Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Stocks experienced volatility on Wednesday as the Federal Reserve took a pause in its rate-hiking campaign while signalling progress in combating inflation. Despite this, the central bank also indicated its intention to implement two more rate hikes later in the year.

The S&P 500 managed to eke out a marginal gain, closing at 4,372.59 with a 0.08% increase, while the Nasdaq Composite saw a 0.39% rise to end the session at 13,626.48, supported by strong performances from Nvidia and AMD.

On the other hand, the Dow Jones Industrial Average dipped by 0.68%, or 232.79 points, closing at 33,979.33, primarily due to losses in UnitedHealth. Notably, both the S&P 500 and the Nasdaq reached their highest levels since April 2022 during the trading session.

As anticipated by traders, the Federal Reserve announced the maintenance of unchanged interest rates, breaking a streak of 10 consecutive rate hikes. However, the markets initially responded negatively as investors focused on the central bank’s projections, which indicated an imminent resumption of rate hikes. Ed Moya, senior market analyst at Oanda, expressed concerns over the Fed’s forecast, stating that the statement and projections were so hawkish that Wall Street may regret not raising rates that day.

Nonetheless, the sell-off stabilized to some extent when Fed Chair Jerome Powell, during the subsequent press conference, revealed that no decision had been made regarding the July meeting and emphasized the Fed’s progress in tackling inflation.

With the S&P 500 up over 13% this year and more than 25% from its bear market low, investors had been betting on the Fed’s impending cessation of rate hikes. Furthermore, recent economic indicators, such as May’s producer price index and consumer price index, have fueled optimism that the Fed is effectively combating inflation. The Federal Reserve’s next meeting is scheduled for July 25-26.

On Wednesday, the stock market witnessed mixed performances across various sectors. The Information Technology sector led the gains with a significant increase of 1.14%. Consumer Staples and Real Estate sectors also recorded positive growth, rising by 0.56% and 0.32% respectively. Communication Services saw a modest gain of 0.13%.

However, several sectors experienced losses, with Energy and Health Care both declining by 1.12%. Financials, Materials, and Industrials sectors also faced declines of 0.37%, 0.43%, and 0.29% respectively. The Utilities sector saw a slight decrease of 0.07%, while Consumer Discretionary recorded a minor loss of 0.11%. Overall, Wednesday’s trading session displayed a mixed performance across sectors, reflecting the varied market dynamics of the day.

Major Pair Movement

The US Dollar Index (DXY) dropped to its lowest level in a month, reaching around 102.95, as market sentiment leaned towards a dovish stance for the US Federal Reserve (Fed). The Fed decided to keep interest rates unchanged, signalling a pause in the rate hike trajectory.

However, the Fed Chair, Jerome Powell, delivered a bullish speech and hinted at a possible rate hike in July. The dot plot projections showed an increase in rates for 2024 and 2025, and the median rate forecasts suggested two more rate increases in 2023.

Despite the hawkish signals from the Fed, the EUR/USD continued to rise and closed at its highest level in a month above 1.0800. Attention now shifts to the upcoming European Central Bank (ECB) meeting, where a 25 basis point interest rate hike is expected.

The language used in the ECB’s statement and President Lagarde’s comments during the press conference will be crucial for the Euro’s performance. If the meeting turns out to be dovish, with hints of a potential pause in rate hikes, the Euro could face downward pressure. In the meantime, market focus will also be on key US economic data such as Retail Sales, Jobless Claims, and the Philly Fed Index.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rises to Monthly High Despite US Dollar Recovery and Hawkish FOMC; Focus Shifts to ECB Meeting and US Data

The EUR/USD pair achieved its highest daily close in a month above 1.0800, disregarding the US Dollar’s rebound following the hawkish stance of the Federal Open Market Committee (FOMC). Market attention now turns towards the upcoming European Central Bank (ECB) meeting and crucial US economic data, which gain significance in light of Fed Chair Powell’s indication that the July meeting will be a “live” session.

The ECB is expected to raise interest rates by 25 basis points, with the language used in the statement and President Lagarde’s comments during the press conference holding key implications for the Euro’s performance.

Meanwhile, the US dollar gained ground after the FOMC meeting, as the central bank hinted at future rate hikes and projected additional tightening measures by year-end. Market sentiment will likely be influenced by the Fed’s decision and forthcoming US economic indicators, including Retail Sales, Jobless Claims, and the Philly Fed Index.

According to technical analysis, theEUR/USD pair experienced an upward movement on Wednesday and was able to reach the upper band of the Bollinger Bands. It then slowly moved lower, targeting the middle band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 55, lower than the previous higher movement, indicating that the EUR/USD might be returning to a neutral stance.

Resistance: 1.0847, 1.0893

Support: 1.0757, 1.0721

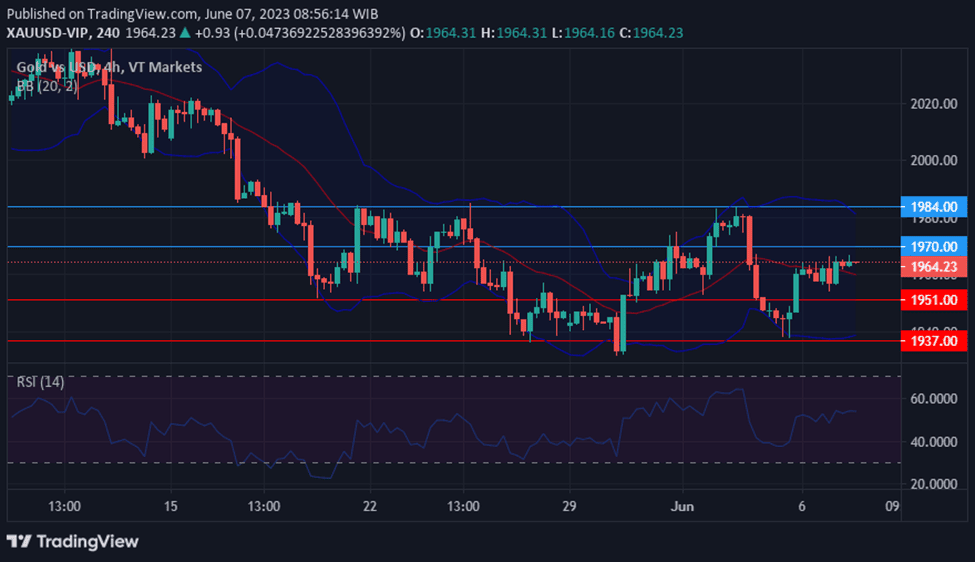

XAU/USD (4 Hours)

XAU/USDHolds Steady Amidst Dovish Fed Outlook, Focusing on Monetary Policy Announcement and Dot Plot

XAU/USD maintains modest gains within the $1,950 price range as investor sentiment improves following US inflation data supporting a dovish Federal Reserve (Fed). The Consumer Price Index (CPI) rose slower than expected in May, while the Producer Price Index (PPI) contracted, indicating downward pressure on prices and validating the Fed’s previous monetary policy measures. Although concerns persist over a tight labor market potentially driving inflation higher, policymakers have anticipated a more dovish approach and a meeting-by-meeting decision.

The market expects the Fed to hold its current stance, with the upcoming monetary policy announcement, dot plot release, and Chairman Jerome Powell’s press conference being the focal points. Market optimism regarding a conservative Fed aiding the economy in avoiding a recession has led investors to seek high-yielding assets, temporarily overshadowing XAU/USD. However, if the Fed deviates from market expectations, significant price volatility can be anticipated, with XAU/USD responding to fluctuations in the broader strength or weakness of the US Dollar.

According to technical analysis, the XAU/USD pair is moving lower creating a push to the lower band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 36, indicating that the XAU/USD is still in a bearish condition.

Stocks climbed as new inflation data revealed a slowdown in price pressures in May, fueling optimism among investors that the Federal Reserve might opt to forgo a rate hike during its upcoming policy decision this week. The Dow Jones Industrial Average, S&P 500, and Nasdaq Composite all experienced gains, with the latter two indices reaching their highest closing levels since April 2022. The consumer price index for May showed a 4% year-over-year increase, the slowest annual rate since March 2021, prompting traders to increase their bets on the Fed maintaining the current target rate of 5% to 5.25%. This sentiment was further supported by market expectations and speculation of a “skip” rather than an extended pause in rate hikes.

Tech shares, in particular, led the market surge, benefiting from the positive outlook driven by easing inflation and interest rates. Oracle shares saw a 0.2% increase following better-than-expected results for the fiscal fourth quarter, while streaming giant Netflix experienced a 2.8% climb. Overall, the market responded favorably to the inflation data, reinforcing expectations that the Fed may adopt a cautious approach and provide further clarity on its rate hike plans to maintain stability and assess the impact of prior rate increases.

On Tuesday, the overall market showed a positive trend with a 0.69% increase across all sectors. The Materials sector had the highest gain, rising by 2.33%, followed by Industrials at 1.16% and Consumer Discretionary at 1.00%. Information Technology also saw a modest increase of 0.71%. Real Estate and Financials sectors both showed a 0.62% gain, while Health Care and Energy had smaller gains of 0.53% and 0.47%, respectively. Consumer Staples and Communication Services sectors experienced more modest gains with increases of 0.42% and 0.27%, respectively. However, the Utilities sector showed a slight decline with a decrease of 0.06%.

Major Pair Movement

On Tuesday, the US dollar experienced a decline against the euro and sterling, as US CPI data indicated that the Federal Reserve would likely not raise interest rates during their upcoming meeting. This news also increased expectations of tighter monetary policy from the Bank of England. The dollar had already been weakening due to risk-on sentiment and pre-Fed selling. While Treasury yields initially dropped, they later rebounded, but the dollar only managed to gain against the yuan and the yen, which had been affected by the Bank of Japan’s efforts to support economic growth. The biggest winner among the major currencies was sterling, which saw a surge after positive UK economic data, including rising average hourly earnings, increased employment, and a lower jobless rate.

EUR/USD experienced a slight gain after Treasury yields recovered, although it encountered resistance from various technical indicators. The European Central Bank is expected to raise rates at upcoming meetings but then enter a period of keeping rates steady. USD/JPY recovered with a 0.46% gain, supported by a rise in 2-year Treasury yields. To surpass previous highs, it may require a more hawkish stance from the Federal Reserve.

Overall, the US dollar faced downward pressure against major currencies on Tuesday, while sterling emerged as a strong performer due to positive economic indicators, and the outlook for central bank actions played a significant role in influencing market sentiment.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Reacts to Inflation Data and Central Bank Meetings Amidst Volatility and Risk Appetite

The EUR/USD pair initially rose above 1.0820 on Tuesday following US inflation data but later retreated to around 1.0780 due to high government bond yields and risk appetite. Despite finishing positively, the pair remained far from its peak. The overall sentiment is bullish, but volatility is anticipated as the market awaits the FOMC meeting and the European Central Bank (ECB) decision.

German inflation data indicated a 6.1% annual increase in May, while the German ZEW survey improved unexpectedly in June. The US Consumer Price Index (CPI) for May showed a 0.1% rise, lower than expected, with an annual rate of 4%, suggesting a slowdown in inflation. This data could lead the Federal Reserve to pause its tightening cycle. The US Dollar initially fell but later recovered amid risk appetite and rising government bond yields. The future direction of the EUR/USD pair is expected to be influenced by the US Dollar’s performance ahead of the FOMC statement, with attention on economic projections and guidance from Federal Reserve Chair Jerome Powell.

According to technical analysis, theEUR/USD pair experienced an upward movement on Tuesday and was able to reach the upper band of the Bollinger Bands. It then slowly moved lower, targeting the middle band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 58, lower than the previous higher movement, indicating that the EUR/USD might be returning to a neutral stance.

Resistance: 1.0808, 1.0847

Support: 1.0757, 1.0721

XAU/USD (4 Hours)

Optimism Reigns as Soft US Inflation Data Fuels Dovish Expectations; Gold (XAU/USD) Trades Near Daily Lows

In response to softer-than-anticipated US inflation figures, Spot Gold (XAU/USD) traded near a daily low of $1,942 as optimism prevailed. The US Dollar experienced a decline throughout the day, further accelerating as the Consumer Price Index (CPI) fell below market expectations. The Bureau of Labor Statistics reported a 0.1% month-on-month rise in May’s CPI, accompanied by a 4% year-on-year increase, with the core annual CPI easing from 5.5% to 5.3%. These figures bolstered expectations of a dovish Federal Reserve (Fed), which is set to announce an update on monetary policy. Meanwhile, global stock markets embraced the positive news, while XAU/USD, after reaching a peak of $1,970.96 following the CPI release, felt the weight of optimism.

According to technical analysis, the XAU/USD pair is moving lower due to a shift in market sentiment towards risk-on conditions following lower-than-expected US inflation data. The XAU/USD has reached the lower band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 40, indicating that the XAU/USD is still in a bearish condition but has the potential to move slightly higher towards the middle band of the Bollinger Bands.

The S&P 500 soared to its highest level in over a year as traders anticipated that the Federal Reserve would refrain from raising interest rates during their policy meeting. The index closed at 4,338.93, surpassing its previous high from August and marking the best intraday and closing levels since April 2022. The Nasdaq Composite also experienced significant gains, reaching its highest point since April 2022, while the Dow Jones Industrial Average climbed to 34,066.33.

Market expectations indicate a high probability that the Fed will skip a rate hike this month, with investors pricing in a 72% chance of no increase. While the June hike seems unlikely, the central bank may continue raising rates in the future. Inflation data, expected to show a drop in May’s consumer price index, could support the notion that inflation is receding, reinforcing the case for holding rates steady. Many anticipate that the Fed will emphasize its commitment to controlling inflation and potentially implement a final rate increase at the July meeting before pausing for the rest of the year.

The recent surge in the S&P 500, which gained over 20% from its October low, has sparked optimism among investors, signalling the end of the bear market. The index has experienced a four-week winning streak, while the Nasdaq Composite has seen an even more substantial increase, rising 33% from its 52-week low. On Monday, technology stocks, including Amazon and Tesla, led the market’s upward trajectory, with each stock gaining over 2%.

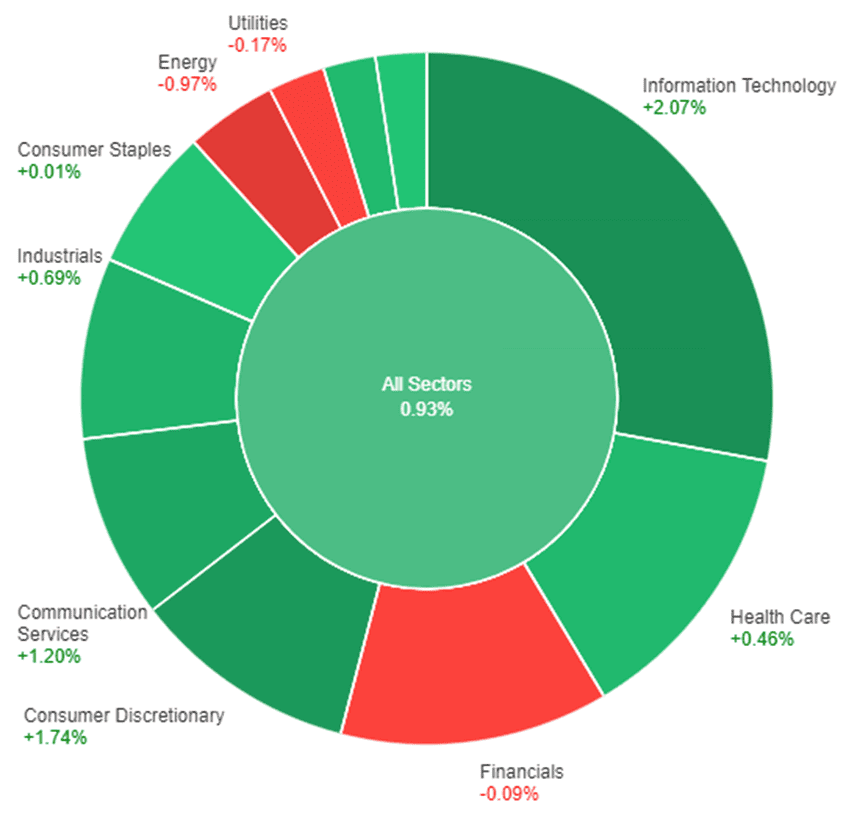

On Monday, the overall market saw a positive trend, with all sectors collectively increasing by 0.93%. The Information Technology sector performed exceptionally well, with a significant rise of 2.07%. The Consumer Discretionary and Communication Services sectors also experienced substantial gains, growing by 1.74% and 1.20% respectively. The Industrials and Health Care sectors followed suit, showing modest growth of 0.69% and 0.46% respectively. The Materials sector and Real Estate sector saw smaller increases of 0.44% and 0.03% respectively. The Consumer Staples sector and Financials sector experienced minimal gains, with a rise of only 0.01% and a slight decline of 0.09% respectively. On the other hand, the Utilities and Energy sectors faced declines, with drops of 0.17% and 0.97% respectively.

Major Pair Movement

The dollar index initially declined but later recovered as Treasury yields rebounded in cautious trading ahead of the U.S. CPI release, as well as the Federal Reserve and European Central Bank meetings. The dollar and yields received a boost from a sizable $72 billion Treasury issuance, while billionaire investor Ray Dalio expressed concerns about a forthcoming financial crisis and suggested equities would outperform risky U.S. Treasuries. Following the auctions, EUR/USD remained largely unchanged, and the yield curve steepened, with 2s remaining flat and a 2.5 basis point increase in 10s.

Market expectations continue to support the Fed’s guidance of skipping a rate hike this week, with another 25-basis point increase likely in July and potential cuts starting in December, though significantly lower than initial projections in early May. The ECB is priced for a 25-basis point rate hike on Thursday, followed by another in July, and a rate cut is expected by April. Sterling experienced the most notable movement among major currencies, falling by 0.63% due to surging gilts yields and increasing UK political risk. The Bank of England is still seen as needing to raise rates by at least another 100 basis points to address inflation concerns, with average hourly earnings forecasted to rise in Tuesday’s April employment report.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds within Familiar Range as Market Awaits Key Economic Data and Central Bank Meetings

The EUR/USD pair saw a modest rise on Monday, remaining below the 1.0800 level while showing limited corrections and potential for upside movement. The upcoming US inflation data on Tuesday, alongside the Federal Reserve (Fed) and European Central Bank (ECB) meetings later in the week, are expected to shape the pair’s next direction. This week holds significant importance for financial markets, with the focus on the US Consumer Price Index (CPI) for May and the interest rate decisions from the Fed and ECB. Volatility and potential for erratic moves are expected, making stability more likely after the ECB meeting on Thursday.

According to technical analysis, theEUR/USD pair experienced an upward movement on Monday, with the price trading along and above the middle band of the Bollinger Bands. At present, the EUR/USD is still hovering around the middle band of the Bollinger Bands, suggesting that there is a possibility that the market is awaiting the next movement, but the overall sentiment remains bullish. The Relative Strength Index (RSI) is currently at 57, indicating that the EUR/USD is still in a bullish trend.

Resistance: 1.0808, 1.0847

Support: 1.0757, 1.0721

XAU/USD (4 Hours)

Gold (XAU/USD) Dips on Positive Market Sentiment, Investors Await Key Data and Central Bank Decisions

On Monday, spot gold (XAU/USD) prices fell to a daily low of $1,949.20 per troy ounce due to a more positive market sentiment driven by global stock recoveries. Investors are cautious as they await crucial data releases and monetary policy decisions from central banks, including the Federal Reserve (Fed). The unexpected rate hikes by the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) have raised doubts about the conclusion of the tightening cycle in the US. The upcoming release of the US Consumer Price Index for May will provide further insights, with expectations of a slight decrease in inflation. This week also features monetary policy decisions from the ECB, BoJ, and PBoC, shaping the overall market outlook.

According to technical analysis, the XAU/USD pair is trending lower on Monday as the market awaits today’s US inflation data. The XAU/USD is currently trading around the middle band of the Bollinger Bands, indicating a possibility of a slight upward movement throughout the day. At present, the Relative Strength Index (RSI) stands at 48, suggesting that the XAU/USD is in a neutral state and is awaiting further developments.

In the week ahead, market participants will be closely monitoring several vital economic events, including interest rate decisions by major central banks and the release of US Producer Price Index (PPI) and Consumer Price Index (CPI) data.

Market watchers and financial experts are expected to pay close attention to these releases, eager to understand their potential impact on financial markets and the global economy as a whole.

US Consumer Price Index (13 June 2023)

US CPI rose 0.4% month-over-month in April 2023, higher than the 0.1% increase seen in March.

Analysts anticipate a 0.3% rise for May data, scheduled for release on 13 June 2023.

US Producer Price Index (14 June 2023)

Producer prices for final demand in the US increased 0.2% month-over-month in April 2023, following a downwardly revised 0.4% drop in March.

For May 2023 data, set to be released on 14 June 2023, analysts expect a 0.1% increase.

US FOMC Meeting Minutes (14 June 2023)

During its May meeting, the Fed increased the Fed funds rate by 25bps, reaching a range of 5%-5.25%. This marks the 10th hike, setting borrowing costs at their highest since September 2007.

For the upcoming meeting on 14 June 2023, analysts forecast that the Fed will hold the rate steady at 5.25%.

Australia Employment Change (15 June 2023)

In April 2023, Australia’s employment saw an unanticipated drop of 4,300, bringing the total to 13.88 million. The unemployment rate increased unexpectedly to 3.7%.

Data for May 2023 is scheduled for release on 15 June 2023, and analysts predict a 20,000 rise in employment with the unemployment rate staying at 3.7%.

European Central Bank Main Refinancing Rate (15 June 2023)

During its May meeting, the ECB raised its key interest rates by 25 bps to 3.75%, signalling a slower pace of policy tightening. In a press conference, President Lagarde mentioned that the ECB still had progress to make and did not intend to halt the cycle of rate increases soon.

Analysts anticipate that for June, the central will increase its interest rates by 25 bps to 4.0%.

US Retail Sales (15 June 2023)

Retail sales in the US increased 0.4% month-on-month in April 2023, rebounding from two consecutive months of declines.

For May 2023 data, which will be released on 15 June, analysts expect a 0.5% increase.

BOJ Rate Statement (16 June 2023)

In April, the Bank of Japan unanimously voted to maintain its key short-term interest rate at -0.1% and 10-year bond yields at around 0%. They also altered guidance on their policy rate by removing references to guarding against risks from the COVID pandemic and maintaining interest rates at “current or lower levels.”

Analysts predict that for June, the rate will remain unchanged.

U.S. stock futures experienced a slight decline on Thursday night, even as the S&P 500 reached its highest closing level of the year. Dow Jones Industrial Average futures dropped by 54 points, equivalent to 0.16%, while S&P 500 futures saw a 0.12% dip and Nasdaq 100 futures edged down by 0.08%.

In extended trading, DocuSign shares surged by 5% after the electronic agreements firm exceeded analysts’ expectations for the first quarter, both in terms of revenue and profit. During the regular trading session on Thursday, stocks continued their recent rally, resulting in the S&P 500 reaching a notable level just below 4,300. The broader index recorded a 0.62% climb to close at 4,293.93. Simultaneously, the Dow Jones Industrial Average enjoyed its third consecutive day of gains, adding 168.59 points or 0.5%. The Nasdaq Composite also performed well, rallying by 1.02%.

Investors found encouragement in the broader participation of stocks, including small-cap equities, in the ongoing market rally. However, some market participants cautioned that the gains may not be sustainable, questioning whether this is a short-lived position squeeze reminiscent of August 2022 or a more enduring trend. The current state of the market is perceived as a potential turning point, leading to uncertainty regarding its future trajectory.

While the S&P 500 is set for its fourth consecutive positive week, a feat not seen since last August, with a modest increase of nearly 0.3% as of Thursday’s close, the Dow Jones Industrial Average is on track for its second consecutive week of gains, up 0.2%—a development unseen since April. On the other hand, the Nasdaq Composite is poised to break its six-week winning streak, with a slight decline of 0.02%.

On Thursday, most sectors of the market experienced a positive performance. Consumer Discretionary showed the strongest gain, rising by 1.56%. Information Technology also had a notable increase of 1.20%. Consumer Staples and Health Care sectors followed with gains of 0.74% and 0.65%, respectively. Utilities and Communication Services sectors showed modest gains of 0.41% and 0.27%, while Industrials had a slight increase of 0.18%.

However, not all sectors saw gains on Thursday. Financials experienced a decline of 0.11%, while Materials and Energy sectors saw larger losses of 0.35% and 0.44%, respectively. The Real Estate sector had the largest decline, dropping by 0.62% on the day. Overall, it was a mixed day for sectors, with most sectors posting gains, but some sectors facing losses.

Major Pair Movement

The dollar experienced a decline on Thursday, accompanied by a drop in Treasury yields, causing concern among traders who held long positions ahead of the upcoming Federal Reserve meeting. Despite some policymakers hinting at a possible pause in interest rate hikes, surprise rate increases from the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) led to speculation that the Federal Reserve might follow suit. The market pricing for Fed policy did not change significantly following the report, with expectations still indicating a likelihood of no rate hike in June, a final 25 basis point hike in July, and the possibility of rate cuts starting from December onwards. The increase in initial jobless claims, along with other indicators of slowing growth, added to worries about global economic conditions.

Meanwhile, the euro gained 0.75% against the dollar, finding resistance near the daily cloud base and the 100-day moving average. The British pound also climbed 0.9% against the dollar, as the Bank of England (BoE) was expected to raise rates, bringing them closer to the levels set by the Federal Reserve. On the other hand, the USD/JPY pair declined by 0.85%, approaching its 21-day moving average and key support levels. The focus of the market now shifts to the upcoming meetings of the Federal Reserve, the European Central Bank (ECB), and the Bank of Japan (BoJ).

Overall, the dollar weakened, Treasury yields declined, and various factors, including global economic growth concerns, upcoming central bank meetings, and the performance of other major currencies, influenced the currency market on Thursday.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges as Weaker US Dollar Boosts Sentiment Ahead of FOMC Meeting

The EUR/USD currency pair experienced a notable upswing on Thursday, driven by a declining US Dollar and improved risk appetite. The Greenback weakened across the board following lackluster employment data from the US, which softened expectations ahead of the upcoming Federal Open Market Committee (FOMC) meeting. Although Euro area Q1 GDP saw downward revisions, it did not have a significant impact on the Euro’s performance. Despite mixed growth figures among European countries, the European Central Bank (ECB) meeting next week is still anticipated to include a 25 basis points rate hike. The rally in EUR/USD was further supported by technical factors, while the negative employment numbers in the US contributed to easing hawkish expectations from the Federal Reserve. The release of the May Consumer Price Index (CPI) on Tuesday will be a crucial report to watch before the FOMC decision. As market sentiment favors riskier assets, the US Dollar is expected to remain weak, potentially leading to further losses. However, a deterioration in sentiment could limit upward movements and facilitate a sharp correction in the currency pair.

According to technical analysis, theEUR/USD pair moved higher on Thursday as the price creating a push to the upper band of the Bollinger Bands. Currently, the EUR/USD is still running around the upper band of the Bollinger Bands showing that there’s a possibility that the market still trying to move higher. The Relative Strength Index (RSI) is currently at 66 just below the overbought area, indicating that the EUR/USD is still in the bullish trend.

Resistance: 1.0808, 1.0847

Support: 1.0757, 1.0721

XAU/USD (4 Hours)

Gold (XAU/USD)Rallies as Weaker US Dollar and Dismal Employment Report Spur Investor Sentiment

After hitting a weekly low of $1,939 per troy ounce, the XAU/USD pair staged an impressive comeback. The US Dollar initially traded with a soft tone, but its decline accelerated during American trading hours, triggered by a worse-than-expected employment-related report. Initial Jobless Claims unexpectedly surged to 261K for the week ended June 2. The disappointing data pushed investors to increase bets on a dovish Federal Reserve (Fed), with the odds of a rate hike next week surpassing 70% once again. The unexpected interest rate hikes by the Bank of Canada (BoC) and the Reserve Bank of Australia (RBA) also contributed to doubts about the US tightening cycle. Additionally, the US Dollar was influenced by a sharp retracement in government bond yields, with both the 10-year and 2-year Treasury yields experiencing a decline.

According to technical analysis, the XAU/USD pair is moving higher on Thursday and try to cover the losses on previous day, moves higher above the middle band of the Bollinger Bands. There is a possibility that the XAU/USD will continue to moves higher and try to create a push to the upper band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 54, suggesting that the XAU/USD is in neutral with potential bullish trend.

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

10th of June 2023 (Saturday) 02:00 – 11:00 (GMT+3)

Please note that the following aspects might be affected during the maintenance:

1. The price quote feature on the Client Portal will be temporarily unavailable. You will not be able to open new positions or close existing positions.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed.

3. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected].

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, both the S&P 500 and Nasdaq Composite closed lower, hovering near their highest closing levels since August 2022. The S&P 500 slipped by 0.38%, settling at 4,267.52, while the Nasdaq Composite declined by 1.29%, ending at 13,104.89. However, the Dow Jones Industrial Average stood out among the major averages, adding 91.74 points or 0.27% and closing at 33,665.02.

Energy emerged as the best-performing sector in the S&P 500, experiencing a rise of approximately 2.6%. Notably, the SPDR S&P Oil & Gas Exploration & Production ETF (XOP) and First Trust Natural Gas ETF (FCG) both gained over 3%. Regional banks also saw continued growth, with the SPDR S&P Regional Banking ETF (KRE) rising more than 3%. PacWest Bancorp’s shares surged by 14.4%, while Zions Bancorporation added 4.5%.

Despite the recent market rally driven by the promise of artificial intelligence and a 7% increase in the S&P 500 over the past three months, Bob Doll, Chief Investment Officer at Crossmark Global Investments, cautioned about the future impact of the Federal Reserve’s interest rate hikes. Doll pointed to ongoing concerns such as leading economic indicators declining for 13 consecutive months, an inverted yield curve, and liquidity issues. He advised caution and urged investors not to get carried away by the current rally.

Meanwhile, the U.S. trade deficit continued to rise in April, although it came in slightly below economists’ expectations. This deficit could potentially lead to lower GDP growth in the second quarter.

On Wednesday, the overall performance of sectors in the market showed a slight decline, with all sectors experiencing a decrease of 0.38%. However, some sectors managed to outperform the market. Energy was the best-performing sector, with a positive price change of 2.65%. Real estate and utilities also had a good day, with gains of 1.75% and 1.70% respectively. Industrials and materials followed suit with increases of 1.59% and 1.18%.

Financials had a modest gain of 0.33%. On the other hand, several sectors faced declines. Consumer staples and healthcare experienced small decreases of 0.33% and 0.41% respectively. Consumer discretionary had a larger decline of 0.91%. The worst performers were information technology and communication services, both with significant decreases of 1.62% and 1.87% respectively.

Major Pair Movement

The US Dollar Index (DXY) is facing downward pressure around 104.00 as the market balances hawkish Federal Reserve expectations with concerns about US economic growth. Despite the strong performance of US Treasury bond yields and the dollar’s safe-haven status, the index fails to reflect these positive factors.

At the same time, the EUR/USD pair is trading within a week-long Pennant formation near 1.0700, with bullish and bearish forces in contention due to fears of an economic slowdown, higher interest rates, and weaker Eurozone data.

In other currency developments, the GBP/USD pair experiences a slight upward movement but remains significantly below the previous day’s weekly peak around the key level of 1.2500. The pair finds support from the subdued performance of the US Dollar.

Similarly, AUD/USD remains low at approximately 0.6650 after retreating from a one-month high, as concerns about the Reserve Bank of Australia’s hawkish stance and worries about economic growth weigh on the Australian dollar.

Additionally, USD/CAD initially dropped to a low of 1.3318 following an unexpected interest rate hike by the Bank of Canada, marking the lowest level since May 8. However, the pair later rebounded to around 1.3400, erasing its losses, due to the overall strength of the US dollar supported by higher US yields.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds Steady Ahead of ECB Meeting and US Economic Indicators

The EUR/USD pair showed a mixed performance as it initially dipped close to weekly lows near 1.0645, surged to 1.0739 – its highest level since Friday – and then retraced back to the 1.0700 range. The pair remained range-bound, eagerly awaiting new catalysts and events scheduled for the following week.

The upcoming European Central Bank (ECB) meeting, where a rate hike is expected, will be a crucial event with new forecasts, shaping market expectations for July. Germany’s reported industrial production increase of 0.3% MoM in April fell short of expectations. On Thursday, a fresh estimate of Q1 Euro area GDP and employment change data will be released.

Meanwhile, the US dollar gained momentum after the Bank of Canada’s rate hike and was further supported by surging US bond yields, with the 10-year yield reaching the highest level since May 29. The focus shifts to upcoming events, including the Federal Reserve’s decision on the Fed Fund rate, as well as potential actions from the Reserve Bank of Australia and the impact of US employment data, particularly the crucial Consumer Price Index report on Tuesday and the weekly jobless claims report on Thursday.

According to technical analysis, theEUR/USD pair moved in flat on Wednesday as we can see that the upper and lower bands is getting narrower. Currently, the EUR/USD is running just above the middle band, with the potential for it to move higher and try to push the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 50, indicating that the EUR/USD is in a neutral trend.

Resistance: 1.0724, 1.0766

Support: 1.0671, 1.0634

XAU/USD (4 Hours)

Gold (XAU/USD)Retreats as US Dollar Regains Strength Amid Speculation of Fed Rate Hike

Gold (XAU/USD) experienced a decline after reaching a peak of $1,970.15 per troy ounce, nearing the $1,940 level. The initial weakness of the US Dollar was reversed during the US session, as rising US government bond yields provided support. The speculation surrounding the US Federal Reserve’s potential decision to raise interest rates by 25 basis points next week favoured the USD, despite still high odds for no change. The Bank of Canada’s surprise rate hike and the Reserve Bank of Australia’s recent move cast doubt on the expected end of the tightening cycle in the US. The mixed trading of US stock indexes reflected the uncertainty surrounding the Fed’s next steps, while the 10-year Treasury note and 2-year note yields rose by 8 and 6 basis points, respectively.

According to technical analysis, the XAU/USD pair is moving higher in the early session on Wednesday but then drop to break our support level in the US session and reach the lower band of the Bollinger Bands. There is a possibility that the XAU/USD will move back higher for today and try to reach the middle band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 41, suggesting that the XAU/USD is in a slight bearish tone.

On Tuesday, the S&P 500 reached its highest close since the beginning of 2023, reflecting a recent rally that propelled the index to its strongest level in nine months. The broad-market index added 0.24% to finish at 4,283.85, marking its highest close since August 2022. Similarly, the Nasdaq Composite also achieved a closing high for 2023, rising 0.36% to end at 13,276.42. Meanwhile, the Dow Jones Industrial Average experienced a slight uptick of 0.03%, or 10.42 points, closing at 33,573.28, hindered by notable losses in Merck and UnitedHealth.

In other market news, Coinbase faced a significant setback as it plummeted over 12% following a lawsuit filed by the Securities and Exchange Commission (SEC) against the cryptocurrency company. The SEC accused Coinbase of operating as an unregistered broker and exchange. On a positive note, Bitcoin saw an increase of more than 6% according to CoinMetrics. Additionally, Apple shares declined by 0.2% the day after the highly anticipated unveiling of their virtual reality headset and new software at the annual Worldwide Developer Conference, despite hitting an all-time high in the previous trading session.

On Tuesday, the overall market experienced a positive price change of 0.24%. Among the sectors, Financials showed the highest increase with 1.33%, followed by Consumer Discretionary at 0.99%. Energy and Real Estate sectors also saw gains, with increases of 0.69% and 0.66% respectively. Materials and Industrials sectors had relatively smaller gains of 0.65% and 0.60% respectively. Communication Services showed a modest increase of 0.49%. On the other hand, Utilities experienced a slight decline of -0.07%. Information Technology and Consumer Staples also showed negative price changes, with decreases of -0.12% and -0.47% respectively. Health Care sector had the largest decrease of -0.88% on Tuesday.

Major Pair Movement

On Tuesday, the US dollar (USD) strengthened due to a lack of significant risk events and a limited news calendar. The US Dollar index had a volatile trading session within a narrow range. The dollar received support from weakness in the euro (EURUSD), while positive growth forecasts for the US by Goldman Sachs and the World Bank further boosted the greenback.

Among the G10 currencies, the euro (EUR) underperformed, causing EURUSD to reach lows of 1.0668 before finding some support at a Fibonacci level. This decline followed a disappointing report on German industrial orders and a consumer survey conducted by the European Central Bank (ECB), which revealed a significant decrease in inflation expectations. Adding to the bearish sentiment were dovish comments from ECB member Knot, known for his hawkish stance, who stated that “the worst of inflation is behind us.” More ECB statements are scheduled for Wednesday, which could reinforce this cautious outlook.

The Australian dollar (AUD) stood out as the top performer among the G10 currencies after the Reserve Bank of Australia (RBA) surprised the market with a 25-basis point rate hike, bringing rates to 4.10%. The RBA’s hawkish statement, indicating the possibility of further rate increases, propelled AUDUSD to a high of 0.6685, just shy of the 200-day moving average at 0.6692. The Australian dollar held most of its gains after the announcement throughout the session.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Drops Amid Cautious Markets as Focus Shifts to Central Bank Meetings

TheEUR/USD experienced a decline while trading around the 1.0700 area, with attention turning to upcoming central bank meetings. The European Central Bank (ECB) is expected to raise interest rates by 25 basis points next week, followed by another potential hike in July. However, economic indicators, such as stagnant retail sales in the Eurozone and a decline in German factory orders, reflect consumer caution. The US Dollar saw modest gains as market participants remained wary ahead of a crucial week, considering a bleak global outlook and the anticipation of higher interest rates. The Federal Reserve’s upcoming FOMC meeting is awaited with caution, as analysts closely monitor the May Consumer Price Index as a determining factor.

According to technical analysis, theEUR/USD pair moved lower on Tuesday, trying to reach the lower band of the Bollinger Bands and moved flat before closing the day. Currently, the EUR/USD is running just below the middle band, with the potential for it to move lower to reach the lower band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 45, indicating that the EUR/USD is in a neutral trend.

Resistance: 1.0724, 1.0766

Support: 1.0671, 1.0634

XAU/USD (4 Hours)

Gold (XAU/USD)Under Pressure as Markets Await Central Bank Decisions and Inflation Data

Gold (XAU/USD) facing slight downward pressure, hovering around $1,960, as financial markets adopt a cautious stance due to discouraging macroeconomic data and upcoming major announcements. Weighing on market sentiment are softer-than-expected figures, alongside anticipation of monetary policy decisions by the US Federal Reserve and the European Central Bank. While the Fed is expected to maintain its current stance, the ECB is likely to implement another rate hike. Additionally, the US will release an update on inflation before the Fed’s decision, with the May Consumer Price Index anticipated to rise by 4.2% YoY. Despite the Fed’s tightening measures, the labour market remains tight, and wage inflation remains a concern. Economic growth has slowed due to monetary tightening, and central banks are striving to strike a delicate balance between maintaining economic activity and curbing inflation. The recent bank crisis in March has prompted policymakers to adopt a cautious approach, but if inflation remains high and the labour market remains tight, the US central bank may resume raising interest rates, leading to uncertainty in the financial markets.

According to technical analysis, the XAU/USD pair is moving higher on Tuesday, reaching above the middle band of the Bollinger Bands. There is a possibility that the XAU/USD will continue to move higher and try to reach the upper band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 54, suggesting that the XAU/USD is in a neutral but slightly bullish trend.