Overview

- Global bond yields remain under pressure as traders price inflation risk, fiscal deficits, and heavy government borrowing.

- Oil remains the key swing factor after Brent fell to $98.83 and WTI dropped to $92.03 on renewed U.S.-Iran peace hopes.

- U.S. Treasury yields still set the tone for USDX, XAUUSD, SP500, and global risk appetite.

- Traders face a busy week with Australia CPI, the RBNZ rate decision, U.S. Core PCE, and U.S. preliminary GDP.

Markets enter the week with one clear pressure point: bond yields remain too high for traders to ignore. Softer inflation in the UK, Canada, and Japan has helped sentiment, but the broader yield story still depends on oil prices, fiscal credibility, and upcoming U.S. inflation data.

The 10-year U.S. Treasury yield recently moved near 4.6%, while the average 10-year borrowing cost across G7 governments approached 4%, up from around 3.2% before the Iran war started in late February. That rise has kept pressure on mortgage rates, corporate credit, equity valuations, and emerging-market funding costs.

This creates a difficult backdrop for traders. Softer inflation data can calm parts of the market, but it does not fully reverse the bond rout while oil prices remain volatile and governments keep issuing large amounts of debt.

Oil Risk Still Drives The Inflation Story

Oil remains the clearest macro trigger. Brent crude fell 4.55% to $98.83, while WTI dropped 4.73% to $92.03 after markets priced a better chance of progress in U.S.-Iran talks. The drop helped risk assets because lower oil prices can ease inflation expectations and reduce pressure on central banks.

The relief remains fragile. Negotiations around the Strait of Hormuz are still in progress, and any delay or breakdown could pull oil higher again. A renewed oil spike would hit gasoline, transport, utilities, and production costs first, then risk spreading into wages and services.

For bond markets, this keeps the inflation outlook unstable. One soft inflation print may slow the selloff, but traders will need clearer evidence that energy prices are easing and staying lower.

Inflation Signals Are Starting To Split

The inflation picture now differs sharply across regions. In the UK, core CPI slowed to 2.5% in the 12 months to April, down from 3.1% in March, while services inflation fell from 4.5% to 3.2%. That gives the Bank of England more breathing room, but gilt yields remain sensitive to borrowing plans and fiscal credibility.

Japan also shows a softer inflation profile. Core consumer prices rose 1.4% year on year in April, marking a much cooler reading than the levels seen during the recent inflation shock. Yet Japanese government bonds remain under pressure as traders watch fiscal spending, energy subsidies, yen weakness, and the gradual end of ultra-low rates.

Europe faces a tougher mix. Euro area annual inflation is expected at 3.0% in April, up from 2.6% in March, according to Eurostat’s flash estimate. With growth still weak, the European Central Bank has less room to sound relaxed on inflation.

The U.S. sits at the centre of this cross-market pressure. The 10-year Treasury yield reached 4.69% last week, its highest level since January 2025, before easing to around 4.62%. That move shows how quickly bond stress can feed through to broader markets.

Fiscal Risk Keeps Long-Term Yields Elevated

Inflation is only one part of the yield story. Fiscal risk has become a major driver. Traders are demanding more compensation to hold long-term government debt as the U.S., UK, Japan, and parts of Europe continue to borrow heavily.

More bond supply forces markets to absorb more debt. When traders worry about deficits, they push yields higher, especially at the long end of the curve. This affects 10-year, 20-year, and 30-year maturities most directly.

The U.S. Treasury market remains the global benchmark. When U.S. yields rise, the impact spreads into USDX, gold, equity indices, emerging markets, and global funding conditions. The stress still looks orderly, but traders are demanding a higher reward for holding duration.

Japan may carry the deeper structural risk. If Japanese yields continue rising, domestic traders may bring capital home. That could reduce demand for U.S. and European bonds and add another layer of pressure to global yield curves.

Equities Can Still Rally, But Leadership May Narrow

Higher yields challenge equities because they raise the discount rate used to value future earnings. Growth stocks feel this pressure first because more of their value depends on profits expected far into the future.

U.S. equities have remained resilient because mega-cap technology, AI infrastructure, cloud spending, semiconductors, and data centre demand continue to support earnings expectations. Still, the rally becomes more fragile if leadership narrows into fewer stocks.

The S&P 500 can keep rising if earnings momentum stays firm and oil prices ease. The risk builds if yields remain high enough to pressure both valuations and earnings. Higher interest costs can slow business investment, raise consumer borrowing costs, and weaken demand.

This creates a more selective market. Large technology firms with strong cash flow may continue to attract buyers. Smaller companies, indebted firms, real estate, utilities, and unprofitable growth stocks may face more pressure.

What Could Bring Yields Lower

Bond yields need a clearer reason to fall. The first trigger would be a sustained decline in oil prices. Lower energy costs would ease inflation expectations and reduce pressure on central banks.

The second trigger would be broader disinflation. The UK and Japan have shown softer readings, but traders need similar progress in the U.S. and eurozone before buying duration with more confidence.

The third trigger would be weaker economic data. Softer jobs growth, lower wage pressure, weaker retail sales, and slower business investment could bring rate-cut expectations back into the market.

The fourth trigger would be stronger fiscal discipline. If governments show more control over deficits and debt issuance, traders may demand less compensation for holding long-term bonds.

The fifth trigger would be stronger demand at bond auctions. If traders absorb supply at current yields, the market can stabilise without needing inflation to collapse.

Key Symbols To Watch

USDX | XAUUSD | SP500 | USOil | BTCUSD

Upcoming Events

| Date | Currency | Event | Forecast | Previous | Analyst Remarks |

| 27 May 2026 | AUD | CPI y/y | 4.40% | 4.60% | Softer inflation may reduce RBA pressure, but AUD still needs support from commodities and China-linked demand. |

| 27 May 2026 | NZD | Official Cash Rate | 2.25% | 2.25% | A hold looks priced in. Guidance will drive NZD direction more than the rate decision. |

| 28 May 2026 | USD | Core PCE Price Index q/q | 0.30% | 0.30% | Sticky inflation would support yields and keep pressure on risk assets. |

| 28 May 2026 | USD | Preliminary GDP q/q | 2.10% | 0.70% | Strong growth may support equities, but it could also delay rate-cut expectations. |

For a full view of upcoming economic events, check out VT Markets’ Economic Calendar.

Key Movements Of The Week

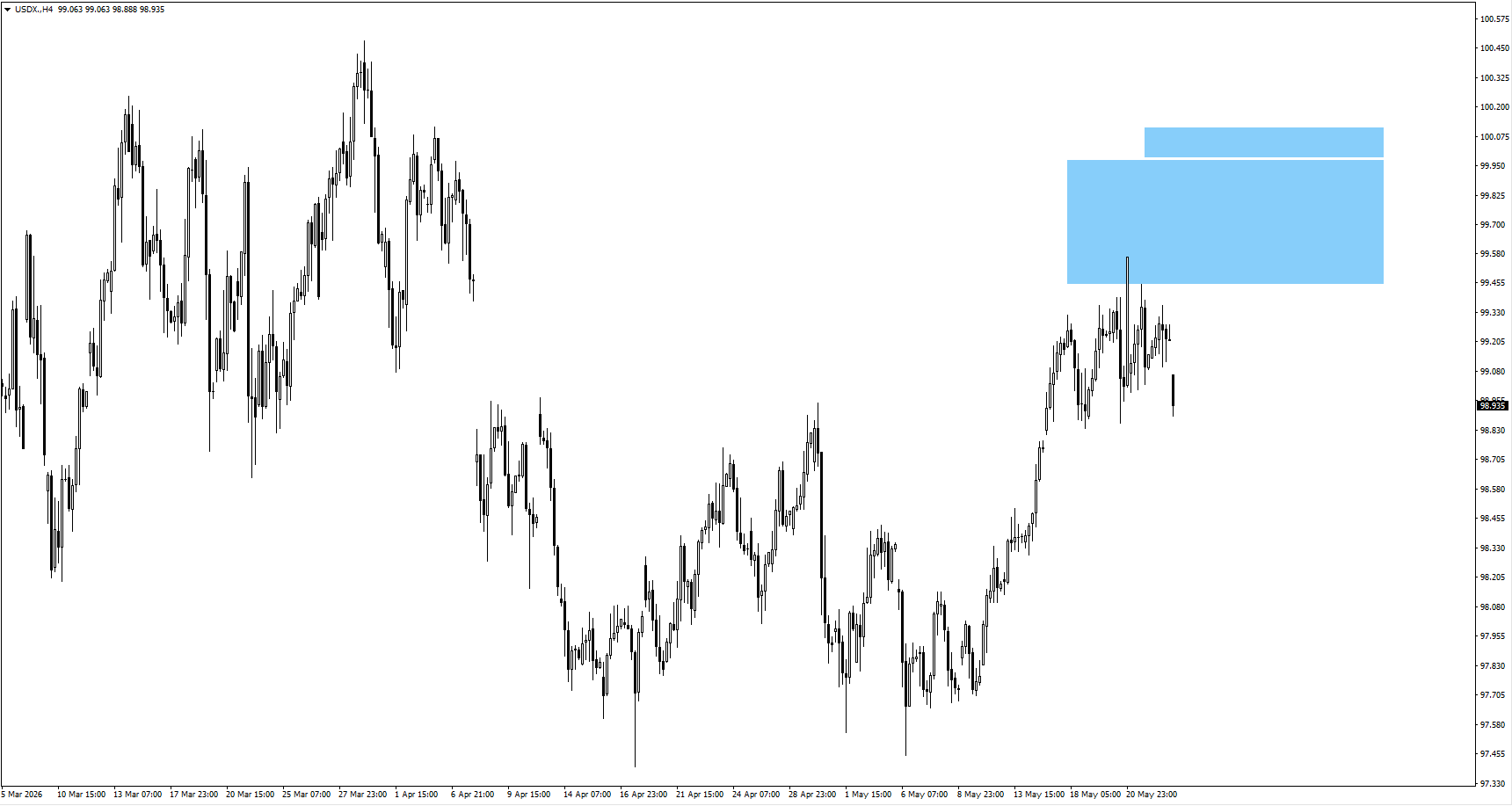

USDX

- The dollar index gapped lower after spending last week near the 99.65 monitored area, but price action has not confirmed a deeper bearish move.

- A rebound toward 99.85 could attract sellers if bearish price action forms near that area.

- Traders should watch whether Treasury yields continue to support the dollar or whether softer inflation data weakens the bullish case.

XAUUSD

- Gold continued its move after taking out liquidity, with the next upside reaction areas sitting around 4650 and 4690.

- If price consolidates without breaking 4590, downside risk may return as higher yields weigh on non-yielding assets.

- Gold traders should track the balance between real yield pressure and safe-haven demand from fiscal and geopolitical risks.

SP500

- The S&P 500 gained tailwind from improved sentiment around the U.S.-Iran talks, but the move still depends on confirmation of progress.

- A softer oil backdrop could support equities, while another yield spike may test stretched valuations.

- Traders should watch whether gains remain broad or become concentrated in mega-cap technology.

USOil

- Oil traded in a tight range before falling sharply on fresh optimism around a possible U.S.-Iran agreement.

- If negotiations progress, oil may stay under pressure and help cool inflation expectations.

- If talks stall, oil could rebound quickly and revive pressure on bonds, central banks, and risk assets.

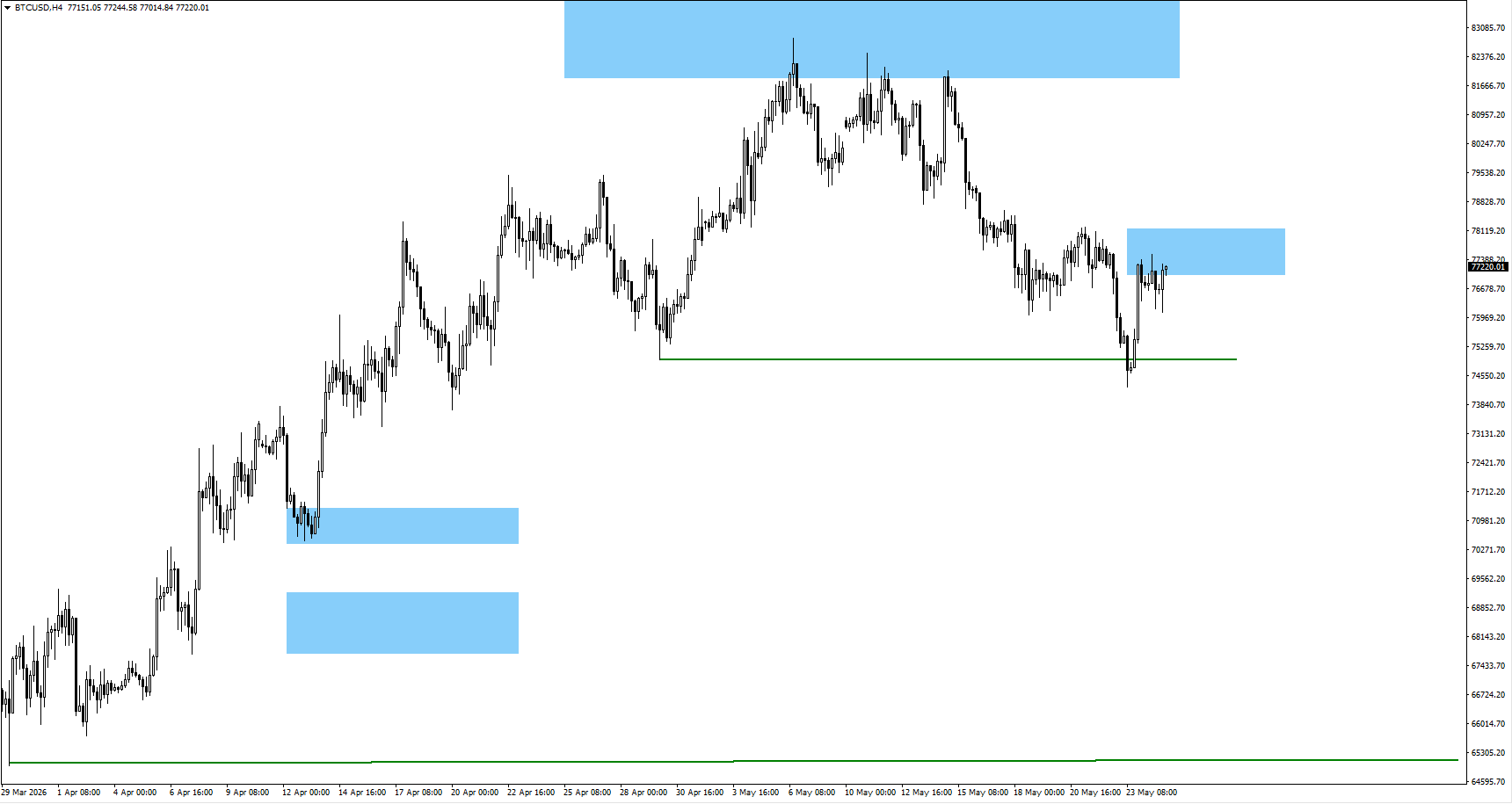

BTCUSD

- Bitcoin took out the 74,932 swing low, with traders now monitoring price action around 77,200.

- The structure may still allow a higher-time-frame fourth-wave rebound if risk appetite improves.

- Bitcoin needs stronger liquidity conditions and calmer bond markets to rebuild bullish momentum.

Bottom Line

The week ahead centres on whether bond markets can stabilise after a global repricing of inflation, fiscal risk, and long-term borrowing costs. Oil remains the fastest-moving trigger, especially with U.S.-Iran talks still shaping inflation expectations. U.S. Core PCE and preliminary GDP will guide Treasury yields, USDX, gold, and equity sentiment, while Australia CPI and the RBNZ rate decision may drive moves in AUDUSD and NZDUSD. A calmer oil market and softer inflation data could ease yield pressure, but sticky U.S. inflation or stronger GDP may keep the higher-for-longer trade alive.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Trader Questions

Why Are Global Bond Yields Still High If Inflation Is Cooling?

Bond yields remain high because investors are watching more than inflation. Softer price data in the UK, Canada, and Japan has helped sentiment, but markets are still pricing oil risk, fiscal deficits, heavy government borrowing, and central bank caution. The bond rout will likely need lower energy prices, better fiscal signals, and stronger demand at bond auctions before yields ease more clearly.

How Do Higher Bond Yields Affect The Stock Market?

Higher bond yields raise the cost of money and reduce the value investors place on future earnings. This usually hits growth stocks, smaller firms, real estate, utilities, and heavily indebted companies first. Mega-cap technology stocks may stay more resilient if earnings remain strong, but market leadership can narrow if yields stay elevated.

Why Is Oil Important For This Week’s Market Outlook?

Oil remains a key inflation trigger. Higher oil prices can raise gasoline, transport, utilities, and production costs, which may later feed into services and wages. If oil prices fall on progress in U.S.-Iran talks, inflation expectations could ease. If talks stall, oil may rebound and renew pressure on bonds, central banks, and risk assets.

What Could Bring Bond Yields Lower?

Bond yields could fall if oil prices decline, inflation cools across more regions, economic data weakens, governments show stronger fiscal discipline, or bond auctions attract stronger demand. Markets do not need inflation to collapse for yields to fall. They need confidence that current yield levels offer enough reward for the risks.

Which Markets Are Most Exposed To The Bond Rout?

The U.S. Treasury market remains the main stress point because it sets the tone for global borrowing costs. Japan also carries deeper structural risk as markets adjust to the end of ultra-low rates. The UK remains sensitive to fiscal credibility, while Europe faces pressure from weak growth, energy inflation, and fragile fiscal conditions.

Start trading now – Click here to create your real VT Markets account