Key Takeaways

- Conflicts involving major oil-producing regions often trigger spikes in global oil and gas prices.

- Historical events such as the 1973 oil embargo and the Gulf War show how quickly geopolitical shocks can move energy markets.

- The Iran–Israel conflict has raised similar concerns because the Middle East remains central to global oil supply.

Fuel prices are closely tied to global geopolitics. When conflicts occur in energy-producing regions, oil markets often react quickly, pushing crude prices higher and eventually raising gas prices for consumers.

This dynamic has played out repeatedly throughout modern history. From the 1973 oil crisis to more recent geopolitical conflicts, wars that threaten oil production or transport routes have often triggered energy price shocks.

Today, concerns about the Iran–Israel conflict and gas prices reflect a familiar pattern. Markets are once again watching developments in the Middle East closely because the region remains a major source of global oil supply.

Understanding how wars affect energy markets can help explain why fuel prices often rise during periods of geopolitical tension.

The 1973 Oil Crisis: The First Global Energy Shock

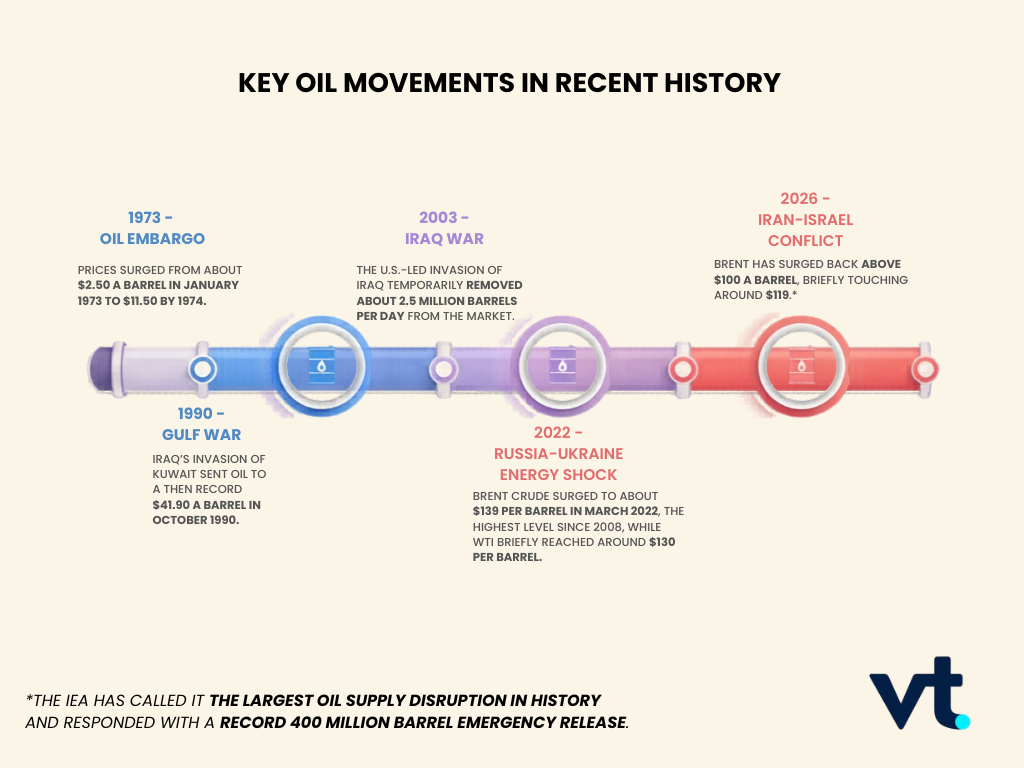

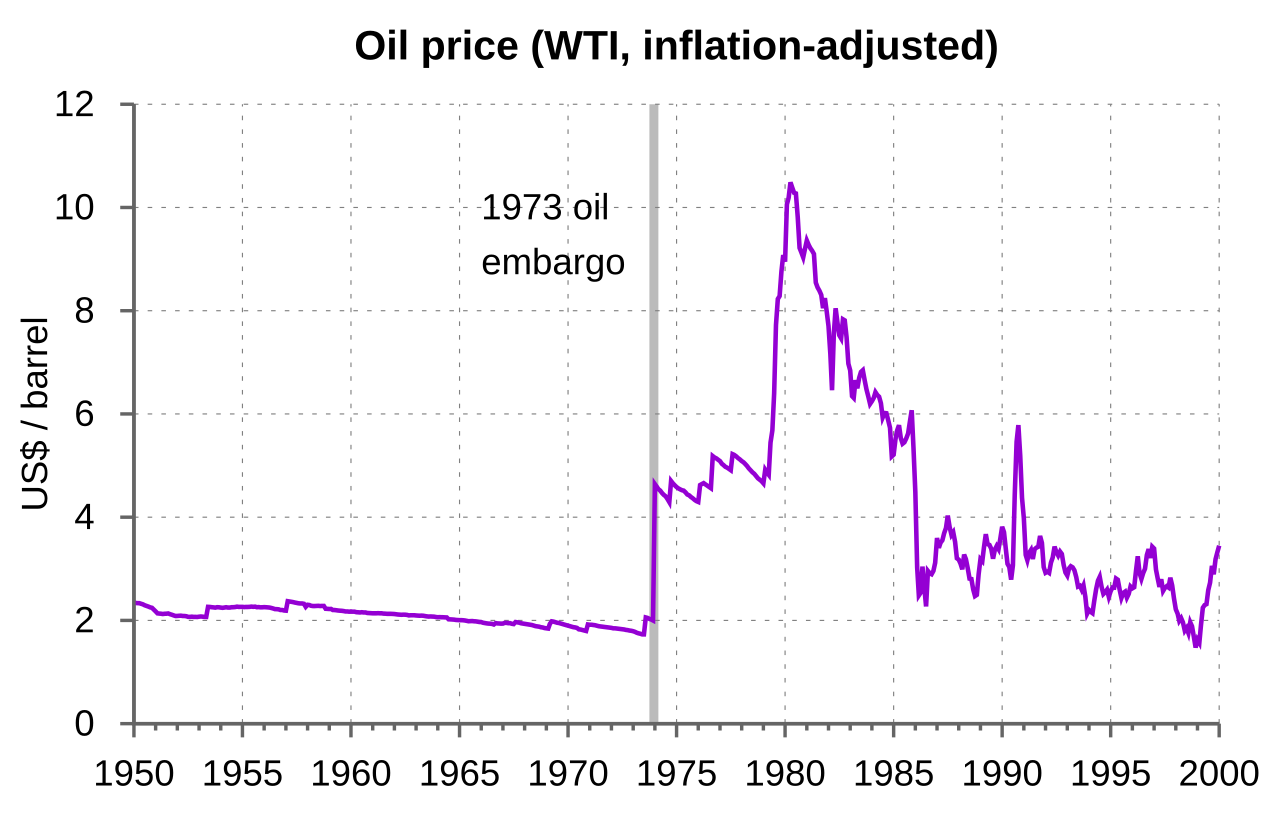

One of the most significant examples of war driving fuel prices higher occurred during the 1973 oil crisis.

Source: Wikipedia

Following the Yom Kippur War between Israel and several Arab states, members of the Organization of Petroleum Exporting Countries (OPEC) introduced an oil embargo against nations that supported Israel.

The consequences were immediate.

Oil prices quadrupled within months, fuel shortages spread across Western economies, and long lines formed at petrol stations. The surge in energy costs contributed to inflation, economic slowdown, and lasting changes in global energy policy.

The crisis demonstrated how geopolitical tensions in the Middle East could rapidly destabilise energy markets and push gas prices higher worldwide.

The Gulf War and Oil Market Volatility

Another major example occurred during the 1990 Gulf War, when Iraq invaded Kuwait.

At the time, both countries were major oil producers. The invasion raised fears that oil production across the region could be disrupted.

Source: The Guardian

As uncertainty spread through energy markets, oil prices surged sharply within weeks. Traders anticipated potential supply shortages and began pricing in geopolitical risk.

Although production eventually stabilised after international intervention, the episode reinforced an important lesson for energy markets. Even the threat of conflict in major oil-producing regions can drive significant price volatility.

The Russia–Ukraine War and the Modern Energy Shock

More recently, the Russia–Ukraine war triggered another major energy price surge.

Russia is one of the world’s largest producers of oil and natural gas. When the conflict began in 2022, global energy markets reacted quickly to fears of supply disruptions and sanctions targeting Russian exports.

Oil prices climbed sharply and natural gas prices surged across Europe. Fuel costs rose worldwide, contributing to inflation and forcing governments and central banks to respond to rising energy bills.

The crisis demonstrated once again how closely global fuel prices are linked to geopolitical stability.

Why the Iran–Israel Conflict Matters for Oil Markets

The current Iran–Israel conflict has renewed concerns about gas prices because of the Middle East’s critical role in global energy supply.

Several factors make the region particularly important for oil markets.

Strategic shipping routes

One of the most important is the Strait of Hormuz, a narrow passage between Iran and Oman. Roughly one-fifth of the world’s oil shipments pass through this route each day.

Any disruption to shipping traffic in the Strait of Hormuz could affect global oil supply and push crude prices higher.

Regional oil production

The Middle East remains one of the largest oil-producing regions in the world. Countries across the Gulf export millions of barrels of oil each day to global markets.

Escalating conflict in the region raises the risk that production or transport infrastructure could be disrupted.

Market psychology

Energy traders often react to geopolitical risks before supply disruptions actually occur. Even the possibility of escalation can cause oil prices to move higher as markets attempt to price in uncertainty.

This is why news about the Iran–Israel war and gas prices often appear together in financial headlines.

Why Oil Prices Affect Gas Prices

Crude oil typically represents the largest component of the price consumers pay at the pump.

When oil prices rise because of geopolitical tensions, refiners pay more for raw crude. Those costs move through the supply chain, eventually raising petrol and diesel prices for drivers.

As a result, global conflicts that push oil prices higher often lead to higher gas prices as well.

Oil movements have more than just an influence on gas prices. Read more about how oil prices play a role in the AI revolution here.

What History Suggests About Future Gas Prices

History shows that geopolitical conflicts often trigger temporary spikes in oil prices and fuel costs.

However, the long-term impact can vary depending on several factors:

- Whether oil supply is actually disrupted

- How long the conflict lasts

- How quickly producers adjust output to stabilise markets

In many cases, prices stabilise once markets gain confidence that supply will remain stable. In other situations, prolonged tensions can keep energy markets volatile for extended periods.

Because the global economy depends heavily on oil, geopolitical developments will likely continue to influence fuel prices for years to come.

The Bottom Line

From the 1973 oil embargo to the Russia–Ukraine war, history shows that geopolitical conflicts often lead to spikes in oil and gas prices.

The Iran–Israel conflict has raised similar concerns because of the Middle East’s central role in global energy supply and the importance of shipping routes such as the Strait of Hormuz.

While the long-term impact on gas prices will depend on how events unfold, one lesson from history remains clear. When conflict threatens global energy supply, oil markets react quickly, and fuel prices often follow.

For more market commentary, explore the latest Analysts’ report on VT Markets.

Refresher

- Why does the Iran–Israel war affect gas prices?

The Iran–Israel war affects gas prices because conflicts in the Middle East can disrupt global oil supply and shipping routes. When traders fear supply shortages, crude oil prices often rise, which can then push petrol and diesel prices higher. - Does war always make gas prices go up?

War does not always lead to higher gas prices, but it often does when the conflict involves major oil-producing regions or key transport routes. Markets tend to react quickly to supply risks, even before actual disruptions happen. - Why do Middle East conflicts affect fuel prices worldwide?

Middle East conflicts affect fuel prices worldwide because the region plays a major role in global oil production and export flows. Important routes such as the Strait of Hormuz handle a large share of global oil shipments, so any threat to supply can raise prices internationally. - How quickly do oil price spikes affect petrol prices?

Oil price spikes can affect petrol prices within days or weeks, depending on the country and the fuel supply chain. The final impact depends on refining costs, transport costs, taxes, and how quickly retailers adjust pump prices. - Have wars caused major fuel price spikes before?

Yes. Historical examples include the 1973 oil crisis, the 1990 Gulf War, and the 2022 Russia–Ukraine war. In each case, geopolitical conflict created supply fears that pushed oil and fuel prices higher. - What is the connection between oil prices and gas prices?

Oil prices are a major component of gas prices because crude oil is refined into petrol and diesel. When crude oil becomes more expensive, the cost of producing fuel usually rises as well, which can lead to higher prices at the pump. - Could gas prices fall even if the conflict continues?

Yes. Gas prices can fall if markets believe supply will remain stable, if oil producers increase output, or if demand weakens. Fuel prices depend on market expectations as much as on the conflict itself. - Why do traders watch the Strait of Hormuz so closely?

Traders watch the Strait of Hormuz because it is one of the world’s most important oil shipping routes. Any disruption there can slow global energy flows and quickly push oil prices higher.

Start trading now – Click here to create your real VT Markets account