Market Turbulence: The crypto community experienced a surge in Bitcoin’s price to nearly $48,000 following an apparent announcement on X (formerly Twitter) by the Securities and Exchange Commission (SEC) regarding the approval of spot Bitcoin exchange-traded funds (ETFs).

SEC Chair’s Clarification: Within fifteen minutes, SEC Chair Gary Gensler declared the message as “unauthorized” and inaccurate, stating that the SEC’s X account had been “compromised,” and the tweet was unauthorized. He emphasized that the SEC had not approved spot Bitcoin ETFs.

Price Fluctuation: Bitcoin’s value retreated to $45,500 after Gensler’s clarification, resulting in a loss of $63 billion in market value within minutes.

Official Statement: The SEC, through a spokesperson, clarified that the unauthorized message on X was not made by the SEC or its staff. The agency confirmed unauthorized access to its X account and pledged to investigate the incident.

ETF Approval Speculation: The incident added to the market frenzy around the potential approval of Bitcoin ETFs, seen as a significant development for widespread acceptance of the cryptocurrency.

Market Expectations: Some applicants anticipated SEC approval on Wednesday, with trading potentially commencing on Thursday. However, Gensler’s statement contradicted these expectations.

Notable Applicants: Major names on Wall Street, including BlackRock and Franklin Templeton, applied for spot Bitcoin ETFs. JPMorgan Chase and Goldman Sachs offered assistance to these money managers.

Industry Impact: Stakeholders believe that spot Bitcoin ETFs could attract substantial capital into Bitcoin, potentially elevating its price.

Price Prediction: Analysts estimate that financial products related to spot Bitcoin ETFs could attract $10 billion or more in investment flows by the end of 2024, potentially pushing Bitcoin’s price higher.

Crypto Risks Warning: Gensler, in a recent statement, reiterated the risks associated with crypto investments, emphasizing their volatility and susceptibility to insolvency.

Optimistic Outlook: Despite past challenges, the crypto industry anticipates wider acceptance and regulatory clarity, with optimism surrounding Bitcoin’s “halving” in April and potential interest rate cuts in 2024.

Long-Term Prediction: Analysts predict Bitcoin reaching $150,000 by 2025, considering various factors, including regulatory developments and industry changes.

{kind=link}