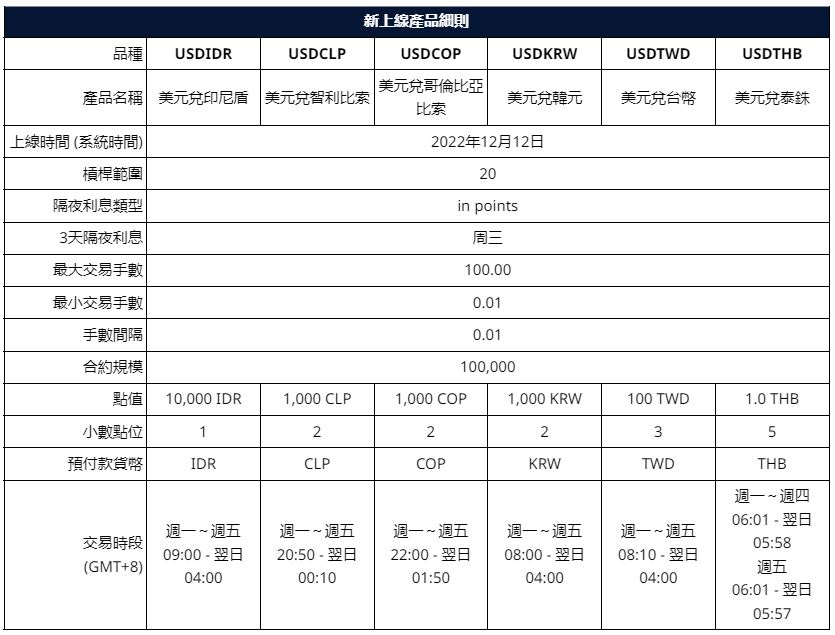

Diversification is key to building a strong trading portfolio. At VT Markets, it’s our mission to help you achieve that by providing multi-asset classes on our robust trading platforms.

Starting on 12 December 2022, we are adding 6 new symbols on MetaTrader 4, MetaTrader 5 and the VT Markets App:

The above data is for reference only, please refer to the trading platforms for the updated data.

To improve your trading experience, we are optimizing the specifications of USOUSD (WTI Crude Oil Cash) on 8 December 2022 (Thursday).

Please note that:

1. During the optimization period, if you are holding a position in USOUSD, a debit or credit adjustment will be made to your account to reflect the price difference before and after the optimization.

2. In the event of a cash adjustment, a record labelled “Cash Adjustment-Rollover – USOUSD” will be reflected in your account history.

3. This optimization is only applicable to USOUSD. The corresponding futures contract for USOUSDft will not be affected.

4. Your take-profit and stop-loss settings will not be automatically updated. Please adjust them accordingly.

5. All open positions will continue to be held. If you do not wish for your position to be affected by this optimization, you are recommended to close your position accordingly.

Rest assured that you will not experience any losses due to this update.

The equities market kicked off the week with losses and bond yields climbed as a US services gauge unexpectedly rose, fueling speculation the Federal Reserve will keep its policy tight to tame stubborn inflation. In the meantime, treasuries slumped across the curve, driving 10-year yields to 3.6%. Swaps showed higher expectations on where the Fed terminal rate will be, with the market indicating a peak above 5% in the middle of 2023.

A majority of 291 respondents to the latest MLIV Pulse survey said leveraged loans would be the canary in the coal mine to indicate that corporate credit quality is getting worse. About 28% of survey respondents expect defaults to jump significantly if US rates peak at or below 5%. Now, market participants are also anxiously awaiting Friday’s report on US producer prices – one of the final pieces of data Fed officials will see before their Dec.13-14 policy meeting. Inflation numbers over the past month have indicated pressures are slowly cooling, but remain very elevated.

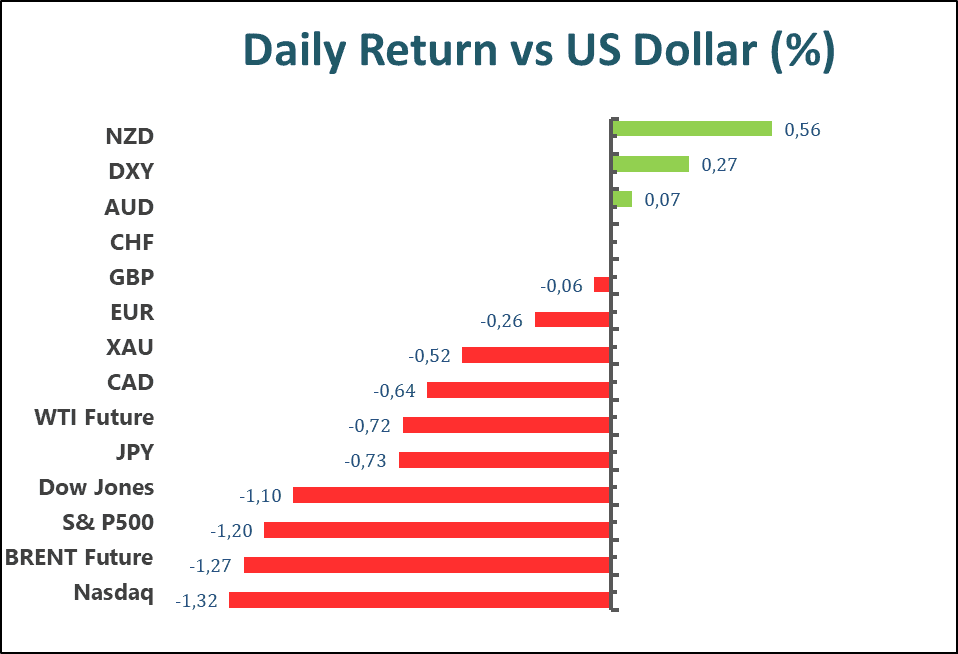

The benchmark, the sell spread throughout all major S&P 500 sectors, with about 95% of the gauge’s companies in the red. The S&P 500 tumbled by 1.79% daily, as all eleven sectors stayed in the negative territory. Especially since the Consumer Discretion sector was performing the worst among all groups, falling 2.95% for the day. Meanwhile, the Nasdaq 100 fell by 1.7%, Dow Jones Industrial Average declined by 1.4%, and the MSCI World index dropped by 1.2% on Monday.

Main Pairs Movement

The US dollar bounced back on Monday after the release of the ISM Services PMI, rising to 56.5 in November from 54.4 in October, which is higher than the market expectation of 53.1, also with the robust Nonfarm Payrolls report, the US Dollar gathered strength against its rivals with the initial reaction and the US Dollar Index rised 0.71% on the day at 105.292 .

US Dollar dropped to over a five-month low at $104.113, the higher-than-expected index may lose the pressure of aggressive policy tightening by the US central bank and release the downward pressure on the greenback. Besides, China’s easing Covid restrictions slow the buying pressure, the EURUSD has dropped lower than 1.05084, and the EUR/USD path of least resistance is downward biased. Therefore, the EUR/USD first support would be the November 22 daily low of 1.022.

The gold price break fell below the cushion of $1,770.0 after surrendering the $1,780.0 support on Monday, the market mood goes soured after the release of the stronger-than-projected US ISM Services PMI data, which triggered a sell-off in the risk-perceived currencies, besides, the upbeat US Nonfarm Payrolls (NFP) data released last week cleared that labour demand is stellar led by strong demand from households. However, the market ignored the surprise rise in employment data and supported Gold prices further.

Technical Analysis

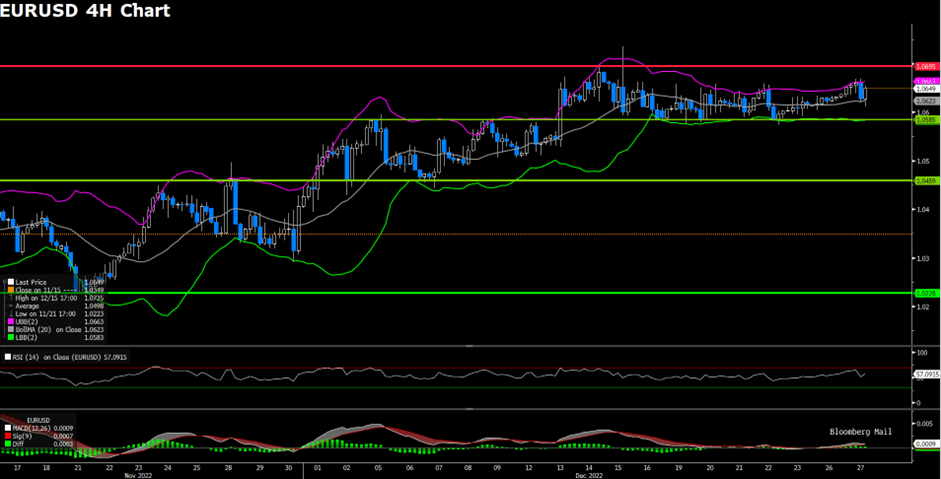

EURUSD (4-Hour Chart)

The Euro Dollar pair witnessed a turbulent trading session on December 2nd. The U.S. nonfarm payrolls for November came in at 263K, above market expectations of 200K. The rather hot payrolls print induced a sell-off in U.S. equity markets and raised interest rate expectations, despite Fed Chair Jerome Powell’s dovish tone on December 1st. On the other hand, Euro bulls have continued to take advantage of the recent Dollar pullback. The surprising dovish signal released by Fed Chair Jerome Powell has continued to put downward pressure on the Dollar. The ECB is expected to hike rates by 50 basis points for December. On the economic docket, ECB president Lagarde is scheduled to speak on the 8th and the 9th.

On the technical side, EURUSD has hit its short-term resistance of 1.06. Short-term support for the pair rests at around 1.035. The 76.4% Fibonacci retracement level of 1.0391 sets another short-term support for EURUSD. RSI for the pair sits at 54.22, as of writing. On the four-hour chart, EURUSD currently trades above its 50, 100, and 200-day SMA.

Resistance: 1.06

Support: 1.0391, 1.035

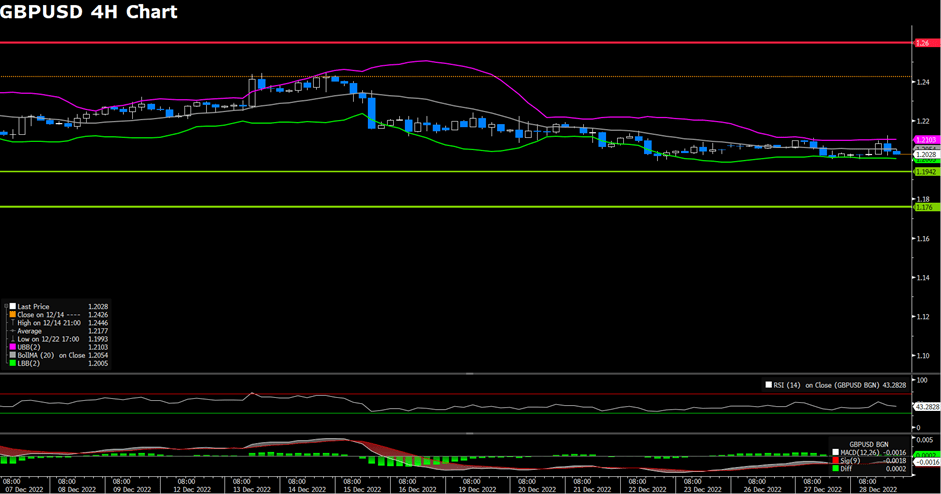

GBPUSD (4-Hour Chart)

GBPUSD snapped its three-day winning streak on the first trading day of the week. The Dollar index’s drop below 105 induced dip buying, which buoyed the U.S. Dollar on the first trading day of the week. U.K. PMI data, released during the European trading session, came in at 48.2, lower than market expectations of 48.3. The lower-than-expected U.K. PMI data has deterred any momentum for Pound bulls. On the economic docket, there are no impactful economic data releases from the U.K. this week. The U.S. will release initial jobless claims and PPI figures on Thursday and Friday, respectively.

On the technical side, GBPUSD has hit its short-term resistance at 1.225. Near-term support for Cable sits at 1.15 and 1.091. The 23.6% Fibonacci retracement also indicates short-term support for Cable. RSI for the pair sits at 49.69, as of writing. On the four-hour chart, GBPUSD currently trades below its 50-day SMA, but above its 100 and 200-day SMA.

Resistance: 1.2400, 1.2600

Support: 1.2154, 1.1927, 1.1765

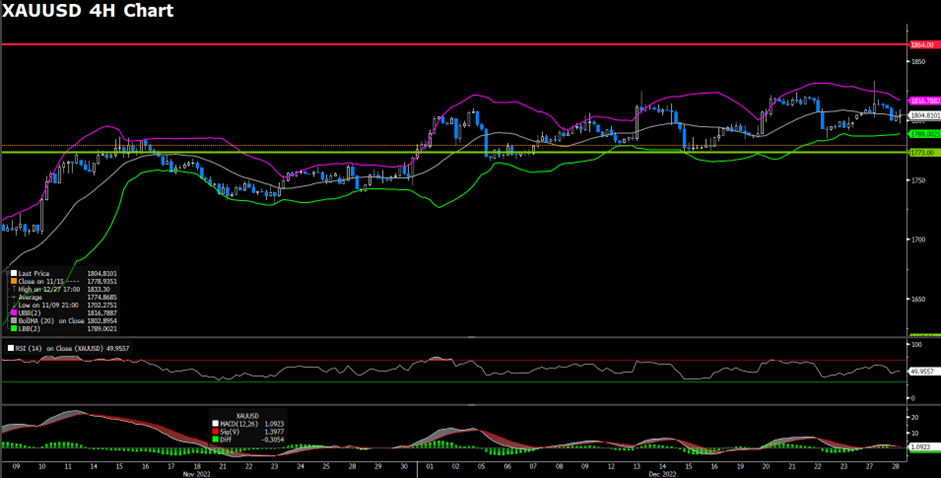

XAUUSD (4-Hour Chart)

Gold extends its losses from last Friday after the U.S. nonfarm payroll data was released. The higher-than-expected nonfarm payrolls figure immediately sparked a rise in the Dollar index and a drop in the Dollar-denominated Gold. Despite market participants expecting a pivot from the Fed, Fed Chair Jerome Powell continues to reiterate that inflation continues to pose a threat to price stability and it is ultimately the central bank’s goal to bring inflation back down to the 2% mark. However, Fed Chair Jerome Powell’s statement regarding a possible “soft landing” of the economy, still instilled optimism across markets. Gold’s drop throughout today’s trading is mainly due to the higher-than-expected PMI data and the resulting stronger Dollar.

On the technical side, XAUUSD has reversed course from its short-term resistance level of around $1800 per ounce. Short-term support for the yellow metal sits at around the $1740 per ounce price region. RSI for Gold sits at 59.63, as of writing. On the four-hour chart, XAUUSD currently trades above its 50, 100, and 200-day SMA.

The Reserve Bank of Australia and the Bank of Canada are expected to further raise interest rates this month. Investors are watching for signs that suggest policymakers will follow through with another hike.

Here are some of the market events to watch this week:

US ISM Services PMI (5 December)

The ISM Services PMI index in the US fell from 56.7 in September to 54.4 in October, missing market expectations of 55.5. This points to a slowdown in the growth of the services sector since May 2020.

Analysts expect another decline in the index, to 53.9 in November.

RBA Rate Statement (6 December)

The Reserve Bank of Australia (RBA) raised the cash rate by 25bps to 2.85% at its November meeting. The board cited concerns over rising inflation in Australia and signalled that further increases were likely necessary.

Analysts predict that RBA will raise interest rates by 25bps to 3.10% this month.

Australian Gross Domestic Products Q/Q (7 December)

Australian gross domestic product (GDP) grew by 0.9% in Q2 of 2022. However, some economists forecast that Australia may enter a recession by 2023 with an unemployment rate of 4.5%.

For Q3, analysts expect GDP to rise to 1.1%.

BOC Rate Statement (7 December)

In October, the Bank of Canada increased its overnight rate by 50bps to 3.75%. This was below the market expectations of an aggressive 75bps hike. Such a move has led to borrowing costs hitting their highest levels since 2008, and added to the 350bps increase in interest rates over the current tightening cycle.

Analysts expect BoC to raise interest rates further by 25bps to 4% this month.

US PPI (9 December)

The PPI for final demand in the US increased 0.2% in October. This was the same as the downwardly revised 0.2% increase in September.

Analysts expect another increase in the US PPI of 0.3% in November.

US Prelim UoM Consumer Sentiment (9 December)

The University of Michigan’s Consumer Sentiment index for the US in November was revised to 56.8, up from a preliminary reading of 54.7.

US stocks edged lower on Friday, as a hot jobs report fueled bets the Federal Reserve will keep tightening even if officials downshift the pace of hikes this month.

Now, the equities and bonds market faced a lot of instability, with the surge in 10-year yields fizzling out while two-year rates remained higher. US employers added more jobs than forecast and wages surged by the most in nearly a year. Nonfarm Payroll increased by 263K in November, while the unemployment rate held at 3.7%. Average hourly earnings rose twice as much as predicted. The resilient labour market is heaping pressure on the Federal Reserve to continue raising rates.

Market participants are all keeping eye on the dot plot, which the central bank uses to signal its outlook for the path of policy. According to Bank of America Corp. strategists, stock investors’ optimism around a cooling labour market and a Fed pivot are overdone.

The benchmarks, S&P 500 and Dow Jones Industrial Average both little changed on Friday, as the S&P 500 almost erased a slide that earlier topped 1% and slid 0.12% daily. Six out of eleven sectors on the S&P 500 stayed in negative territory as the Energy sector is performing the worst among all groups, losing 0.60% for the day. It’s also worth noting that the Materials and Industrials sectors got the best performance on Friday with 1.10 % and 0.62% gain, respectively, daily. Meanwhile, the Nasdaq 100 fell 0.4% on Friday and the MSCI World index slid 0.2% for the day.

Main Pairs Movement

The US dollar edged lower on Friday, with a 50 basis point rate hike remaining favoured despite the full Nonfarm Payrolls report. The US economy added 263K jobs during the last month and the unemployment rate remained at 3.7%, while Average Hourly Earnings rose more than expected by 0.6% MoM and 5.1% from a year earlier. The DXY index was moving a little lower in the first half of Friday but underpinning by a better-than-forecast jobs report. However, the US Dollar failed to hold its ground and dropped to a level of around 104.5.

GBP/USD records modest growth with a 0.27% gain daily following dropping to a daily low of 1.2134 level. The pair ended at the 1.2288 level on Friday, with investors betting more on 50 bps rate hikes in December despite a better-than-expected jobs report. Meanwhile, the EURUSD also confronted heavy selling pressure when the release of the US NFP, dropped to a daily low of 1.0428 level. However, the pair managed to rebound back above the 1.0500 level and rallied by 0.14% for the day.

Gold declined by 0.30 % for the day, witnessing strong selling transactions when the US Payrolls report was released. The XAUUSD managed to stand firmly above the $1795 mark during the late American trading session following a daily low of $1778 marks ahead of the US trading hour.

Technical Analysis

EURUSD (4-Hour Chart)

The EURUSD managed to stage a modest rebound after dropping below 1.0450 with the data from the US showing that Nonfarm Payrolls rose by 263K in November. The pair was climbing back above 1.0500 at the moment of writing. The US. Nonfram Payrolls, measuring the change in the number of people employed without the farming industry during the previous month, printed a surprising 263K figure compared to market forecast of 200K. This report showed that the US labor market remain highly resilient, despite a series of big techs have announced massive layoffs. Further data saw the Unemployment Rate unchanged at 3.7% and the key Average Hourly Earnings, a proxy for inflation via wages, rise 0.6% MoM and 5.1% from a year earlier.

From the technical perspective, the four-hour scale RSI indicator rebounded to 63 figures as of writing, suggesting that the pair was surrounded by strong upside traction. As for the Bollinger Bands, the euro was stably trading above the 20-period moving average, and the size between the upper and lower bands became larger. As a result, we think the pair’s positive tendency would persist shortly.

Resistance: 1.0605, 1.0773

Support: 1.0315, 1.0228, 0.9961

GBPUSD (4-Hour Chart)

The GBPUSD has erased its losses from the early American trading session after diving around 100 pips caused by a better-than-foreseen labour market report in the United States (US). The Department of Labor (DoL) report showed November US Nonfarm Payrolls rose by 263K following an upward revision of 284K jobs added in October. Delving into the information, the Unemployment Rate stood at 3.7%, while Average Hourly Earnings put upward pressure on inflation, jumping 5.1% YoY, vs. 4.6%, consensus. Given that Federal Reserve (Fed) policymakers agreed that moderating the pace of rate hikes is appropriate, how Fed officials look into this would be critical. Apart from this, a weaker Institute for Supply Management (ISM) Manufacturing PMI report for November on Thursday flashed signs of activity contraction, shifted sentiment sour, spurring flows towards safety, except for the US Dollar (USD).

From the technical perspective, the four-hour scale RSI indicator changed its direction suddenly and climbed to 65 figures as of writing, suggesting the pair amid strong bullish momentum. As for the Bollinger Bands, the pair continued to trade in the upper area, meaning the upside traction would persist. As a result, we think if the pound could successfully break through the psychological 1.2400 level, the bulls have a chance to target 1.2600.

Resistance: 1.2400, 1.2600

Support: 1.2154, 1.1927, 1.1765

XAUUSD (4-Hour Chart)

The Gold managed to rebound to above the $1795 mark following a sharp retreat caused by upbeat jobs data. The closely-watched Nonfarm Payroll (NFP) from the United States showed that the economy added 263K new jobs in November, beating consensus estimates pointing to a reading of 200K. Adding to this, the previous month’s print was also revised higher to show an addition of 284K vacancies as compared to the 261K reported initially. Meanwhile, the unemployment rate held steady at 3.7% during the reported month, the same as market expectations. Furthermore, additional details of the report showed that Average Hourly Earnings grew 0.6% in November and 5.1% YoY rate, suggesting a further rise in inflationary pressures. The data validates Federal Reserve Chair Jerome Powell’s forecast that the peak rate will be higher than expected, which triggers a sharp rise in the US Treasury bond yields. This, in turn, prompts an aggressive US Dollar short-covering move and weighs heavily on the Dollar-denominated Gold price.

From the technical perspective, the four-hour scale RSI indicator 63 figured as of writing, suggesting that the gold regained positive strength. As for the Bollinger Bands, the pair held its ground above the 20-period moving average, meaning the upside tendency is more favoured in the near term.

US stocks declined higher on Thursday, struggling for direction and saw a lot of instability near a key technical level as traders awaited the all-important jobs report for clues on the Federal Reserve’s next policy steps. The persistent optimism and tepid US data continued to support the Federal Reserve’s monetary policy pivot and dragged the US Dollar to multi-month lows.

The dovish bias of the Federal Reserve (Fed) Chairman Jerome Powell, as well as downbeat comments from US Treasury Secretary Janet Yellen, initially raised hopes of easy rate hikes. Additionally, some Chinese cities announced they are easing their testing and control coronavirus-related policies, which acted as a tailwind for the equity markets.

On Friday, the US will publish the Nonfarm Payrolls report, which might provide fresh impetus. On the Eurozone front, investors are waiting for the speech from European Central Bank (ECB) President Christine Lagarde.

The benchmarks, S&P 500 and Dow Jones Industrial Average both little changed on Thursday as the S&P 500 closed mixed but the US 10-year Treasury bond yields plummeted to a four-month low. The S&P 500 was down 0.09% daily and the Dow Jones Industrial Average dropped lower with a 0.6% gain for the day. Eight out of eleven sectors in the S&P 500 stayed in negative territory as the Financials sector and the Consumer Staples sector is the worst performing among all groups, losing 0.71% and 0.47%, respectively. The Nasdaq 100 meanwhile was little changed with a 0.1% gain on Thursday and the MSCI World index was up 0.8% for the day.

Main Pairs Movement

The US dollar slumped sharply on Wednesday, suffering from daily losses and dropped towards the 104.70 level amid expectations for the Federal Reserve’s monetary policy pivot. The dovish comments from Fed policymakers favouring a 50 bps Fed rate hike in December allowed the US Treasury bond yields to refresh a four-month low amid receding market pessimism and a rush toward the riskier assets. The focus will then shift to the release of the closely-watched US monthly jobs report – popularly known as NFP.

GBP/USD surged higher on Thursday with a 1.57% gain after jumping above the 1.2030s area as the US Dollar struggles to gain any meaningful traction. On the UK front, the overnight dovish remarks by Bank of England (BoE) Chief Economist Huw Pill failed to drag the cable lower. Meanwhile, EUR/USD regained upside traction and grinds near a five-month high past 1.0500 amid a weaker US dollar across the board. The pair was up almost 1.10% for the day.

Gold rallied sharply with a 1.96% gain for the day after refreshing a four-month high above the $1,800 mark during the US trading session, as the hopes of slower Federal Reserve rate hikes provided strong support to the precious metal. Meanwhile, WTI Oil advanced sharply with a 0.83% gain for the day.

Technical Analysis

EURUSD (4-Hour Chart)

The EURUSD extends its rally above the 1.0500 level following the release of US annual PCE inflation data and the ISM Manufacturing PMI. The data from the US showed the annual Core PCE Price Index declined to 6% in October and the ISM Manufacturing PMI dropped to 49.0 compared to the previous 50.2, triggering a fresh leg of US dollar selloff. Moreover, the US Federal Reserve Chair Jerome Powell dropped the hawkish rhetoric on monetary policy at a private event. Powell acknowledged that moderating the pace of rate hikes is the path to take and may come as soon as December, as progress towards “sufficiently restrictive” police has already been made. The dovish speech undermined the US Dollar situation, which, in turn, provide support for the pair. In the eurozone, German Retail Sales fell by 2.8% MoM in October, much worse than anticipated. Additionally, S&P Global released the final version of its November Manufacturing PMIs, which were downwardly revised. The German index was confirmed at 46.2, while the Euro Area one came down to 47.1 from the previously estimated 47.3. Despite discouraging news for the EUR, the upbeat mood keeps the pair afloat.

From the technical perspective, the four-hour scale RSI indicator surged to 68 figures as of writing, suggesting that the pair was surrounded upbeat market mood. As for the Bollinger Bands, the euro was pricing along with the upper band, and the size between upper and lower bands became larger, which is a signal that the pair would persist in its positive traction in the near term.

Resistance: 1.0604, 1.0774

Support: 1.0315, 1.0228, 0.9961

GBPUSD (4-Hour Chart)

The GBPUSD has preserved its upside traction and was trading around the 1.2250 level as of writing, with the softer-than-expected PCE inflation data and the disappointing ISM Manufacturing PMI weighing heavily on the US Dollar, fueling the pair’s upside. The monthly Core PCE price index declined to 0.3% in October and the annual fell to 6%, compared to the previous of 0.5% and 6.3%. Moreover, the ISM Manufacturing PMI in November fell below the 50 figure to 49.0. The economic data released on Thursday showed easing inflation signs and weakening conditions in the Manufacturing sector, which triggered mounting speculation about less hawkish rate hikes, pushing the greenback further lower. Apart from this, after the FOMC Chairman, Jerome Powell, reaffirmed that smaller rate hikes could come as early as December, the CME FedWatch Tool’s probability of a 50 basis points rate hike at the next policy meeting jumped to 80% from 66%. Powell further added that they have made substantial progress toward a “sufficiently restrictive policy,” further weighing on the USD. The US Dollar index was trading at 104.8 at the moment of writing.

From the technical perspective, the four-hour scale RSI indicator jumped to 70 figured as of writing, which has entered into an overbought zone, suggesting that a corrective pullback could be expected in the near term. As for the Bollinger Bands, the pair was priced above the upper band, and the size between the upper and lower bands get larger, meaning the bullish momentum would persist shortly.

Resistance: 1.2400, 1.2600

Support: 1.2154, 1.1927, 1.1765

XAUUSD (4-Hour Chart)

The XAUUSD jumped above a critical psychological level of $1800, the highest since early August. The precious metal benefited from an extended USD sell-off as US macroeconomic figures fueled Powell’s triggered slump. On Wednesday, the Dollar fell on the back of a dovish message from Fed’s Powell.

The US Dollar remained under pressure throughout all day, extending its losses during the US trading session. On the one hand, the Personal Consumption Expenditures (PCE) Price Index rose by 6% YoY in October, easing from 6.3% in the previous month. In addition, core PCE inflation came in at 5% in the same period, down from 5.2% in September. On the other, the ISM Manufacturing PMI fell to 49 in November, down from the previous 50.2, being the first time the indicator signals contraction since the early stages of the pandemic. The events reflect the high risk of an economic setback after the US central bank aggressively hiked rates to tame inflation. Price pressures give signs of receding, although the risk of an economic downturn has increased.

From the technical perspective, the four-hour scale RSI indicator rose above 75 figures as of writing, suggesting that the pair was surrounded by strong upside momentum and the market mood. As for the Bollinger Bands, the pair was priced above and along with the upper band, and the gap between upper and lower bands became larger, signalling that the pair was more favoured to the upside path shortly.

Warmly reminds you that the component stocks in the stock index spot generate dividends. When dividends are distributed, VT Markets will make dividends and deductions for the clients who hold the trading products after the close of the day before the ex-dividend date.

Indices dividends will not be paid/charged as an inclusion along with the swap component. It will be executed separately through a balance statement directly to your trading account, the comment for which will be in the following format “Div & Product Name & Net Volume ”.

Please note the specific adjustments as follows:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The new futures rollover dates are listed in the table below.

Please note:

• The rollover will be done automatically. All existing positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, you can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

Please contact our customer service team at [email protected] if you have any questions.

US stocks rallied sharply on Wednesday, witnessing fresh buying and extending the daily rally as Jerome Powell signalled a slowdown in the pace of tightening as early as December while indicating more hikes to fight inflation. The dovish comments from Federal Reserve (Fed) Chairman Jerome Powell provided strong support to the equity markets, as he was dovish while saying it makes sense to moderate the pace of interest rate increases and added that the monetary policy would need to remain restrictive for some time.

Additionally, Powell said that the time to slow the pace of rate hikes could come as soon as the next meeting in December and he does not want to over-tighten. Powell’s comments likely cement expectations for the Fed to hike by 50 basis points in December, following four straight 75 basis-point moves. However, rates are likely to reach a somewhat higher level than officials estimated in September. On the Eurozone front, European inflation fell for the first time in seventeen months, as the Euro Area annual Harmonized Consumer Price Index printed at 10% in October.

The benchmarks, S&P 500 and Dow Jones Industrial Average both advanced higher on Wednesday as the S&P 500 hit a two-month high and notched the longest monthly winning streak since August 2021 amid all the optimism. The S&P 500 was up 3.1% on a daily basis and the Dow Jones Industrial Average climbed higher with a 2.2% gain for the day. All of the eleven sectors in the S&P 500 stayed in positive territory as the Information Technology sector and the Communication Services sector are the best performing among all groups, losing 5.03% and 4.91%, respectively. The Nasdaq 100 meanwhile advanced the most with a 4.6% gain on Wednesday and the MSCI World index was up 2.5% for the day.

Main Pairs Movement

The US dollar slumped sharply on Wednesday, suffering from daily losses and dropped towards the 105.80 level amid US Federal Reserve Chair Jerome Powell’s dovish comments. The policymaker stated that it makes sense to moderate the pace of interest rate increases while also suggesting that the time to slow the pace of rate hikes could come as soon as the next meeting in December. Therefore, the chances of a 50 bps rate hike in December increased from 69.9% ahead of the speech to above 75%.

GBP/USD advanced higher on Wednesday with a 0.89% gain after jumping above the 1.2030s area as the Fed pivots to lower hikes. On the UK front, the Bank of England (BoE) Chief Economist Huw Pill said inflation is expected to fall quickly in the second half of 2023 while supply chain issues are being solved. Meanwhile, EUR/USD regained upside traction and jumped from weekly lows of 1.0290 amid a weaker US dollar across the board. The pair was up almost 0.74% for the day.

Gold rallied sharply with a 1.07% gain for the day after posting the biggest daily jump in three weeks around the $1,775 level during the US trading session, as the dovish comments from Fed Chairman Jerome Powell and optimism surrounding China both support the precious metal. Meanwhile, WTI Oil advanced sharply with a 3.01% gain for the day.

Technical Analysis

EURUSD (4-Hour Chart)

The EURUSD turned south and witnessed heavy selling pressure during the US trading session, as the US Dollar Index gathered strength following the mixed macroeconomic data releases while investors await FOMC Chairman Jerome Powell’s speech. The pair was trading at the 1.032 level at the moment of writing. Earlier, the National Association of Realtors (NAR) released the United States Pending Home Sales Report, which printed -4.6%, compared to market expected -5.0% and the previous -8.7%. Apart from this, the United States ADP Nonfarm Employment Change shows an increase of 127K in November, far from the forecast 200K and the previous 239K. Furthermore, the second estimate of the Q3 Gross Domestic Product (GDP) rallied to 2.9%, higher than the expectation of 2.7% and the previous 2.6%. The better market mood helps the EUR amid news suggesting China’s government has decided to ease coronavirus-related restrictions in Zhengzhou and Guangzhou. The country has continued to report record daily contagions, but massive protests across the country have forced the decision. Now, the US Dollar regained bullish strength ahead of FOMC Chairman Jerome Powell’s speech.

From the technical perspective, the four-hour scale RSI indicator surged to 54 figured following the dovish speech by Fed Chairman Jerome Powell, suggesting that the pair was amid an upbeat market mood. As for the Bollinger Bands, the euro was priced above the 20-period moving average, in a case that successfully breaks through the upper band, the bull has the chance to challenge the multi-month high 1.0497 level.

Resistance: 1.0497, 1.0604

Support: 1.0228, 1.0163, 0.9961

GBPUSD (4-Hour Chart)

The GBPUSD has reversed its direction and declined toward 1.1900 after having climbed above 1.2000 earlier in the day, as the safe-haven greenback benefits from the cautious mood ahead of Powell’s speech. The market sentiment remained fragile, as shown by US equities wavering. Latest Federal Reserve officials commented that the US central bank is ready to moderate the pace of rate hikes but also stated that rates would end higher than September projections. Therefore, any hawkish tilt remarks by Jerome Powell could rock the boat and bolster the US Dollar. On the data side, the ADP Employment Change report for November disappointed investors as the economy added just 127K jobs below expectation and trailed the 239K employees hired by private companies in October. Moreover, the US Gross Domestic Product (GDP) for the third quarter, on its second estimate, increased by 2.9% above forecasts of 2.7%, smashing Q3’s advanced reading of 2.6%. The higher-than-expected report sent recession speculations in the United States to the trash can. In the domestic, the BoE’s chief economist Huw Pill foresees rates to peak lower than the market projections and echoed the BoE’s Governor Andrew Bailey’s remark at the last monetary policy meeting. Therefore, further GBP weakness is expected.

From the technical perspective, the four-hour scale RSI indicator rallied to 54 figures after a less aggressive remark by Federal Reserve Chairman, Jerome Powell, suggesting that the pair were surrounded by positive market sentiment. As for the Bollinger Bands, the pair was priced above the 20-period moving average, meaning that the pair was more favoured to the upside path.

Resistance: 1.2124, 1.2253

Support: 1.1764, 1.1645, 1.1366

XAUUSD (4-Hour Chart)

The Gold was holding on to modest intraday gains after hitting a fresh weekly high, as investors await US Federal Reserve Chair Jerome Powell’s words to move more aggressively and mixed US data showed better-than-anticipated growth but tepid employment performance. The intraday US Dollar selling was witnessed following the disappointing release of the ADP report, showing that the US private-sector employers added 127K jobs in November. The headline print was well below the previous month’s reading of 239K and 200K anticipated. This tempered expectations for any positive surprise from the official jobs report (Nonfarm Payroll) on Friday. However, the upbeat GDP report capped the upside for the yellow metal ahead of Powell’s speech. The preliminary report released by the US Bureau of Economic Analysis showed that the economy expanded by 2.9% annualized pace during the third quarter against 2.6% reported previously. Traders will look for clues about future rate hikes upon Jerome’s speech and provide a fresh directional impetus to the non-yielding gold.

From the technical perspective, the four-hour scale RSI indicator rose to 59 figures after Powell’s dovish speech, suggesting that the yellow metal was attracting some flow from the greenback. As for the Bollinger Bands, the pair was challenging the upper band and two-week high $1767 mark at the moment of writing. As a result, we think the gold would move upward in the near future and target the $1784 mark if successfully stand firmly above $1767.

US stocks edged lower on Tuesday, regaining upside traction and paring most of their daily losses with traders unwilling to make big bets ahead of Jerome Powell’s speech Wednesday. Jerome Powell is expected to cement expectations the Fed will slow its pace of hikes next month and remind investors that its fight against inflation will run into 2023.

The need for more measured rate rises will also take account of increased two-way economic risks as policy becomes restrictive. Meanwhile, the US central bank is expected to hike rates by an additional 50 basis points when it meets on Dec. 13-14, though the odds of a 75-basis-point increase have risen over the past several weeks and now stand at a 37% probability.

Moreover, market mood improved slightly as Chinese authorities announced multiple measures to ease the strict lockdown in the key areas after witnessing a retreat in the daily Covid infections from a record high. On the Eurozone front, the sentiment remains supportive of the Euro in that the European Central Bank remains committed to raising interest rates to dampen high inflation.

The benchmarks, S&P 500 and Dow Jones Industrial Average both declined lower on Tuesday as the S&P 500 rebounded back slightly with gains in energy and financial firms tempered a slide in big tech. The S&P 500 was down 0.2% on a daily basis and the Dow Jones Industrial Average was little changed with a 0.1% loss for the day. Six out of eleven sectors in the S&P 500 stayed in negative territory as the Information Technology sector and the Utility sector are the worst performings among all groups, losing 0.98% and 0.73%, respectively. The Nasdaq 100 meanwhile dropped the most with a 0.7% loss on Tuesday and the MSCI World index was unchanged for the day.

Main Pairs Movement

The US dollar advanced higher on Tuesday, preserving its upside momentum and extending its daily gains towards the 106.80 area amid a cautious market mood. The 10-year US Treasury yields have accelerated to 3.75% as Fed policymakers see no halt in rate hike culture in the near term, which helped the US Dollar Index (DXY) to print a three-day uptrend despite softer statistics from the United States. This week, the US Nonfarm Payrolls (NFP) is the key event that investors will focus on.

GBP/USD retreated slightly on Tuesday with a 0.06% loss as the cable dropped to a daily low near the 1.1940 mark in the late US trading session amid a cautious market mood. On the UK front, the speech from Bank of England (BOE) Governor Andrew Bailey on Tuesday failed to provide support for the British Pound. Meanwhile, EUR/USD suffered from daily losses and pared the biggest monthly gains since September 2010 amid a stronger US dollar across the board. The pair was down almost 0.10% for the day.

Gold advanced higher with a 0.49% gain for the day after struggling around the $1,750 level ahead of Fed Powell’s speech during the US trading session, as expectations for a less aggressive policy tightening by the Federal Reserve underpinned the precious metal. Meanwhile, WTI Oil advanced sharply with a 1.24% gain for the day.

Technical Analysis

EURUSD (4-Hour Chart)

The EURUSD was having difficult time gathering upside strength and hovering around the 1.0335 level as of writing, with Wall Street’s main indices declining further after the opening bell, the US Dollar was trying to attract positive traction and weighing on the pair. Earlier, the euro was initially boosted by the hopes of a potential easing in China’s strict pandemic restrictions following an unprecedented episode of unrest in the country. However, the pair failed to preserve its daily gain during the US trading session. The Conference Board’s (CB) index shaved off 2 points to come in at 100.2, a hair above the 100 consensuses. In the meantime, flash euro zone inflation figures for November are due on Wednesday, with economists polled by Reuters expecting inflation to come in at 10.4% year-on-year. The key event, however, for Wednesday will be in the comments from Fed Chair Jerome Powell. These will be scrutinised for new signals on further tightening. The Fed is widely expected to hike rates by an additional 50 basis points when it meets on Dec. 13-14.

From a technical perspective, the four-hour scale RSI indicator edged lower to 43 figures as of writing, suggesting that the pair was amid negative traction. As for the Bollinger Bands, the pair was priced in the lower area and supported by the lower band. As a result, in case the pair was falling below the lower band, the bears have the chance to test the weekly low 1.0228 level.

Resistance: 1.0497, 1.0604

Support: 1.0228, 1.0163, 0.9961

GBPUSD (4-Hour Chart)

The GBPUSD has turned south and fell below the 1.2000 level in the second half of the day on Tuesday, as the negative shift witnessed in risk sentiment seems to be helping the US Dollar find demand and forcing the pair to stay on the back foot. The US equities wavered as Wall Street opened, as the St.Louis Fed President James Bullard said that the Fed has “a ways to go to get a too restrictive policy,” adding that the first 250 bps was to get rates neutral. He emphasized that rates need to be at around 5% to 7% through 2023 and 2024. In fact, money market futures have priced in a 50 bps hike in December, with odds of a 75 jumbo increase at 15%. Apart from this, the Covid-19 outbreak has not escalated as initially thought, as global equities remained mixed but tilted to the upside on early Tuesday. According to the Wall Street Journal, the National Health Commission urged local governments to avoid unnecessary and lengthy lockdowns. On the data side, the Conference Board (CB) Consumer confidence, decreased to 100.2 a 4-month low. Lynn Franco, senior director of economic indicators at the Conference of Board, said that the combination of inflation and interest rate hikes will continue to pose challenges to confidence and economic growth into early 2023.

From the technical perspective, the four-hour scale RSI indicator edged lower to 39 figures as of writing, suggesting that the pair was surrounded by strong bearish momentum. As for the Bollinger Bands, the pair was pricing along with the lower band and trying to find some support from it, meaning that the British Pound is likely to move downward in the near future.

Resistance: 1.2123, 1.2253

Support: 1.1765, 1.1647, 1.1366

XAUUSD (4-Hour Chart)

The XAUUSD rallied on Tuesday, recovering after Monday’s slide. The gold price has almost reversed the previous day’s losses, having captured the $1750 mark amid a renewed sell-off in the US Dollar across its main rivals. Earlier on Tuesday, the three-day coronavirus lockdown-induced protests across China eased. Chinese equity markets rebounded firmly on expectations that the government will further relax its zero-Covid policy after the weekend protests. China’s authorities announced new property market measures while Global Times tweets suggested that the government could do away with its stringent zero-Covid policy sooner. These developments from China improved the market risk sentiment and triggered a sharp retreat in the safe-haven greenback, which, in turn, boosted the dollar-denominated gold. Nevertheless, the further recovery in Gold prices could be capped by the buoyant tone seen around the US Treasury bond yields, which recovered sharply on Monday after the hawkish commentary from the US Federal Reserve officials.

From the technical perspective, the four-hour scale RSI indicator recovered to neutral level 48 figured as of writing, suggesting that the gold has not made a decisive move. As for the Bollinger Bands, the pair was fluctuating around the 20-period moving average, signalling that the yellow metal would get into a consolidation phase ahead of any surprising event.