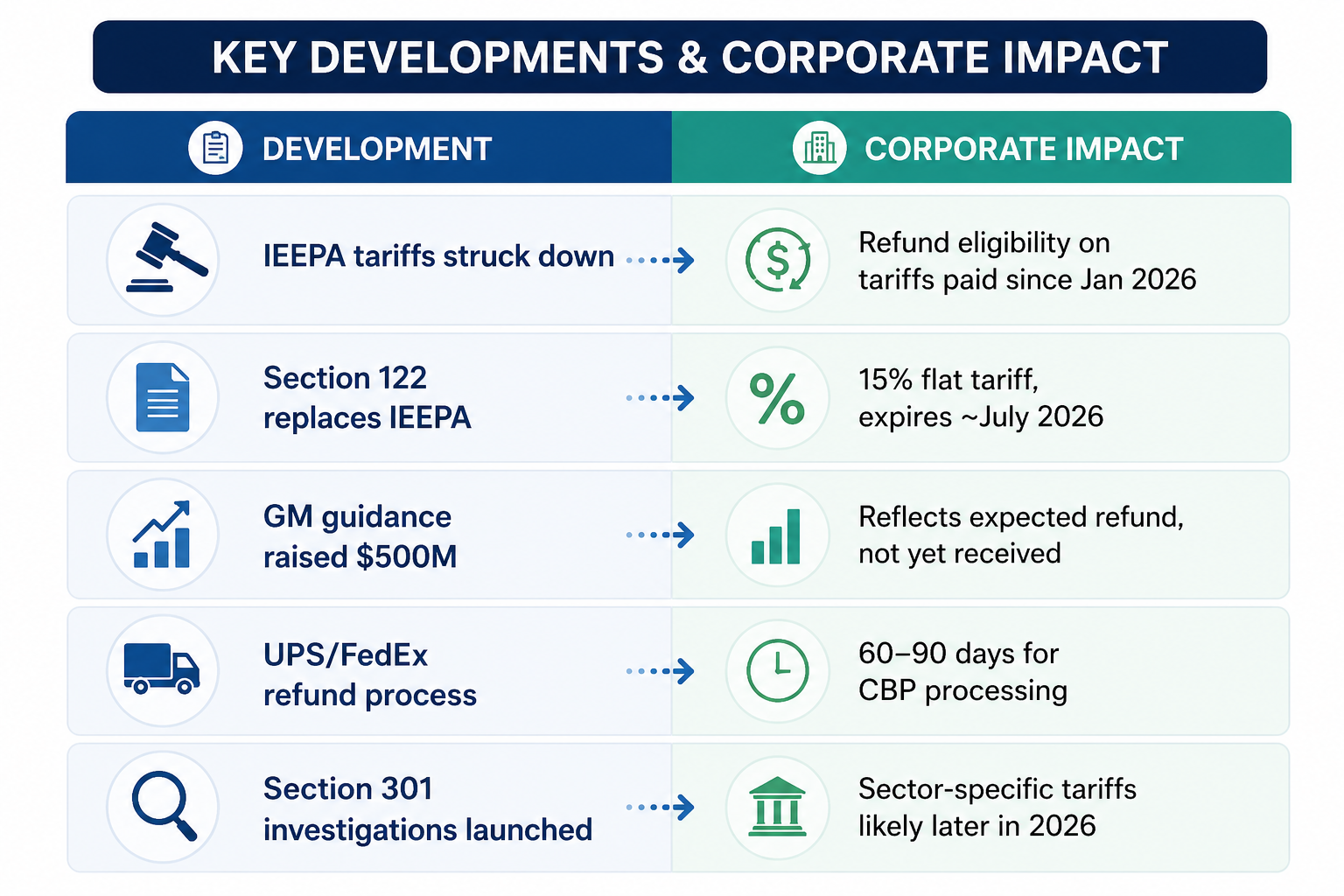

General Motors (GM) is expecting a $500 million tariff refund. UPS has started processing refunds for customers after collecting roughly $5 billion in tariffs on their behalf. For corporate America, the era of sweeping emergency-power tariffs is legally over, and financial damage might find relief.

But that story is running into a harder one. Brent crude (UKOUSD) crossed $111 a barrel this week, up 13 per cent in seven days, with prices still climbing despite Iran’s proposal to reopen the Strait of Hormuz. Trade cost relief and an energy-driven inflation shock are now moving in opposite directions at the same time, and markets have to price both simultaneously.

How the tariff landscape shifted

In February, the Supreme Court ruled that the International Emergency Economic Powers Act does not give the President authority to impose tariffs. The administration responded within hours — replacing the struck-down levies with a 15 per cent flat tariff on all imports under Section 122 of the Trade Act of 1974.

The change in legal architecture matters as much as the rate. Section 122 tariffs are time-limited to 150 days, require congressional approval to extend, and are non-discriminatory by design — they cannot easily be used as bilateral bargaining chips the way IEEPA tariffs were.

The administration has also launched new Section 301 investigations into manufacturing overcapacity across several major economies, flagging that sector-specific tariffs are the likely next phase.

For importers, the current picture looks like this:

The refund numbers are real, but context matters. GM’s $500 million sits against $3.1 billion in tariff costs it reported last year — the company still expects $2.5 to $3.5 billion in tariff expenses for 2026 after the refund. The legal architecture has changed. The cost burden on earnings has not disappeared.

Oil is in another direction

The IEA has described the Strait of Hormuz closure as the largest supply disruption in the history of the global oil market. Before the conflict began in late February, an average of 129 vessels crossed the strait each day. Last Sunday, only eight vessels did.

Saudi Arabia and the UAE have rerouted some supplies through overland pipelines, and a coordinated release of strategic reserves has helped prevent the worst-case price scenarios. But Brent (UKOUSD) above $110 is still a significant inflation input for any economy running import-heavy supply chains. Jet fuel, freight costs, and petrochemical inputs are all moving up with it.

The sectoral effects are already showing:

- Logistics: Freight costs rising sharply; air cargo most exposed

- Autos: Input cost pressure against overseas competitors, diminishing the impact of tariff refunds

- Retail: Import costs squeezed from both energy and residual tariff exposure

- Energy producers: US domestic output holding back despite elevated prices

Explore how to trade commodity markets and futures here.

Two forces, one earnings line

Both forces happening at once can be hard to read together. For CFD traders, that kind of environment is not a reason to step back. It is precisely the condition for short-term opportunities on both sides of the market.

The tariff relief story points toward demand recovery. Lower trade barriers reduce input costs, ease supply chain friction, and give margins room to improve. The oil shock points toward inflation persistence. Higher energy prices raise transportation costs, compress consumer spending, and put central banks back in a difficult position on rate cuts.

For sectors like autos and logistics, both forces are landing on the same earnings line at the same time. That is not a straightforward net positive — it is a compression from two directions.

Economists have drawn comparisons to the 1970s energy crisis, flagging risks of stagflation if price of oil stays elevated into the second half of the year. Whether that framing proves accurate depends heavily on how quickly Hormuz traffic recovers and whether the inflation spike reads as transitory or structural to central banks. Neither answer is clear yet. Explore types of inflation here.

What still needs resolving

Three variables will shape the picture more than anything else over the next quarter.

First, whether Section 122 tariffs survive legal challenge. Multiple states have already filed suits arguing that the balance-of-payments conditions required to justify tariffs do not exist. If those challenges succeed, trade policy enters another period of uncertainty before mid-year.

Second, how fast Hormuz shipping recovers. In this Trump era, every country is impacted by trade threats. Even with a ceasefire holding, traffic through the strait remains a fraction of pre-conflict levels. Experts expect months, not weeks, before oil prices normalise. With the inflation from the supply shock already embedded, regardless of what happens next.

Third, what the Section 301 investigations produce. If sector-specific tariffs on steel, semiconductors, and critical minerals arrive in the second half of the year, companies that assumed trade friction was behind them will need to revise that assumption.

The trade relief is not trivial. But it arrived into a market that already has a separate, larger problem to price.

Markets moving between two opposing forces do not trend cleanly in one direction. They swing and provide market conditions worth watching. There are several live instruments where the tension is directly tradable.

Explore assets mentioned with VT Markets today.

TLDR

Why are tariff refunds not fully improving corporate earnings?

While tariff refunds such as General Motors’ $500 million provide relief, they only offset a portion of prior costs. Companies are still facing ongoing tariff expenses, meaning the overall financial burden remains significant.

How do rising oil prices affect different sectors?

Higher oil prices increase costs across supply chains. Logistics firms face higher freight expenses, automakers deal with rising input costs, and retailers see pressure on margins due to more expensive imports and transportation.

What is the significance of the Section 122 tariff framework?

Section 122 tariffs are temporary and require congressional approval to extend. Unlike previous tariffs, they are broad and non-discriminatory, limiting their use as a strategic trade negotiation tool.

Why is the Strait of Hormuz disruption important for markets?

The Strait of Hormuz is a key global oil transit route. Reduced shipping traffic disrupts supply, pushing oil prices higher and increasing inflationary pressure worldwide.

What are the main factors markets are watching next?

Markets are focused on three key variables: legal challenges to Section 122 tariffs, the recovery speed of oil shipments through Hormuz, and the outcome of new Section 301 tariff investigations.

Start trading now – Click here to create your real VT Markets account