Key Points

- NVIDIA is back in focus after the U.S. cleared H200 AI chip sales to around 10 Chinese firms.

- CEO Jensen Huang’s China visit has turned the H200 issue into a fresh market catalyst.

- China remains a key swing factor as NVIDIA works to defend access to a major AI market.

- The core AI story remains strong, but export controls and valuation pressure keep the trade volatile.

NVIDIA is no longer moving only on chip demand. It is now moving on diplomacy.

The company has returned to the centre of the U.S.-China technology debate after the U.S. government approved H200 AI chip sales to around 10 Chinese companies, including Alibaba, Tencent, ByteDance and JD.com. CEO Jensen Huang also joined President Donald Trump’s China visit, raising hopes that direct diplomacy could help break the current shipment deadlock.

China remains one of the few large markets where policy, rather than demand, has capped NVIDIA’s reach. The company once held a dominant position in China’s advanced AI chip market, but shipments have stalled as Beijing weighs national security concerns and the risk of weakening its domestic AI chip push.

The H200 story adds a fresh layer to the NVIDIA trade. The company does not need China to prove that AI demand is real. Its earnings already show that. China could instead decide whether the next leg of NVIDIA’s growth comes from a fresh revenue channel or another round of geopolitical pressure.

Why The H200 Chip Sits At The Centre Of The Debate

The H200 has become more than a product. It now sits at the centre of a wider fight over AI leadership, chip access, and national security.

NVIDIA’s high-end AI chips power model training, inference workloads, cloud computing, and enterprise AI deployment. China wants access to that compute power, while U.S. policymakers want to control technology flows that could strengthen Beijing’s AI capabilities.

Every H200 headline now carries market weight. A shipment breakthrough would suggest Washington and Beijing can still carve out commercial space inside a strategic rivalry. Another delay would show that advanced chip access remains one of the hardest parts of the U.S.-China relationship.

The market may be too quick to treat any China headline as an automatic positive. A partial reopening would help NVIDIA, but it would not restore the old operating environment. China has changed. The U.S. has changed. AI chips have become strategic assets, and NVIDIA now sits between two governments with competing priorities.

China access could lift the stock, but it could also make NVIDIA’s risk profile more visible.

China Could Add Upside, But Not Certainty

A China H200 deal would give NVIDIA an important revenue channel, but approval alone does not create growth.

The U.S. has cleared H200 sales to major Chinese firms and distributors, but shipments still need to move through customer demand, purchase orders, licence terms, and policy stability. Beijing has also hesitated because it does not want to weaken the domestic AI chip sector at a time when self-sufficiency has become a national priority.

That creates a more complicated setup for traders. Approval is one step. Revenue is another. NVIDIA still needs clear shipment timing, customer uptake, and enough political stability for Chinese buyers to commit at scale.

China also has a long-term reason to reduce dependence on U.S. chips. Export controls have already pushed Chinese technology firms and policymakers to support domestic semiconductor alternatives. A partial reopening may help NVIDIA in the near term, but it is unlikely to stop China’s wider AI chip independence drive.

The H200 issue should be treated as optional upside, not the foundation of the bull case. It can add fuel to the NVIDIA story, but it can also add volatility.

Export Controls Remain The Real Risk

The H200 story sits inside a larger semiconductor fight.

China has criticised the proposed U.S. MATCH Act ahead of high-level Beijing talks. The bill aims to restrict China’s access to advanced semiconductor manufacturing equipment and pressure U.S. allies such as Japan and the Netherlands to adopt similar controls.

That backdrop keeps NVIDIA exposed to policy shifts. Even if H200 sales restart, the U.S. could tighten rules again. China could also retaliate against U.S. technology companies if chip restrictions deepen.

China is not only a growth opportunity for NVIDIA. It is also the clearest reminder that the AI trade now sits inside national security policy.

A clean commercial deal would support sentiment. A restricted deal could disappoint investors who expected a wider reopening. A renewed policy block could quickly turn China from a bullish catalyst into a valuation risk.

NVIDIA’s Core AI Story Still Looks Strong

The China question adds volatility, but it does not carry NVIDIA’s whole investment case.

NVIDIA reported record Q4 FY2026 revenue of $68.1 billion, up 20% from the previous quarter and 73% from a year earlier. Data centre revenue reached $62.3 billion, up 22% quarter on quarter and 75% year on year. Full-year revenue rose 65% to $215.9 billion.

Those numbers show that AI demand is still converting into revenue at scale. NVIDIA’s data centre business remains the central engine, supported by hyperscaler spending, model training, inference growth, networking, and full-stack systems.

The bull case does not depend entirely on China. NVIDIA already has the strongest earnings proof in the AI infrastructure trade. China can expand opportunities, but it does not define the entire business.

The market, however, looks forward. Investors are now asking where the next layer of growth comes from after the first wave of AI infrastructure spending. China offers one possible answer, though with more political risk than most growth catalysts.

Interested in trading major market themes like AI, chips, and U.S.-China risk? Explore VT Markets’ share CFDs and follow price action across leading U.S. technology stocks.

The Valuation Test Is Getting Harder

NVIDIA’s growth remains exceptional, but exceptional growth is already the market’s starting point.

That is the challenge for a stock that has become the face of the AI trade. Strong earnings may no longer be enough. Investors now want proof that NVIDIA can keep expanding its addressable market, defend margins, and stay ahead of regulatory and competitive pressures and customer concentration risk.

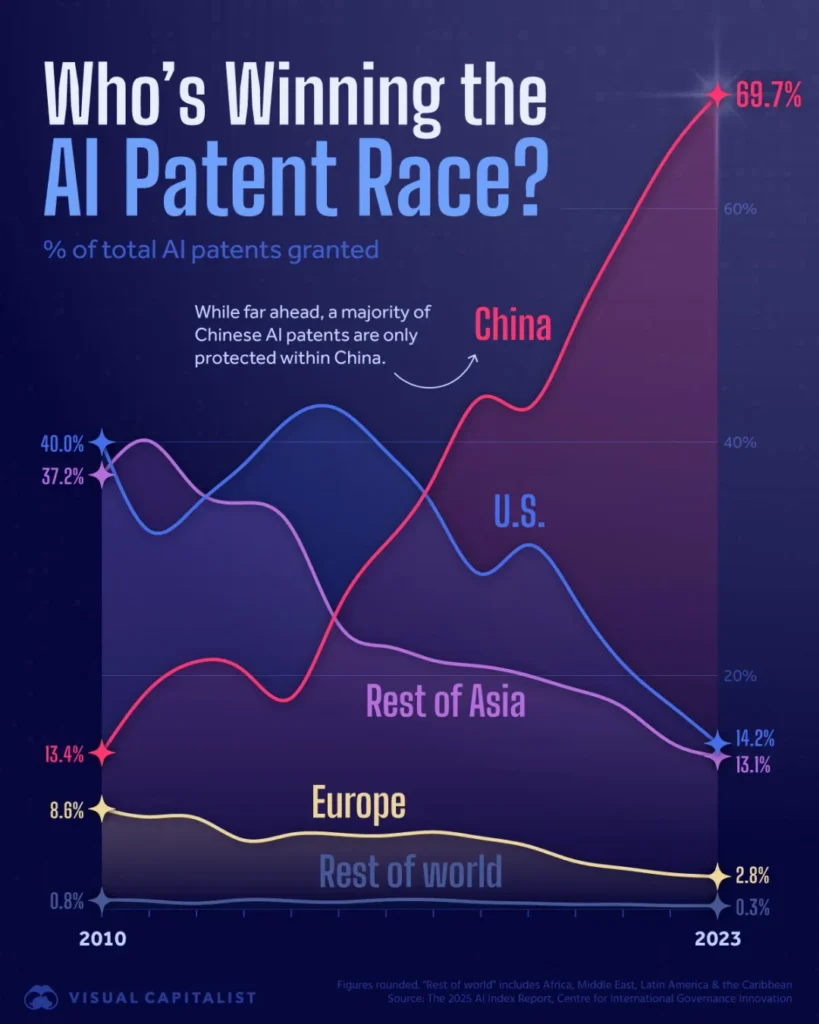

Source: Visual Capitalist

China fits directly into that valuation debate. A clean H200 deal could give investors a new reason to keep paying a premium. A vague or restricted deal may do less than bulls expect. A failed deal could remind the market that even NVIDIA cannot fully outrun politics.

That does not weaken NVIDIA’s core position. It raises the bar. The company has already proved that AI demand is real. Now it must keep proving that the growth runway remains wide enough to support the valuation attached to it.

What A China Deal Would Mean For Traders

A China H200 breakthrough would likely support bullish sentiment toward NVIDIA, especially if it improves order visibility and reduces concerns about lost share in China.

The strongest reaction would likely come from a deal that gives clear shipment timing, workable sale terms, and enough policy stability for Chinese customers to place meaningful orders. That would turn China from a restricted market into a partial growth channel again.

A weaker outcome would be more complicated. A broad political statement without shipment clarity may spark a short-term rally, but traders may fade that move if purchase orders fail to follow.

The downside scenario is a renewed policy block. If talks fail, if Washington tightens restrictions, or if Beijing pushes customers toward domestic alternatives, NVIDIA may still rely on strong global AI demand, but the China premium could fade quickly.

NVIDIA Forecast: Strong Core, Volatile Catalyst

NVIDIA still carries a constructive bias while data centre growth remains this strong. Few companies have turned the AI boom into revenue as effectively, and fewer have built such a deep lead across chips, systems, networking, and software.

But the stock is no longer trading on discovery. It is trading on confirmation. Investors already know NVIDIA is the AI leader. They now need fresh proof that the growth runway can stay wide enough to support the valuation.

China gives the stock a powerful but unstable catalyst.

A workable H200 agreement could extend the bullish narrative and give NVIDIA another growth channel. Yet traders should avoid treating it as a simple green light. Any deal will likely carry conditions, political scrutiny, and the risk of future restrictions.

The base case remains positive, but more fragile than the headline numbers suggest. NVIDIA can keep leading the AI trade, but the stock may become more sensitive to policy risk as its valuation leaves less room for disappointment. Track the themes driving NVIDIA, AMD, Microsoft, Meta, and the wider Nasdaq 100.

What Traders Should Watch Next

Traders should watch for direct updates on H200 shipment approval, sale terms, and Chinese customer demand. Purchase orders would matter more than diplomatic language.

They should also track NVIDIA’s next earnings guidance. Data centre revenue, gross margin, Blackwell demand, and China commentary will shape whether the stock can extend its AI premium.

The final signal is U.S.-China policy language. If chip talks remain constructive, NVIDIA may hold its China upside. If the summit shifts toward tougher controls, the market may treat the H200 story as another geopolitical risk rather than a growth catalyst.

Keep your eyes on VT Markets’ Weekly Market Outlook to get the latest news around the Trump-Xi Summit.

FAQs

Why Is NVIDIA In The News?

NVIDIA is in focus because the U.S. has cleared H200 AI chip sales to around 10 Chinese firms, while CEO Jensen Huang has joined President Donald Trump’s China visit. The issue has become a key part of the wider U.S.-China technology debate.

What Is The NVIDIA H200 Chip?

The H200 is one of NVIDIA’s advanced AI chips used for high-performance computing and AI workloads. It matters because Chinese companies want access to advanced AI compute, while U.S. policymakers want to control technology that could strengthen China’s AI capabilities.

Why Does China Matter For NVIDIA?

China matters because it remains one of the world’s largest AI markets. Reuters reported that NVIDIA once held about 95% of China’s advanced AI chip market, so any reopening of H200 sales could improve the company’s growth visibility.

Could A China Deal Boost NVIDIA Stock?

A China deal could support NVIDIA stock if it leads to clear shipment timing, purchase orders, and revenue visibility. The impact would depend on sale terms, regulatory approval, and whether Chinese customers can buy without further policy delays.

What Is The Main Risk For NVIDIA?

The main risk is policy. Export controls, U.S.-China tensions, Chinese retaliation, and domestic competition in China could limit NVIDIA’s access to the market. Valuation is also a risk because the stock already reflects very high expectations for AI growth.

Start trading now – Click here to create your real VT Markets account