Key Takeaways

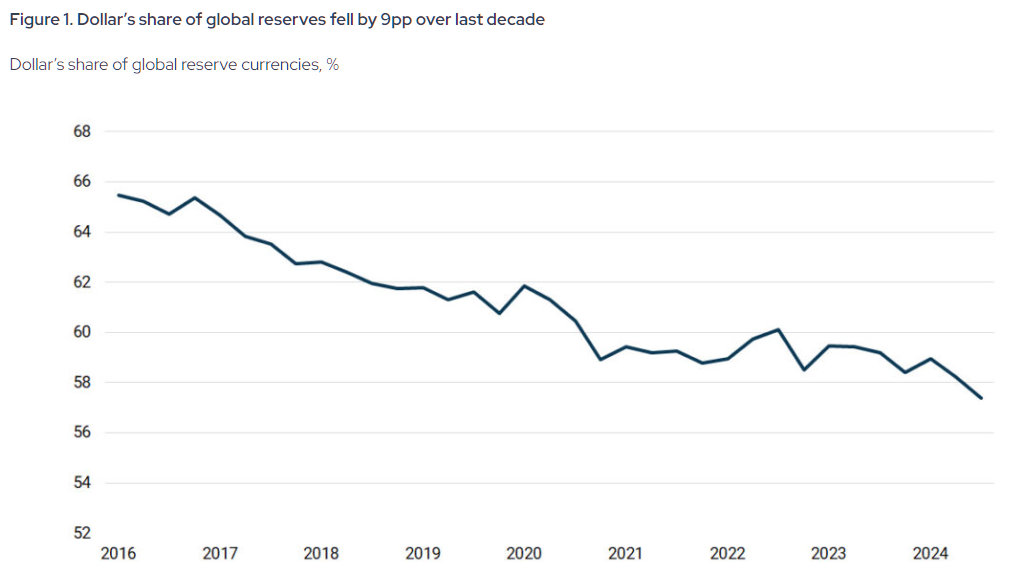

- The U.S. dollar’s share of global foreign exchange reserves has declined from a 2001 peak of 72% to 57.8% by the end of 2024.

- Dedollarisation is currently rated a 4 out of 10 in terms of severity, signifying a structural trend that is accelerating but not yet a crisis.

- Central banks have significantly increased gold holdings, purchasing over 1,000 tonnes annually between 2022 and 2024.

The Exorbitant Privilege Is Shrinking But is America Done?

For the better part of eighty years, the United States has enjoyed something no other country in modern history has possessed. It could print money the world was forced to accept. It could borrow at rates no other sovereign could match. It could run deficits that would bankrupt any other nation and wake up the next morning with the global financial system still running on its terms. The French called it an exorbitant privilege. The rest of the world simply lived with it.

The privilege is not ending. It is eroding, slowly but structurally, and that distinction is what markets are beginning to price.

Understanding Dedollarisation: The 3-Part Monopoly

Dedollarisation is not a single event. It is a process, the slow unwinding of the dollar’s three-part monopoly over global finance. The dollar is simultaneously the world’s primary reserve currency held by central banks, the dominant currency for settling international trade, especially in oil and commodities, and the default unit of account for sovereign debt markets. Dedollarisation means chipping away at all three, not necessarily replacing the dollar with one alternative, but diluting its exclusivity across dozens of smaller shifts happening simultaneously.

It is important to be clear about what dedollarisation is not. It is not a conspiracy. It is not a clean break. It is not imminent. It is a long structural shift that has been building for two decades and is now accelerating due to decisions made in Washington itself.

Why It Is Happening

The single most consequential accelerant was the freezing of Russia’s foreign exchange reserves in February 2022 following the invasion of Ukraine. In one decision, the United States demonstrated to every government on earth that dollar assets held abroad could be immobilised by Washington at will. Russia’s own dollar holdings collapsed from 41.5% of reserves before the sanctions to just 13 to 18% by late 2024. The message was received far beyond Moscow.

| Asset Class | Jan 2022 (Pre-Sanctions) | Jan 2025 (Adjustment) | Jan 2026 (Current) |

| Total Reserves | ~$630 Billion | ~$609 Billion | $769.1 Billion (Record High) |

| Gold Share | 21.50% | ~26% | ~43.0% |

| US Dollar | 20.90% | < 5% (Active) | ~0% (Active) |

| Euro | 32.10% | ~10% (Active) | ~0% (Active) |

| Chinese Yuan | 17.10% | ~30% | ~32-35% |

What followed was a layered response. By January 2025, Russia and Iran had effectively completed their own bilateral exit from the dollar, with over 95% of trade between the two countries settled in rubles and rials. China’s Cross-Border Interbank Payment System, known as CIPS, processed roughly 180 trillion yuan in transactions in 2025, equivalent to about USD25–26 trillion, providing a growing settlement alternative alongside the dollar-dominated SWIFT network.

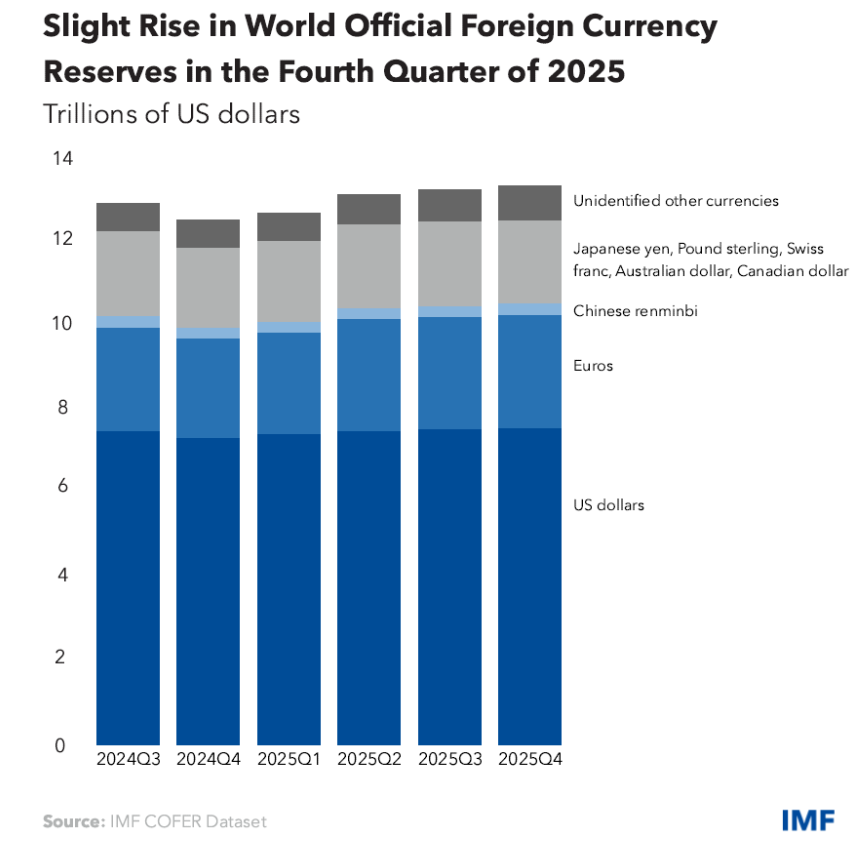

Central banks globally purchased over 1,000 tonnes of gold annually from 2022 through 2024, more than double the average of the previous decade. In 2025, they added another 863 tonnes, reinforcing the shift toward reserve diversification. The IMF’s own data shows the dollar’s share of global foreign exchange reserves fell from a peak of 72% in 2001 to 57.8% by the end of 2024.

While most of these shifts are gradual and institutional, recent geopolitical developments have begun to operationalise these alternatives in real-world trade flows.

The Petrodollar Under Threat: The Strait of Hormuz Tolls

During the war, Iran’s Islamic Revolutionary Guard Corps began charging oil tankers and LNG carriers up to two million dollars per vessel to transit the strait, demanding payment not in dollars, but in Bitcoin, USDT, or Chinese yuan routed through Kunlun Bank via CIPS. Iran’s parliament was reported to have codified this under the Strait of Hormuz Management Plan on March 30, 2026. At current traffic volumes of roughly 21 million barrels of oil passing through the strait daily, estimates place the toll revenue at USD600 to USD800 million per month. The dollar was not just bypassed. It was explicitly excluded.

This is not an isolated provocation. It is the most visible deployment yet of infrastructure that has been quietly scaling for years, a state using crypto and yuan payment rails as a sovereign revenue mechanism at the world’s most critical oil chokepoint. The Houthis in Yemen set an earlier template by charging vessels in the Red Sea. Iran has taken it further, and in doing so has demonstrated that the petrodollar system, the 1973 arrangement that made dollar settlement the price of admission to global energy markets, is no longer the only game in town.

What Happens to the US if Dedollarisation Continues

The dollar’s reserve status is not just a theory. It is a key part of U.S. power. Since global trade relies on dollars, there is steady demand for U.S. currency and assets even when the domestic economy is weak. This demand lets the government borrow at lower costs, run deficits without immediate pressure, and fund spending beyond what taxes alone could cover.

If that foundation weakens, the effects build up quickly. Without steady foreign demand for U.S. Treasuries, interest rates rise across the economy, increasing the cost of mortgages, business loans, and government borrowing at the same time. A weaker reserve role also puts pressure on the dollar, making imports more expensive and adding to inflation. Most importantly, the U.S. loses some of its financial influence, since sanctions are effective mainly because the dollar is widely used. If real alternatives to the dollar emerge, that influence becomes less powerful.

How Bad Is It Really

Despite these developments, the scale of the dollar’s dominance remains overwhelming. On a scale of one to ten where ten is bad, dedollarisation today sits at roughly four. Real, structural, and accelerating, but nowhere near a crisis.

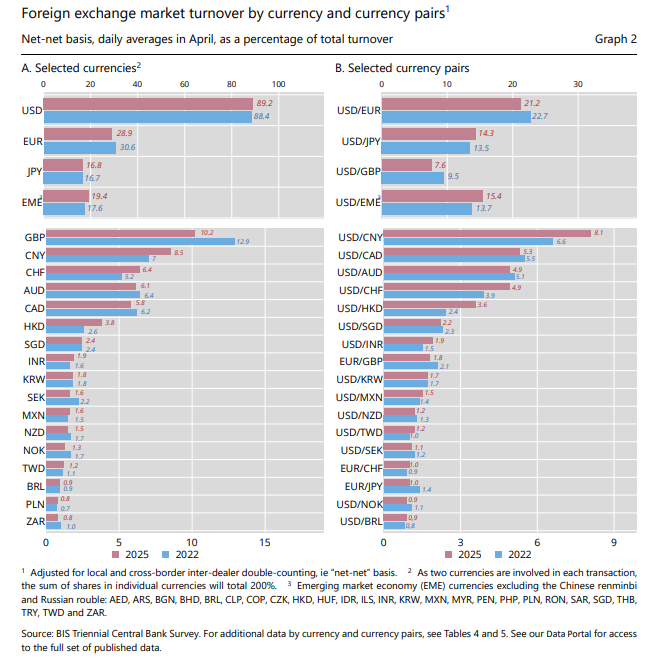

Data shows the dollar is still firmly dominant. The BIS 2025 Triennial Survey found it was involved in about 89% of all global foreign exchange trades, slightly higher than in 2022. At the BRICS summit in Rio, leaders did not even mention dedollarisation, and India stated clearly that it has no plan to replace the dollar, calling it a source of global stability. Meanwhile, China’s yuan is still limited by capital controls. In reality, no other currency or system is ready to take over the dollar’s global role anytime soon.

The score is a four and not a two because the trend is real and the infrastructure being built, CIPS, mBridge, BRICS Pay, digital yuan, local currency swap agreements, is not going away. It is a four and not a six because the dollar’s institutional moat remains enormous and no rival is close to bridging it. Yet this is where the story becomes counterintuitive.

The Investment Paradox: Why the World is Buying America While Fleeing the Dollar

Here is the number that stops every dedollarisation argument in its tracks. In 2025, foreign investors purchased a record $1.55 trillion in US financial assets according to the Treasury Department. They now hold $21 trillion in US equities, an all-time high. The number of days in 2026 where US stocks, the dollar, and bonds all declined simultaneously has fallen to just nine, on track for the lowest annual reading in eleven years. By comparison, the 1990s saw 30 to 60 such days per year.

The world is not fleeing America. It is buying America.

The explanation is that dedollarisation and investing in US markets are not contradictions. They are parallel rational strategies. Governments diversify away from holding dollar reserves issued and controlled by Washington while simultaneously wanting ownership of the most innovative, profitable companies on earth. US equities are not a dollar bet. They are a bet on American corporate earnings, American innovation, and American institutional depth. Until a rival market offers comparable liquidity, legal protection, and returns, capital will keep flowing in even as reserve managers quietly rebalance elsewhere.

The world is hedging the dollar institutionally while still trusting America commercially. That distinction matters enormously.

The Choice Facing America

The United States has two paths available to it. The first is pressure. It can threaten high tariffs on countries trying to move away from the dollar. This shows strength, but it can also backfire. If countries are already worried about the U.S. using the dollar as a weapon, more pressure will not stop them. It will push them to find alternatives faster.

The second choice is harder, but more effective in the long run. The U.S. needs to make the dollar trustworthy again. That means managing its finances responsibly, using sanctions carefully, keeping markets open, and staying involved in building the future of global payment systems instead of leaving it to China.

In the end, the dollar’s strength does not come from force. It comes from trust. Investors, governments, and institutions around the world hold dollars because they believe the U.S. will keep its word, act fairly, and remain a strong economy.

That trust is now being tested. The advantage the U.S. has enjoyed is slowly shrinking. Whether it continues or fades depends on whether the U.S. remembers that the dollar is not just money.

It is a promise, and that promise needs to be protected.

The Big Questions

1) Is the U.S. dollar losing its status as the world’s primary reserve currency?

The dollar is undergoing structural erosion rather than an imminent collapse. While its share of global foreign exchange reserves has fallen from 72% in 2001 to 56.77% by the end of 2025, it remains the world’s most utilised currency, involved in nearly 9 out of every 10 foreign exchange trades.

2) What are the primary drivers of dedollarisation in 2026?

The shift is largely fueled by the 2022 freezing of Russian foreign exchange reserves, which demonstrated that Washington can immobilise dollar assets at will. This has led nations to seek alternative payment rails like China’s CIPS and increase annual gold purchases to over 1,000 tonnes.

3) What is the investment paradox mentioned in recent market data?

The paradox describes a trend where global governments diversify away from dollar reserves while simultaneously increasing their ownership of U.S. commercial assets. In 2025, foreign investors held a record $21 trillion in the U.S. equities, signalling that they trust American innovation even as they hedge against the currency’s political risks.

4) How does the Strait of Hormuz impact the petrodollar system?

The petrodollar arrangement is no longer the exclusive system for energy trade since Iran began charging tankers up to $2 million in Bitcoin, USDT, or yuan for transit through the strait. This represents a visible deployment of non-dollar infrastructure at a critical global oil chokepoint.

5) How dominant is the U.S. dollar in global foreign exchange today?

Despite the rise of alternatives, the dollar remains overwhelmingly dominant and was involved in approximately 89% of all global foreign exchange trades according to 2025 data.

6) What are the economic risks to the United States if dedollarisation continues?

A significant weakening of the dollar’s reserve role would lead to higher domestic interest rates, increased costs for government borrowing, and higher inflation as imports become more expensive. Furthermore, the effectiveness of U.S. Financial sanctions would diminish as global trade moves to alternative systems.

7) Are other nations ready to replace the dollar?

Currently, no other currency or system is prepared to fully assume the dollar’s global role. Major economies like India continue to view the dollar as a source of global stability and have stated they have no plans to replace it.

Start trading now – Click here to create your real VT Markets account