Key Points

- The Fed held rates at 3.50% to 3.75%, but the 8 to 4 vote split showed a deeper divide over inflation, growth, and the next policy move.

- Oil remains the key macro variable as prices above $100 keep inflation expectations and rate-cut pricing under pressure.

- The week’s main data risk sits with the RBA cash rate decision, US JOLTS job openings, and Friday’s US Non-Farm Payrolls report.

- Technical setups still favour selective dollar weakness, gold strength, firm oil, and cautious risk appetite unless US labour data changes the Fed narrative.

Markets enter the new week with one question doing most of the heavy lifting: can the Fed cut rates if oil keeps inflation alive?

The Fed held rates at 3.50%-3.75%, but the real story was the split vote. An 8-to-4 division marked the most divided FOMC decision since 1992, showing that policymakers no longer agree cleanly on the next step. One side sees slowing growth and wants room to ease.

The other still sees inflation risk, especially with energy prices feeding into transport costs, goods prices, wages, and inflation expectations.

Higher Oil Keeps The Fed Boxed In

If oil stabilises, inflation can still ease later in the year. If oil stays above $100 or pushes higher, the Fed becomes boxed in. It cannot cut aggressively while energy-driven inflation threatens to move through the wider economy.

This is why Powell’s tone still holds weight. He described the US economy as resilient, with growth expected to stay above 2% this year, supported by consumer spending and data centre investment. That is not the language of a central bank racing to cut. It sounds more like a late-cycle economy where growth still holds up, but inflation refuses to fade cleanly.

The market impact is clear. Strong growth reduces the urgency for cuts. Sticky inflation reduces the room for cuts. Higher oil reduces the Fed’s freedom further. That mix supports the “higher for longer” trade and keeps bond yields, the dollar, gold, oil, and equities vulnerable to sharper moves.

The labour market now has to carry a lot of weight. Friday’s US Non-Farm Payrolls report is forecast at 60K, down from 178K, while unemployment is expected to hold at 4.3%. A soft jobs print could revive rate-cut bets, but only if wage and inflation signals do not look too sticky. A stronger print would give the Fed more reason to wait.

Australia returns to the spotlight this week. The RBA cash rate decision comes with markets watching for a move from 4.10% to 4.35%, as inflation concerns remain in focus. For AUDUSD, the reaction may depend on whether the RBA confirms a more restrictive path or sounds more cautious about growth risks.

Markets may stay volatile rather than directional. Oil needs to cool before risk assets get cleaner upside air. Until then, the Fed remains boxed in, the dollar may stay choppy, gold can stay supported on dips, and equities may need strong earnings or softer labour data to extend gains.

Key Symbols to Watch

- USDX

- XAUUSD

- USOil

- SP500

- BTCUSD

- USDJPY

Key Events of the Week

| Date | Currency | Event | Forecast | Previous | Analyst Remarks |

| Tue, May 05 | AUD | Cash Rate | 4.35% | 4.10% | A hawkish RBA can support AUDUSD near key bullish zones. |

| Tue, May 05 | USD | JOLTS Job Openings | 6.87M | 6.88M | Labour demand will shape the next Fed rate-cut debate. |

| Fri, May 08 | USD | Non-Farm Employment Change | 60K | 178K | Payrolls can reset USDX, XAUUSD, and SP500 direction. |

| Fri, May 08 | USD | Unemployment Rate | 4.30% | 4.30% | A higher rate may revive Fed rate-cut expectations. |

Next week’s data calendar also matters, with US CPI y/y due on 12 May, US PPI m/m on 13 May, GBP GDP m/m on 14 May, and US Retail Sales m/m on 14 May. These releases could decide whether markets treat oil as a temporary inflation shock or a larger policy problem.

For a full view of upcoming economic events, check out VT Markets’ Economic Calendar.

Key Movements Of The Week

USDX

- USDX remains under pressure after the prior sell-off, but the index may attempt to consolidate higher.

- The 98.20 area is the key resistance zone to watch for bearish price action.

- If price later takes out the 97.399 swing low, the dollar may face renewed downside pressure.

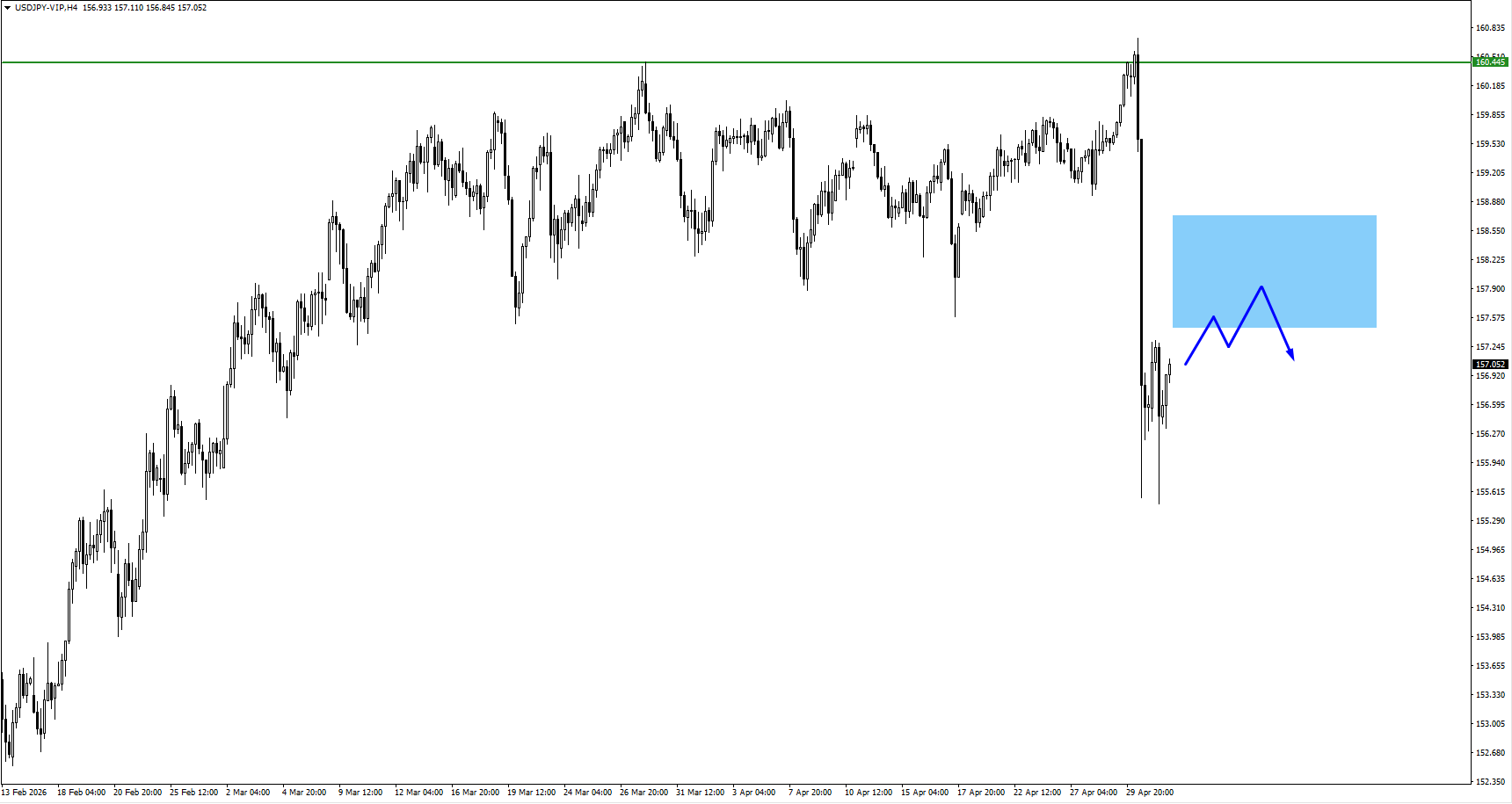

USDJPY

- USDJPY traded upward from the 158.90 monitored area and broke above 160.45 before pulling back.

- The pullback puts focus on whether upside retracements attract fresh selling.

- Bearish price action may be watched at 157.50, 158.10, or 158.70 if price consolidates upward.

USOil

- USOil continued to rise after breaking above 103.75, then retraced.

- The broader structure still leaves room for another upside extension if price consolidates cleanly.

- Oil remains the main macro pressure point because sustained strength can keep inflation and Fed policy risk alive.

Gold

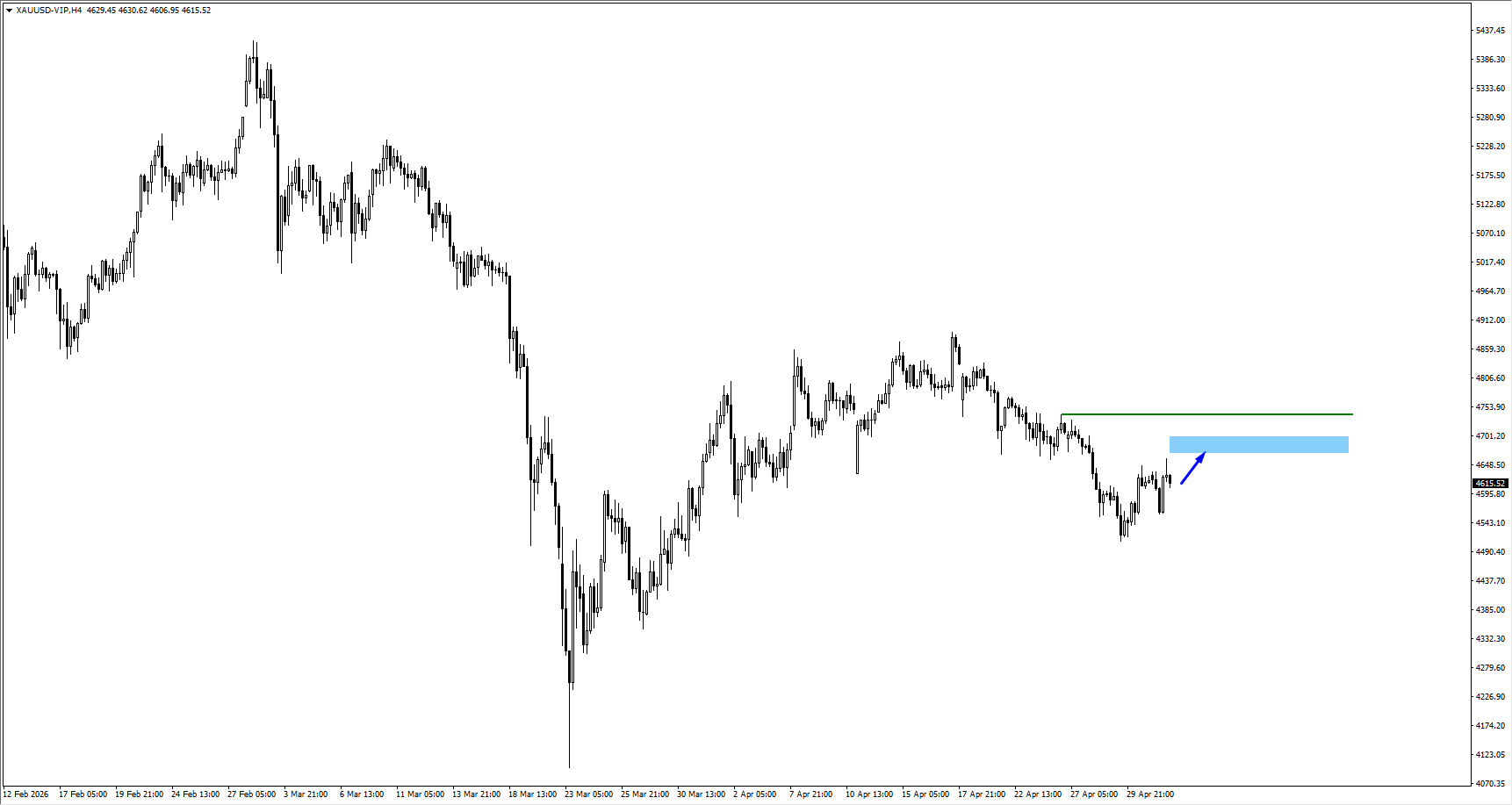

- Gold broke 4633.39 and traded higher.

- The move fits the broader macro backdrop of sticky inflation, delayed rate-cut hopes, and geopolitical risk.

- As price moves higher, 4690 is the next area to monitor for price action.

SP500

- SP500 continued to trade higher and remains near all-time highs.

- Traders should monitor price action closely because stretched rallies can attract profit taking.

- If the 7110 swing low is taken out, profit taking could be underway.

Bitcoin

- Bitcoin traded higher from the 75,600 area.

- The structure remains constructive if risk appetite holds and the dollar stays capped.

- If price consolidates next, 77,550, 77,000, and 76,550 are the key zones to watch for bullish price action.

Bottom Line

The week ahead is less about one data print and more about the market regime forming around it. A divided Fed, oil above $100, and resilient growth create a difficult setup for traders. Softer US labour data may help risk assets and gold, but oil must cool before markets can price an easier Fed path with confidence. Until then, rallies in SP500 and BTCUSD may need confirmation, USDX may stay volatile around resistance, and XAUUSD can remain supported if inflation and geopolitical risk stay in focus.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Trader Questions

Why Is Oil So Important For The Fed This Week?

Oil matters because it can keep inflation pressure alive even when other parts of the economy slow. Higher energy prices feed transport costs, goods prices, inflation expectations, and wages. That makes it harder for the Fed to cut rates quickly.

What Would A Weak NFP Report Mean For Markets?

A weak NFP report could revive rate-cut hopes and pressure the dollar. Gold, SP500, and BTCUSD may benefit if traders see softer jobs growth without a fresh inflation scare. The reaction may fade if wages stay hot or oil keeps rising.

What Would A Strong NFP Report Mean For Markets?

A strong NFP report would support the Fed’s patient stance. It could lift USDX and bond yields while creating short-term pressure on gold, equities, and crypto. The key risk is that strong jobs plus high oil keeps the higher-for-longer story alive.

What Should Traders Watch On USDX?

The key level is 98.20. A bearish reaction there could confirm that dollar rallies are still being sold. A break below 97.399 would add pressure and may support EURUSD, GBPUSD, gold, and other risk-sensitive assets.

Is Gold Still Bullish This Week?

Gold still has support from delayed rate cuts, inflation risk, and geopolitical tension. The next area to watch is 4690. A clean reaction there could decide whether buyers keep control or whether price needs a deeper consolidation first.

Start trading now – Click here to create your real VT Markets account