Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, the stock market witnessed a downturn triggered by the Federal Reserve’s decision to maintain interest rates while signaling a looming rate hike. The S&P 500 and Nasdaq Composite both declined, with tech giants such as Microsoft, Nvidia, and Alphabet experiencing significant drops. The Federal Reserve’s cautious approach to rate hikes due to inflation concerns sent shockwaves through the markets, particularly impacting tech stocks that had been performing well earlier in the year. The increase in Treasury yields also raised concerns about the tech sector’s vulnerability to higher rates. Meanwhile, the US dollar had mixed movements in the currency market as the Fed’s hawkish stance influenced market sentiment but concerns about limited rate hike potential limited further gains.

Stock Market Updates

On Wednesday, the stock market experienced a decline in response to the Federal Reserve’s announcement of leaving interest rates unchanged but hinting at an impending rate hike. The S&P 500 dropped by 0.94% to 4,402.20, while the Nasdaq Composite slid by 1.53% to 13,469.13. This decline was primarily driven by significant drops in tech giants like Microsoft, which saw a drop of over 2%, and Nvidia and Google-parent Alphabet, which both experienced declines of around 3%. The Dow Jones Industrial Average also lost 76.85 points, or 0.22%, closing at 34,440.88, with all three major indexes ending the day at session lows.

The Federal Reserve’s decision to keep interest rates steady, while expected, raised concerns among investors as the central bank indicated that one more rate hike is likely before the end of the year. The Fed’s economic projections suggested that after this increase, they would begin cutting rates next year, although rates would remain higher than previously signaled in June. Fed Chair Powell emphasized the need to proceed cautiously in raising rates further due to ongoing concerns about inflation. This news sent shockwaves through the markets, particularly impacting tech stocks, which had been performing well earlier in the year based on the expectation of a less aggressive monetary policy. Additionally, the increase in Treasury yields, with the 2-year yield reaching levels not seen since July 2006 and the 10-year yield hitting a high not seen since November 2007, raised concerns about the potential adverse effects of higher rates on the tech sector.

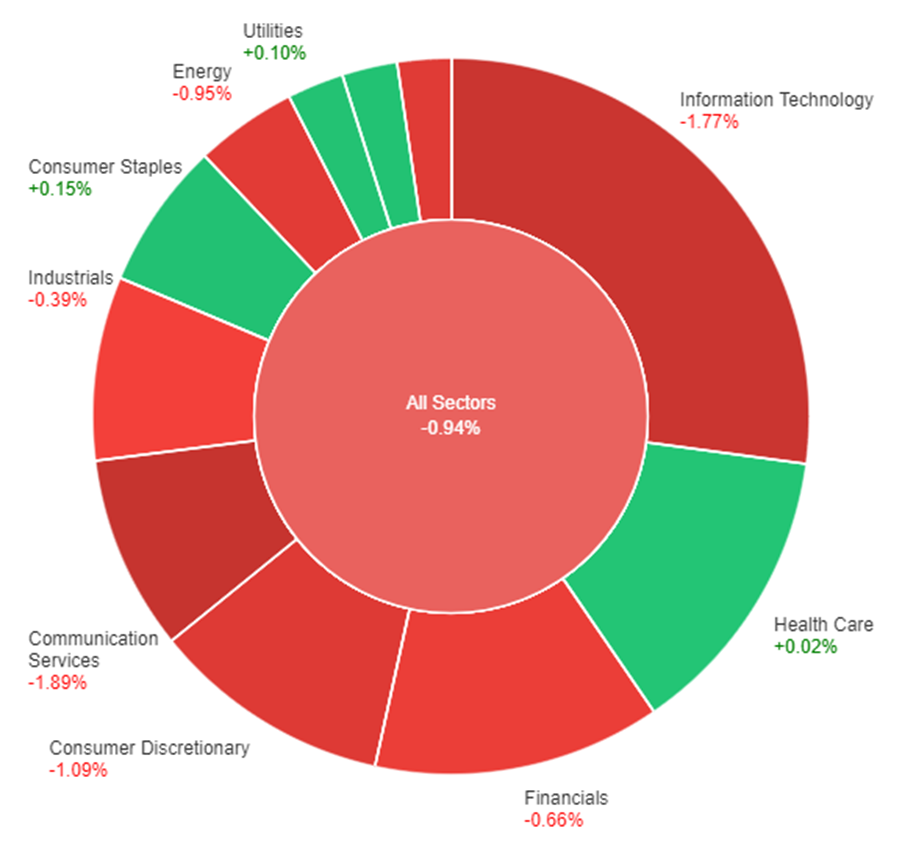

On Wednesday, across all sectors, the market experienced a decrease of 0.94%. Some sectors showed modest gains, with Consumer Staples up by 0.15%, Real Estate by 0.13%, Utilities by 0.10%, and Health Care by 0.02%. However, several sectors saw declines, including Industrials (-0.39%), Financials (-0.66%), Energy (-0.95%), Materials (-1.03%), Consumer Discretionary (-1.09%), Information Technology (-1.77%), and Communication Services (-1.89%).

Currency Market Updates

In the latest currency market update, the US dollar experienced a day of mixed movements. Initially facing losses, the dollar index managed to stabilize as the Federal Reserve’s hawkish stance boosted market confidence. However, its ability to advance further was limited due to market consensus that there is limited room for the US central bank to raise rate expectations. The Fed’s dot plots indicated a preference for one more rate hike in the current year, reducing the median projection for rate cuts in 2024 from 100 basis points to 50 basis points. Federal Reserve Chair Jerome Powell emphasized the data-dependent nature of their decisions, noting that policy is already restrictive, and the full impact of previous tightening measures has yet to be felt. This announcement led to a sharp decline in the EUR/USD pair as 2-year Treasury yields rebounded to new highs for 2023.

Despite these developments, the dollar index is still grappling with overbought pressures that have arisen from its 6% increase since July. GBP/USD also saw fluctuations, initially dropping following below-forecast CPI data but rebounding ahead of the Federal Reserve’s announcement. To reverse the downtrend, GBP/USD would need to close above the 200-day moving average at 1.2434. Meanwhile, USD/JPY held relatively steady after the Fed events and briefly exceeded the 148 hurdle earlier in the day. The focus now turns to upcoming U.S. data releases and the Bank of Japan’s policy decisions, with potential tension between U.S. and Japanese officials regarding the timing of Japanese FX intervention. Overall, high-beta currencies like the Australian dollar retreated from their pre-Fed risk-on gains, stemming from expectations that major central banks’ tightening cycles are reaching their peaks.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Falls as FOMC Meeting Spurs Stronger US Dollar, Fed Signals Hawkish Stance

The EUR/USD experienced a significant decline, dropping from its weekly highs above 1.0730 to 1.0650 in response to the FOMC meeting’s outcome. The Federal Reserve unanimously maintained its interest rate target range at 5.25-5.50%, with minimal changes in the statement compared to the previous month. The Summary of Economic Projections suggests the likelihood of another rate hike by year-end, although Fed Chair Powell emphasized that the dot plot is not a firm plan. The market perceived the meeting as hawkish, causing US bond yields to surge to multi-year highs and Wall Street to turn bearish, subsequently strengthening the US Dollar. Upcoming US data releases and decisions from central banks like the Swiss National Bank and the Bank of England will remain pivotal for market dynamics.

According to technical analysis, the EUR/USD moved in high volatility on Wednesday and able to reach the upper band but then moves back lower and reach the lower band of the Bollinger Bands. This movement suggests the possibility of further consolidation. The Relative Strength Index (RSI) is currently at 39, indicating that the EUR/USD is in a neutral stance with a slight bearish bias.

Gold prices fell for the third consecutive day, trading around $1,925 during Asia’s early trading hours on Thursday. The US Federal Reserve (The Fed) kept its benchmark interest rate at 5.5%, but projected more rate hikes in 2023, leading to pressure on precious metals. The Fed’s revision of 2024 interest rate projections, from 4.6% to 5.1%, unexpectedly boosted the US Dollar, causing the US Dollar Index (DXY) to reach a six-month high at 105.60. US bond yields also rose, with the 10-year bond hitting 4.43%, its highest since 2007. Precious metals slipped after Fed Chair Jerome Powell’s press conference, where he reiterated The Fed’s commitment to a 2% inflation target and emphasized data-driven future decisions. More US data, including Weekly Jobless Claims, the Philadelphia Fed Manufacturing Survey, and Existing Home Sales Changes, will impact markets on Thursday.

According to technical analysis, XAU/USD moved in high volatility on Wednesday and able to reach the upper band then moving back lower. Currently, the price is trading between the middle and lower bands. The Relative Strength Index (RSI) is currently at 48, indicating that the XAU/USD pair is back in neutral stance.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Tuesday, the stock market experienced a decline as investors awaited the Federal Reserve’s policy meeting outcomes later in the week, resulting in the Dow Jones Industrial Average falling by 0.31%, the S&P 500 slipping by 0.22%, and the Nasdaq Composite dropping by 0.23%. Disney and Deere faced setbacks due to investment plans and downgrades, respectively, while Instacart stood out with a gain of over 12% after going public. The Federal Reserve’s two-day meeting garnered significant attention, with a 99% probability of no interest rate hike, but investors were keen on economic forecasts, oil prices settled lower, and the U.S. Treasury yield reached its highest level in years. In the currency market, the US dollar remained stable, and the euro to US dollar pair faced resistance, while the USD/JPY rose, and the British pound saw a modest increase. The Australian and Canadian dollars both gained, with additional support from energy prices, and the New Zealand dollar rose to its highest level in five days.

Stock Market Updates

On Tuesday, the stock market saw a retreat as investors anxiously awaited the outcomes of the Federal Reserve’s policy meeting scheduled for later in the week. The Dow Jones Industrial Average declined by 106.57 points, or 0.31%, closing at 34,517.73, while the S&P 500 slipped 0.22% to 4,443.95, and the Nasdaq Composite fell 0.23% to 13,678.19. Disney faced a significant setback, plummeting more than 3% following its announcement of plans to nearly double its investment in its cruise and parks business. Deere, often considered an economic activity indicator, also suffered a 3% drop after being downgraded by investment bank Evercore ISI due to concerns about agricultural production. However, grocery delivery company Instacart stood out with a gain of over 12% after going public.

The Federal Reserve’s two-day meeting, commencing on Tuesday, was the focal point for investors. While it was widely expected that the Fed would not raise interest rates in its Wednesday announcement, traders priced in a 99% probability of no hike, according to CME Group’s FedWatch tool. Only a 29% chance of a rate hike in November was anticipated. Investors are eagerly awaiting the Fed’s economic forecasts, especially regarding inflation and future monetary policy. Additionally, oil prices settled lower after reaching highs not seen since November, which seemed to boost market sentiment and lift stocks off their lows. Meanwhile, the 10-year U.S. Treasury yield hit its highest level since November 2007. In other news, the United Auto Workers union’s leadership warned of the potential for more members to strike if progress isn’t made by a Friday deadline. As a result, Stellantis saw an increase of more than 2% in its stock price, while Ford and General Motors each added more than 1%.

On Tuesday, across all sectors, the overall market experienced a slight decline of 0.22%. Among the sectors, Health Care showed a modest gain of 0.10%, while Communication Services and Information Technology both saw marginal increases of 0.01% and -0.08% respectively. The Materials and Financials sectors decreased by 0.10% and -0.11%, while Consumer Staples experienced a more significant decline of 0.25%. Industrials and Utilities both had substantial drops of 0.46% and 0.55% respectively. Real Estate and Consumer Discretionary sectors also saw notable decreases of 0.56% and 0.65%, while Energy had the most significant decline of 0.83%.

Currency Market Updates

In the currency market, the US dollar index remained relatively stable, showing slight upward movement after earlier declines in anticipation of important events from the Federal Reserve (Fed). Investors were closely watching the possibility of the Fed providing guidance suggesting another interest rate hike later in the year. This cautious sentiment was impacting expectations for any potential interest rate cuts before the second half of 2024. The dollar index had retreated from its recent six-month highs, encountering significant resistance, as it aimed to consolidate gains made since hitting lows in July. The euro to US dollar (EUR/USD) pair was in focus, with EUR/USD having recovered from last week’s probe of the major swing low at 1.0635 but facing resistance at 1.0718. The market’s attention was shifting towards the Fed, with the expectation that it might adopt a more hawkish stance compared to the European Central Bank (ECB), which had recently raised rates, citing that they were now restrictive enough to curb euro zone inflation.

In the USD/JPY pair, the US dollar rose by 0.17%, primarily driven by a rise in Treasury yields. Two-year yields were nearing their highest level since 2006, just below the peak seen in July at 5.12%, while ten-year yields were reaching levels not seen since 2007. This development led to a narrowing of Treasury-JGB yield spreads, potentially paving the way for a breakout in USD/JPY, assuming a hawkish stance from the Fed and the Bank of Japan’s expected policy normalization delay. Meanwhile, the British pound (GBP) saw a 0.06% increase, although it retreated from intraday highs due to the US dollar’s broader rebound. Concerns were rising that the Bank of England’s anticipated rate hike on Thursday might be its last, despite persistently high UK overall and core inflation rates at 6.8% and 6.9%, respectively. In the coming days, the currency market will closely monitor CPI releases, which are forecasted to show overall and core inflation rates at 7.0% and 6.8%. Finally, the Australian and Canadian dollars both gained 0.3%, with the latter receiving additional support from above-forecast data. Both currencies benefited from the recent surge in energy prices and signs of stabilization in China’s economy, while the New Zealand dollar rose by 0.15% to its highest level in five days, though it faced challenges in breaking above the 10-day moving average.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Sees Modest Decline as US Dollar Strengthens Ahead of FOMC Decision

The EUR/USD pair experienced a slight decline, falling from its peak above 1.0700 as the US Dollar gained strength due to deteriorating market sentiment and higher US yields in anticipation of the Federal Reserve’s (Fed) decision. The Eurozone Harmonized Index of Consumer Price Index showed a minor revision in annual rates, while economic data from Germany and the UK were on the horizon. However, all eyes were on the forthcoming FOMC decision, with expectations of a steady Fed Fund rate and a potential warning regarding the need for further tightening if inflation persists. The market’s direction, especially that of the US Dollar Index (DXY), hinged on the outcome of the meeting, leading to cautious anticipation among market participants.

According to technical analysis, the EUR/USD moved flat on Tuesday and is currently trading just above the middle band of the Bollinger Bands. This movement suggests the possibility of further consolidation. The Relative Strength Index (RSI) is currently at 49, indicating that the EUR/USD is in a neutral stance. (Note: the markets are waiting for today’s Fed rate decision which will create high volatility movement).

Resistance: 1.0711, 1.0759

Support: 1.0653, 1.0605

XAU/USD (4 Hours)

XAU/USD Stall as USD Gains Momentum Amid Inflation Concerns and Fed Speculation

On Tuesday, gold prices showed minimal movement, hovering around the $1,930 mark for XAU/USD. The US Dollar initially faced market disfavor but saw increased demand ahead of Wall Street’s opening and after the release of the Canadian Consumer Price Index (CPI), which indicated a higher-than-expected 4% YoY inflation rate for August. This global inflationary trend, coupled with surging US government bond yields, particularly the 10-year Treasury note reaching levels not seen since 2007 at 4.36%, bolstered the Greenback’s position. While the Federal Reserve’s forthcoming monetary policy announcement is widely expected to maintain the status quo, concerns loom, and Chair Jerome Powell’s words will be closely scrutinized for hints about future rate changes. Wednesday’s release of new economic projections by the Fed is expected to have a more significant impact on the market than the decision itself.

According to technical analysis, XAU/USD moved in a tight range on Tuesday and moved between the middle and upper bands of the Bollinger Bands. Currently, the price is trading slightly above the middle band with the potential for further higher movement. The Relative Strength Index (RSI) is currently at 57, indicating that the XAU/USD pair is in a neutral stance with a bullish bias. (Note: the markets are waiting for today’s Fed rate decision which will create high volatility movement).

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Monday, the stock market showed subdued performance ahead of the Federal Reserve meeting later in the week. The S&P 500 inched up by 0.07%, the Nasdaq rose by 0.01%, and the Dow Jones gained 0.02%. Investors overwhelmingly expected the Fed to maintain its current policy, but uncertainty loomed about November’s actions, with a 31% chance of a rate hike. Apple’s stock surged by 1.7% on positive outlooks, while Ford, Stellantis, and General Motors faced declines due to ongoing union disputes. The US dollar dipped by 0.2% in anticipation of central bank meetings, and EUR/USD rose by 0.24%. USD/JPY struggled to breach resistance, and Sterling hovered below the 200-DMA. USD/CAD dropped by 0.23%, while AUD/USD and USD/CNH made modest gains. The market awaited crucial data and central bank decisions throughout the week.

Stock Market Updates

In the stock market, Monday saw a relatively flat performance as investors eagerly anticipated the upcoming Federal Reserve meeting later in the week. The S&P 500 made a modest 0.07% gain, closing at 4,453.53, while the Nasdaq Composite edged up by 0.01% to finish at 13,710.24. The Dow Jones Industrial Average also advanced by a slight 0.02%, closing at 34,624.30. Traders are overwhelmingly expecting the Federal Reserve to maintain its current policy during its two-day meeting, with a 99% probability of no change in interest rates, according to the CME Group’s FedWatch tool. However, the market remains uncertain about the Fed’s actions in November, with roughly a 31% chance of a rate hike. Investors are keen to decipher the central bank’s future guidance and messaging for potential insights into its next moves.

In company-specific news, Apple saw a 1.7% increase in its stock price, buoyed by optimistic outlooks from Goldman Sachs and Morgan Stanley regarding new iPhone demand. Conversely, Ford’s stock slid by over 2% as the United Auto Workers’ strike persisted, while Stellantis and General Motors, also embroiled in disputes with the union, saw their stocks decline by over 1%. The previous trading week ended with the S&P 500 and Nasdaq posting losses for the second consecutive week, while the Dow managed a slight 0.1% gain, setting the stage for a week of anticipation and cautious observation as market participants await the Federal Reserve’s decisions and guidance.

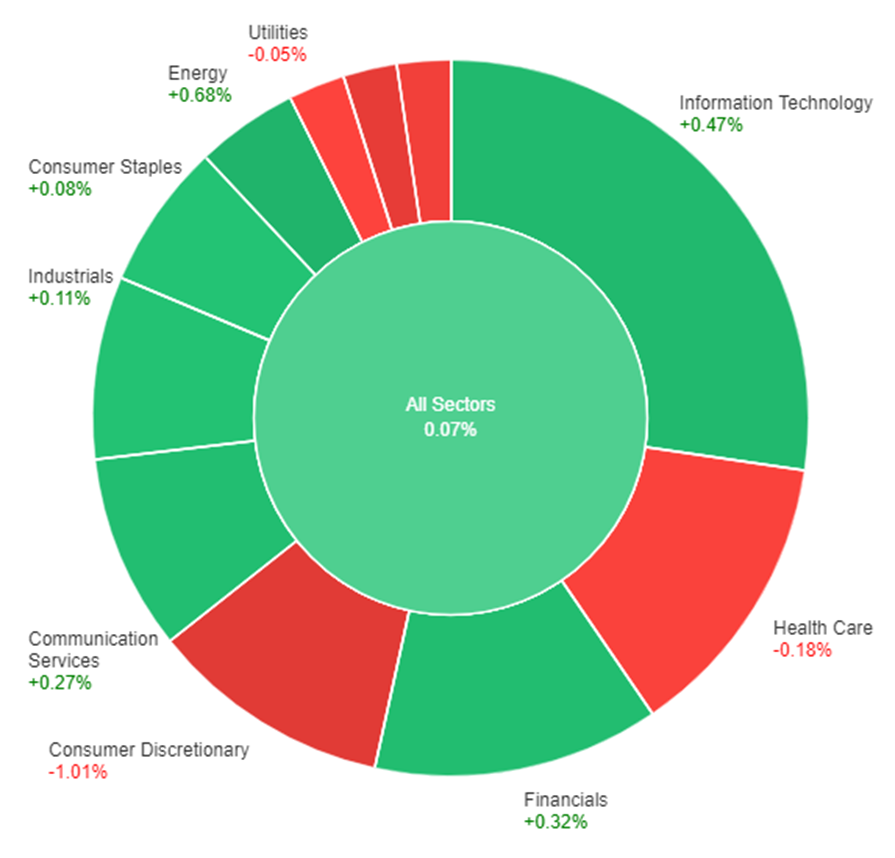

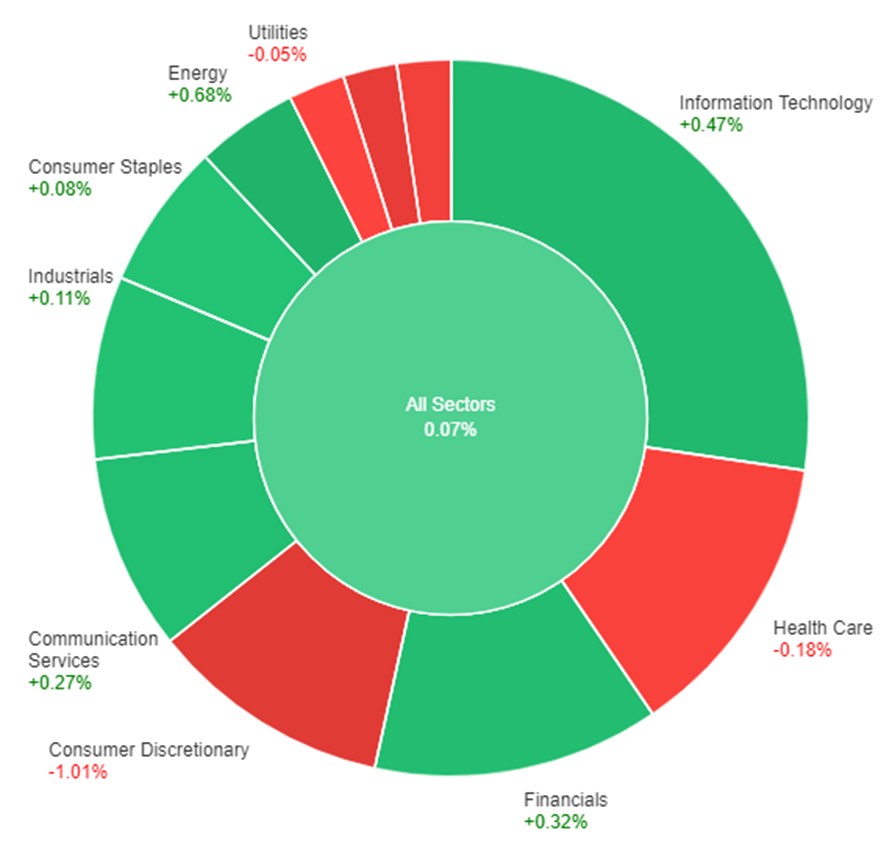

On Monday, across all sectors, there was a slight increase of 0.07% in the market. The sectors that saw gains were led by Energy, with a 0.68% increase, followed by Information Technology at 0.47%, Financials at 0.32%, and Communication Services at 0.27%. However, there were declines in other sectors, with the largest decreases occurring in Consumer Discretionary, which dropped by 1.01%, and Real Estate, which saw a decline of 0.81%. Other sectors that saw declines were Materials at -0.43%, Health Care at -0.18%, and Utilities at -0.05%. Industrials and Consumer Staples had smaller gains of 0.11% and 0.08%, respectively.

Currency Market Updates

In the midst of various global economic factors, the US dollar faced a 0.2% decline on Monday as it encountered significant resistance and EUR/USD found support. This decline occurred in anticipation of upcoming meetings by central banks, including the Fed, BoE, and BoJ. The day saw limited US economic data, with only the NAHB housing market index showing an unexpected downturn. Investors remained vigilant, considering the potential risks posed by the UAW strike and the looming threat of a US government shutdown.

EUR/USD experienced a rise of 0.24%, with factors such as opposition from ECB hawks to rate cut expectations and disappointing Michigan sentiment data lending support. Furthermore, the bond yields in the eurozone outpaced Treasury yields, and Brent crude oil prices approached triple-digit figures. Despite these dynamics, USD/JPY faced a 0.1% decline, failing to breach the 148 hurdle that had been impeding its upward trend for an extended period. The forthcoming Fed meeting was expected to influence the market’s perception of future rate hikes and Treasury yields, potentially opening room for USD/JPY to rise towards resistance around 150 before any substantial correction.

Meanwhile, Sterling remained stable but below the 200-day moving average (200-DMA), which it had broken and closed below in the previous week. Market expectations indicated an 81% probability of a BoE rate hike on Thursday, although Sterling’s performance could be influenced by perceptions of the likelihood of a follow-on rate increase. In addition, USD/CAD experienced a 0.23% drop, breaking below September’s lows, initially bolstered by rising oil prices, but subsequently facing a setback as WTI oil prices retreated below $90 later in the day. Canadian CPI data was awaited on Tuesday, potentially influencing the trajectory of USD/CAD. Meanwhile, AUD/USD and USD/CNH both recorded modest gains of 0.06% and 0.14%, respectively.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Fluctuates Amidst Central Bank Moves and Growth Outlook Uncertainty

The EUR/USD saw an initial rise to near 1.0700 on Monday, driven by a US Dollar correction in a calm session. Despite the European Central Bank’s expected 25 basis point rate hike last Thursday, the Euro weakened but found support at 1.0630, subsequently recovering. Market sentiment suggests no further ECB rate increases, shifting the focus to rate duration. Likewise, the Federal Reserve’s upcoming FOMC meeting anticipates no rate changes, focusing on statements, projections, and Chair Powell’s remarks. Current fundamentals favor the US Dollar due to a stronger US growth outlook. This week’s data, including preliminary PMIs and CPI readings, will offer insights into differing growth prospects between Europe and the US.

According to technical analysis, EUR/USD moved slightly higher on Monday and is currently trading just around the middle band of the Bollinger Bands. This movement suggests the possibility of further consolidation. The Relative Strength Index (RSI) is currently at 47, indicating that EUR/USD is in a neutral stance.

Resistance: 1.0711, 1.0759

Support: 1.0653, 1.0605

XAU/USD (4 Hours)

XAU/USD Starts the Week with Optimism Amidst Economic Uncertainty

XAU/USD started the week on a positive note, trading near the upper end of Friday’s range, while market focus remains on stocks and government bond yields due to a lack of significant news. The demand for the US Dollar is subdued as stock markets grapple with tepid earnings reports, particularly in the tech sector. European indexes saw modest losses, but Wall Street rebounded from last week’s slump. US Treasury yields continue to rise due to inflation concerns ahead of the Federal Reserve’s monetary policy meeting this Wednesday. Currently, the 10-year note yields 4.33%, while the 2-year note offers 5.06%. Speculators anticipate the Fed will keep rates unchanged this week, though caution prevails as market players hope for hints regarding future interest rate moves.

According to technical analysis, XAU/USD moved higher on Monday and was able to create a higher push to the upper band of the Bollinger Bands. Currently, the price is trading slightly below the upper band with the potential for further higher movement. The Relative Strength Index (RSI) is currently at 65, indicating that the XAU/USD pair is now entering the bullish bias.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

This week, traders are mainly focused on the rate decisions of major central banks, such as the Federal Reserve, Swiss National Bank (SNB), Bank of England (BOE), and Bank of Japan (BOJ). These decisions have the potential to influence the markets significantly. It’s advisable to exercise caution and stay informed about the latest developments to ensure a successful week of trading.

Here are some notable market highlights for this week:

Canada Consumer Price Index (19 September 2023)

Consumer prices in Canada rose 0.6% in July 2023, following a 0.1% gain in June 2023.

Analysts expect a 0.6% increase in the figures for August, which are set to be released on 19 September.

Federal Reserve Rate Decision (21 September 2023)

The Fed raised its funds rate target to 5.5% in July.

Analysts expect the Fed to keep interest rates at 5.5% following its upcoming meeting on 21 September.

Swiss National Bank Rate Decision (21 September 2023)

The SNB raised its policy interest rate by 25 bps to 1.75% during its June meeting. It also raised the possibility of further rate hikes in the future to ensure price stability over the medium term.

The next rate decision will be released on 21 September, with analysts expecting another increase of 25 bps to 2%.

Bank of England Rate Decision (21 September 2023)

The BOE raised its policy interest rate by 25 bps to 5.25% during its August 2023 meeting, marking the 14th consecutive increase.

Analysts expect the central bank to raise its rate by another 25 bps to 5.5% at its upcoming meeting on 21 September.

Bank of Japan Rate Decision (22 September 2023)

The BOJ unanimously decided to keep its key short-term interest rate at -0.1% and 10-year bond yields at 0% during its July 2023 meeting.

For the upcoming meeting on 22 September, analysts anticipate that the central bank will maintain the current interest rate levels.

Flash manufacturing PMI for Germany, the UK, and the US (22 September 2023)

Germany’s manufacturing PMI increased to 39.1 in August 2023 from 38.8 in July 2023. Meanwhile, the UK’s manufacturing PMI for the same period fell from 45.3 to 43. Additionally, the US’ manufacturing PMI for the same period decreased from 49 to 47.9

The next set of data will be released on 22 September. Analysts’ predicted manufacturing PMIs are 39 for Germany, 43.6 for the UK, and 48.8 for the US.

Flash services PMI for Germany, the UK, and the US (22 September 2023)

Germany’s services PMI declined from 52.3 in July 2023 to 47.3 in August 2023. Similarly, the UK’s services PMI declined from 51.5 to 49.5 during this period, while the US’ services PMI also fell from 52.3 to 50.2 during the same period.

Analysts’ predicted services PMIs for September 2023 are as follows: Germany at 47.2, the UK at 49.1, and the US at 50.2.

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

16th of September 2023 (Saturday) 08:00 – 13:00 (GMT+3)

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed.

3. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

4. Please note that client might experience order rejections on MT5 and unable to login their MT4/MT5 during the maintenance period.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].